ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

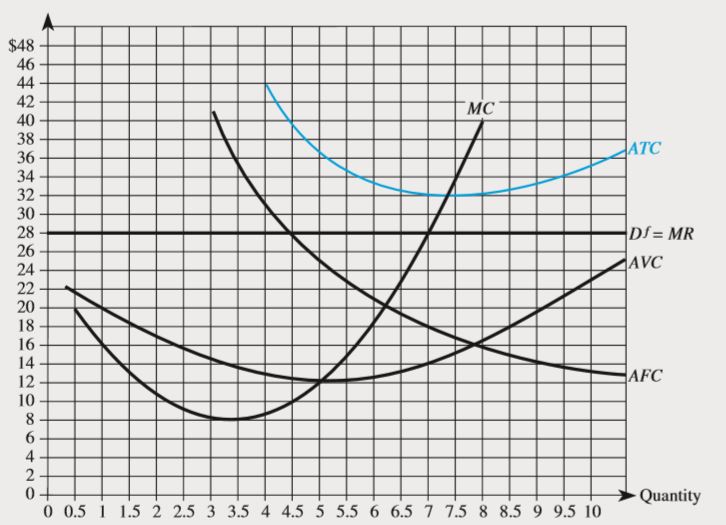

The following graph summarizes the demand and costs for a firm that operates in a

Transcribed Image Text:$48

46

44

42

40

38

36

34

32

30

MC

ATC

Df= MR

28

26

24

AVC

22

20

18

16

14

12

10

AFC

8.

6.

4

Quantity

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 6.5 7 7.5 8 8.5 9 9.5 10

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider the competitive market for dress shirts. The following graph shows the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves for a typical firm in the industry. For each price in the following table, use the graph to determine the number of shirts this firm would produce in order to maximize its profit. Assume that when the price is exactly equal to the average variable cost, the firm is indifferent between producing zero shirts and the profit-maximizing quantity. Also, indicate whether the firm will produce, shut down, or be indifferent between the two in the short run. Lastly, determine whether it will make a profit, suffer a loss, or break even at each price.arrow_forwardAnswer D to H.arrow_forwardThe graph below shows the marginal cost (MC), average variable cost (AVC), and average total cost (ATC) curves for a firm in a competitive market. These curves imply a short-run supply curve that has two distinct parts. One part, not shown, lies along the vertical axis (quantity-0); this represents a condition of production shutdown. Where is the other part? Use the straight-line tool to drawit. To refer to the graphing tutorial for this question type, please click here Price and cost 18 15 14 13 12 10 19/21 SUBMIT ANSWER 13 OF 21 QUESTIONS C OMPLETED 28 MacBook Pro 금□ F7 F8 F9 F1o F2 F3 F5arrow_forward

- Suppose a corn dog stand market is perfectly competitive and in long-run equilibrium. One day, the city starts imposing a $300 per year tax on each stand. How does this policy impact the number of corn dogs produced and sold in the market in the short run and long run? Down in the short run and no change in the long run No change in the short run and down in the long run Up in the short run and no change in the long run No change in the short run and up in the long runarrow_forwardUse the table Costs for Alina's Apple Pies. If Alina's Apple Pies operates in a perfectly competitive market and the market price for a pie is $18, how many pies should Alina's Apple Pies produce and what is the economic profit or loss per unit?arrow_forwardConsider the perfectly competitive market for dress shirts. The following graph shows the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves for a typical firm in the industry. PRICE AND COST PER UNIT (Dollars) 100 90 80 70 60 40 30 20 10 0 0 ☐ ☐ MC ■ ATC AVC 70, 85 ■ 10 20 30 40 50 60 70 80 90 QUANTITY OF OUTPUT (Thousands of shirts) 100 ?arrow_forward

- A market in perfect competition is in long-run equilibrium. What happens to the market if labor unions are able to increase wages for workers? Include a detailed set of graphs showing both the market and firm long run equilibration in reaction to the change.arrow_forwardWhy don't firms in a competitive market have excess capacity in the long run?arrow_forward9.7. A producer operating in a perfectly competitive market has chosen his output level to maximize profit. At that output, his revenue and costs are as follows: Revenue Variable costs $200 $120 $60 Sunk fixed costs Nonsunk fixed costs $40 Calculate his producer surplus and his profits. Which (if either) of these should he use to determine whether he should exit the market in the short run? Briefly explain. 9.8. Dave's Fresh Catfish is a northern Mississippi farm that operates in the perfectly competitive catfish farming industry. Dave's short-run total cost curve is STC(Q) = 400 + 2Q + 0.5Q², where Q is the number of catfish harvested per month. The corresponding short-run marginal cost curve is SMC(Q)=2+ Q. All of the fixed costs are sunk. a. What is the equation for the average variable cost (AVC)? b. What is the minimum level of average variable costs? c. What is Dave's short-run supply curve?arrow_forward

- What is the most important decision a perfectly competitive firm must make in order to maximize profit? what quantity to produce what price to charge what quality to produce what quantity of labor is neededarrow_forwardQ3arrow_forwardIn Problem 5, the market demand decreases and the demand schedule becomes: If firms have the same costs set out in Problem 5, what is the market price and the firm’s economic profit or loss in the short run? Problem 5 The market for paper is perfectly competitive and 1,000 firms produce paper. The table sets out the market demand schedule for paper. The table in the next column sets out the costs of each producer of paper. Calculate the market price, the market output, the quantity produced by each firm, and the firm’s economic profit or loss.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education