FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

thumb_up100%

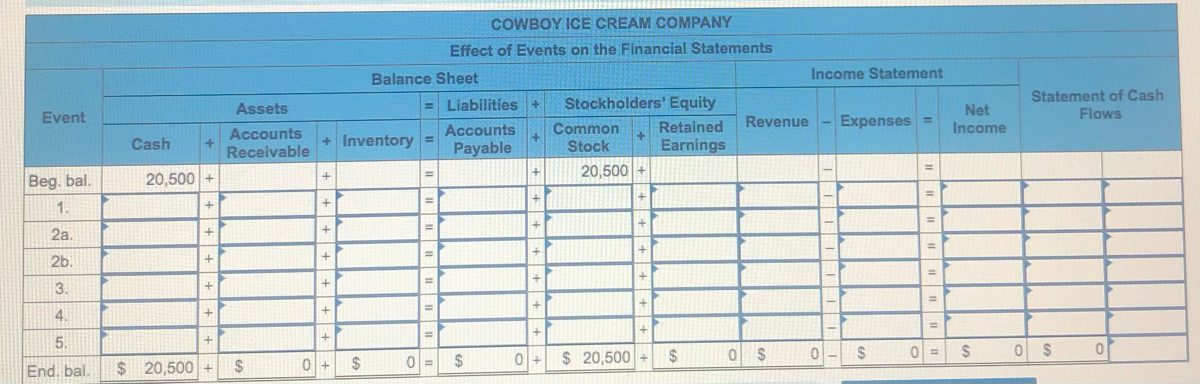

During Year 1, Cowboy Ice Cream Company purchased $25,000 of inventory on account. COC sold inventory on account that cost, $18,800 for $28,100. Cash payments on accounts payable were $15,600. There was $25,000 cash collected from accounts receivable , CIC also paid $4,500 cash for operating expenses. Assume that CIC started the accounting period with $20,500 in both cash and common stock.

Transcribed Image Text:COWBOY ICE CREAM COMPANY

Effect of Events on the Financial Statements

Balance Sheet

Income Statement

Statement of Cash

Flows

Assets

= Liabilities+

Stockholders' Equity

Net

Event

Revenue - Expenses

=

Accounts

%3D

Common

Retained

Income

Accounts

Cash

+ Inventory =

Payable

Stock

Earnings

Receivable

20,500 +

20,500 +

%3D

Beg. bal.

%3D

%3D

1.

%3D

%3D

2a.

%3D

%3D

2b.

%3D

%3D

3.

+

%3D

4.

%3D

5.

2$

$ 20,500

24

0- $

2$

End. bal.

$ 20,500 +

2$

Transcribed Image Text:b. Accounts receivable

c. Accounts payable

d. Gross margin

Net income

e. Net cash flow from operating activities

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Required information [The following information applies to the questions displayed below.] The following transactions apply to Ozark Sales for Year 1: 1. The business was started when the company received $50,000 from the issue of common stock. 2. Purchased merchandise inventory of $175,000 on account. 3. Sold merchandise for $206,500 cash (not including sales tax). Sales tax of 7 percent is collected when the merchandise is sold. The merchandise had a cost of $131,500. 4. Provided a six-month warranty on the merchandise sold. Based on industry estimates, the warranty claims would amount to 3 percent of sales. 5. Paid the sales tax to the state agency on $156,500 of the sales. 6. On September 1, Year 1, borrowed $20,000 from the local bank. The note had a 5 percent interest rate and matured on March 1, Year 2. 7. Paid $6,000 for warranty repairs during the year. 8. Paid operating expenses of $55,000 for the year. 9. Paid $124,000 of accounts payable. 10. Recorded accrued interest on…arrow_forwardDuring the current year, Royal Industries sold treasury stock for $32,000 cash. The treasury stock was purchased last year for $28,000. The company also issued bonds payable for $430,000 cash and declared and paid dividends of $40,000. What amount did Royal report on its statement of cash flows for cash provided by financing activities? O $390,000 O $394,000 O $422,000 O $434,000arrow_forwardYork Company engaged in the following transactions for Year 1. The beginning cash balance was $86,000 and the ending cash balance was $59,100. 1. Sales on account were $548,000. The beginning receivables balance was $128,000 and the ending balance was $90,000. 2. Salaries expense for the period was $232,000. The beginning salaries payable balance was $16,000 and the ending balance was $8,000. 3. Other operating expenses for the period were $236,000. The beginning other operating expenses payable balance was $16,000 and the ending balance was $10,000. 4. Recorded $30,000 of depreciation expense. The beginning and ending balances in the Accumulated Depreciation account were $12,000 and $42,000, respectively. 5. The Equipment account had beginning and ending balances of $44,000 and $56,000, respectively. There were no sales of equipment during the period. 6. The beginning and ending balances in the Notes Payable account were $36,000 and $44,000, respectively. There were no payoffs of…arrow_forward

- On Cherry Blossom Department Stores' most recent balance sheet, the balance of its inventory at the beginning of the year was $11,000. At the end of the year, the inventory balance was $17,500. During that year, its cost of goods sold was $59,000. All purchases of inventory throughout the year were on account. What was the total of Cherry Blossom's purchases during the year?arrow_forwardProcter & Gamble is a multinational corporation that manufactures and markets many household products. Assume sales for the company in a recent year were $66,000 (all amounts In millions). The annual report did not disclose the amount of credit sales, so we will assume that 90 percent of sales were on credit. The average gross profit on sales was 42 percent. Additional account balances were: Accounts receivable (net) Inventory Ending $6,500 6,831 Beginning $6,500 6,292 Required: Compute Procter & Gamble's receivables turnover ratio and Its Inventory turnover ratio. On average, how many days does it take for the company to collect its accounts receivable and sell its Inventory? Complete this question by entering your answers in the tabs below. Required 1 Required 2 Compute Procter & Gamble's receivables turnover ratio and its inventory turnover ratio. Note: Round your intermediate calculations and final answers to 2 decimal places. Turnover Accounts receivable Inventoryarrow_forwardOn January 1, Year 2 Grande Company had a $21,000 balance in the Accounts Receivable account and a zero balance in the Allowance for Doubtful Accounts account. During Year 2, Grande provided $78,000 of service on account. The company collected $74,500 cash from accounts receivable. Uncollectible accounts are estimated to be 2% of sales on account. What is the amount of cash flow from operating activities that would appear on the Year 2 statement of cash flows? Multiple Choice $57,420 $78,000 $74,500 $73,010arrow_forward

- Blooming Flower Company was started in Year 1 when it acquired $61,400 cash from the issue of common stock. The following data summarize the company's first three years' operating activities. Assume that all transactions were cash transactions. Purchases of inventory Sales Cost of goods sold Selling and administrative expenses Income Statements Balance Sheets Assets Cash Required Prepare an income statement (use multistep format) and balance sheet for each fiscal year. (Hint: Record the transaction data for each accounting period in the accounting equation before preparing the statements for that year.) Merchandise inventory Complete this question by entering your answers in the tabs below. Total assets Liabilities Stockholders' equity Common stock Retained earnings Total stockholders' equity Total liabilities and stockholders' equity Year 1 $22,300 26,500 12,400 5,310 $ 60,290 9,900 Prepare a balance sheet for each fiscal year. (Hint: Record the transaction data for each accounting…arrow_forwardSilk Enterprises operates a small retail store that makes all merchandise inventory purchases on account. During the current year, Silk's cost of goods sold is $193,000 and its cash payments to suppliers of inventory are $179,000. Which combination of changes to the inventory and accounts payable balances during the year are consistent with the difference between cost of goods sold and cash payments to suppliers of inventory? O Inventory increased by $28,000 and accounts payable increased by $42,000 O Inventory decreased by $28,000 and accounts payable decreased by $42,000 Inventory increased by $28,000 and accounts payable decreased by $42,000 Inventory decreased by $28,000 and accounts payable increased by $42,000 None of the abovearrow_forwardHow do I answer #5?arrow_forward

- Festivus Company has working capital of $140,680 on December 30. On December 31 it has the following transactions: An account payable for $10,000 is paid off An account receivable of $1,000 is written off (Festivus does not use the direct write-off method) $16,600 more inventory is purchased on account. If Account Payable balance on December 30th is $10,000 what is the Days Accounts Payable are outstanding? Use ending balance of AP instead of the average. Festivus' Gross profit percentage isarrow_forwardStmt of Cash Flows and Req C, please The following transactions apply to Ozark Sales for Year 1: The business was started when the company received $50,000 from the issue of common stock. Purchased equipment inventory of $178,000 on account. Sold equipment for $192,000 cash (not including sales tax). Sales tax of 6 percent is collected when the merchandise is sold. The merchandise had a cost of $117,000. Provided a six-month warranty on the equipment sold. Based on industry estimates, the warranty claims would amount to 5 percent of sales. Paid the sales tax to the state agency on $142,000 of the sales. On September 1, Year 1, borrowed $21,500 from the local bank. The note had a 6 percent interest rate and matured on March 1, Year 2. Paid $5,900 for warranty repairs during the year. Paid operating expenses of $56,000 for the year. Paid $124,000 of accounts payable. Recorded accrued interest on the note issued in transaction no. 6. Required Record the given transactions in a…arrow_forwardThe balance of Total Assets for Virtue Company is $500,000 on November 30. During November, the following took place:Sold $60,000 of inventory for cashPurchased a $100,000 machine for cashIncreased accounts payable $50,000 by acquisitions of inventory on accountWrote off accounts receivable of $20,000Total Assets for Virtue Company on November 1 is: Multiple Choice $550,000 $530,000 none of the other alternatives are correct $500,000 $450,000arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education