ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

{kind=link}

Question

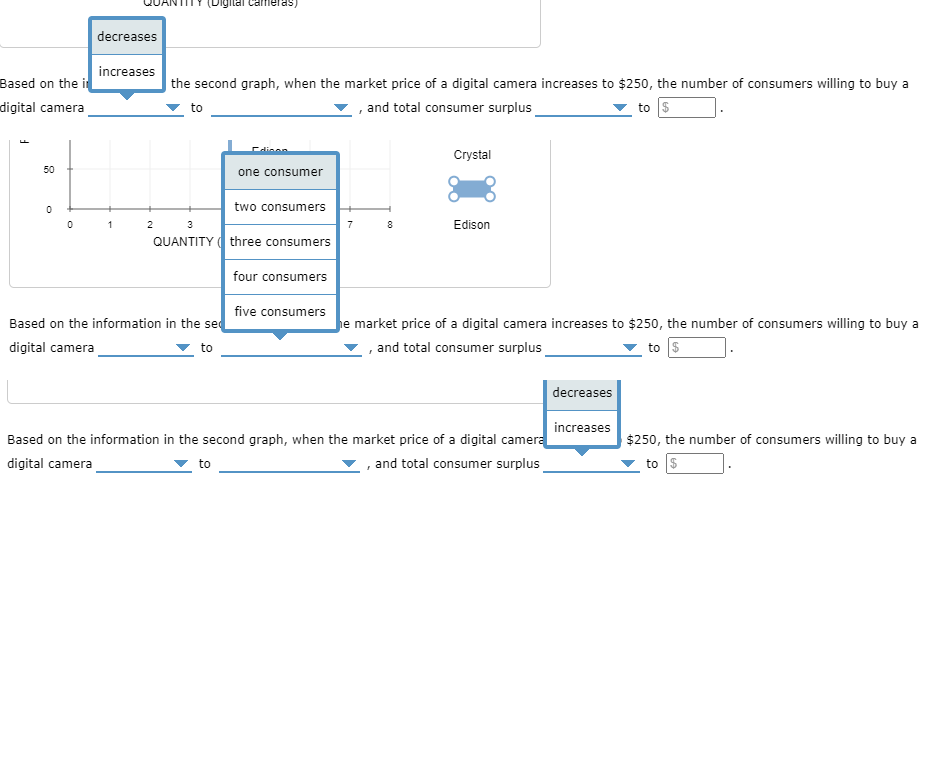

Transcribed Image Text:gilal cameras)

decreases

increases

Based on the i

| the second graph, when the market price of a digital camera increases to $250, the number of consumers willing to buy a

digital camera

, and total consumer surplus

to s

to

Edinon

Crystal

50

one consumer

two consumers

2 3

QUANTITY ( three consumers

1

7

Edison

four consumers

five consumers

Based on the information in the se

digital camera

he market price of a digital camera increases to $250, the number of consumers willing to buy a

, and total consumer surplus

to

to $

decreases

increases

Based on the information in the second graph, when the market price of a digital camera

, and total consumer surplus

$250, the number of consumers willing to buy a

digital camera

to

to $

Transcribed Image Text:13. Consumer surplus for a group of consumers

Based on the information on the previous graph, you can tell that

will buy digital cameras at the given market price, and total

The following graph shows the demand curve for a group of consumers in the U.S. market (blue line) for digital cameras. The market price of a digital

consumer surplus in this market will be $

camera is shown by the black horizontal line at $150.

one consumer

Suppose the market price of a digital camera increases to $250.

two consumers

Each rectangle you can place on the following graph corresponds to a particular buyer in this market: orange (square symbols) for Tim, green

three consumers

(triangle symbols) for Alyssa, purple (diamond symbols) for Brian, tan (dash symbols) for Crystal, and blue (circle symbols) for Edison. Use the

On the following graph, use the rectangles once again to shade th

consumer surplus for each person who is willing and able to

four consumers

rectangles to shade the areas representing consumer surplus for each person who is willing and able to purchase a digital camera at a market price of

purchase a digital camera at the new market price: orange (squar

green (triangle symbols) for Alyssa, purple (diamond symbols)

$150. (Note: If a person will not purchase a digital camera at the market price, indicate this by leaving his or her rectangle in its original position on

for Brian, tan (dash symbols) for Crystal, and blue (circle symbols five consumers

If a person will not purchase a digital camera at the new

the palette.)

market price, indicate this by leaving his or her rectangle in its original posiTIon on the palette.)

Hint: You can view the area of a rectangle by clicking the rectangle after you have plotted it.

400

Tim

350

400

Tim

Alyssa

Tim

300

350

Tim

Alyssa

Market Price

250

300

Alyssa

Brian

250

Alyssa

Brian

Brian

150

8 200

Crystal

100

Market Price

Brian

150

Edison

Crystal

Crystal

50

100

Edison

Crystal

3

5

7

8

Edison

50

QUANTITY (Digital cameras)

2

5

6

7

Edison

QUANTITY (Digital cameras)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Answer the following questions based on the graph that represents Kyle's demand for ribs per week at Big Ed's Barbecue. f. If the price of ribs rose to $10, what would happen to Big Ed's producer surplus? g. What is the total surplus in this market at a price of $10? h. If the price of ribs fell to $5, what would be Kyle's consumer surplus? j. What is the total surplus in this market at a price of $5?arrow_forward9 Erika's evaluation of packets of nacho chips in terms of $MU is shown in table below. Marginal Consumer Surplus Quantity of Chips 1 2 3 4 5 SMU $ 3.50 2.70 1.90 1.50 1.40 Price $1.30 1.30 1.30 1.30 1.30 $ Total Consumer Surplus $ If Erika buys five packets, calculate her marginal consumer surplus for each packet and the total consumer surp complete table above. Round your answers to 2 decimal places.arrow_forwardam. 122.arrow_forward

- John is looking to sell his car and Mary is looking to buy it. John values the car at $2000 and Mary values it at $3000. John offers to sell it to Mary at a price of $3500. Which of the following is true: O Mary will accept the offer and the total surplus will be $1000 Mary will not accept the offer and the total surplus yill be 0. O Mary will accept the offer but the total surplus will be less than $1000 O Mary will not accept the offer and the total surplus will be $1000. O None of the abovearrow_forwardIf the price of a hamburger falls from $2.00 to $1.50, the gain in consumer surplus to consumers who are persuaded to buy at the lower price (and who were not buying when the price was $2.00) is equal to:arrow_forwardHelp with this one pleasearrow_forward

- KE Consider the market for some product X that is represented in the accompanying demand-and-supply diagram a. Calculate the total economic surplus in this market at the free-market equilibrium price and quantity The total economic surplus is $ per day (Round your response to the nearest cent as needed) 57.00 $5.00 45.00 30 00 3300 27.00 21.00 15.00 900 300- 10 25 15 20 Quantity (units per day) 30arrow_forwardPrice per unit Supply & Demand $34 a. 18 12 le C. 6. 1. D. 32 44 68 Units per day The graph above shows the market for movie tickets at a small theatre. The letters on the graph represent the bounded areas. Using the graph above, if the price is set to $12, what is the consumer surplus in the market? Note: enter answer with only numerical values and round up to the nearest tenth. For example, if you think the answer is "$101.58" then enter the answer "101.6" in the space below.arrow_forwardPrice 27.5 CHOKRESE DEDELS 85 80 75 70 65 60 55 50 45 40 35 30 25 20 15 10 5 Supply Demand 5 10 15 20 25 30 35 40 45 50 55 60 65 70 Quantity Refer to the figure. When the price falls from $45 to $35, consumer surplus increases by $100 from new consumers entering the market. O increases by $50 from new consumers entering the market. increases by $50 from consumers who were already buying the good now paying a lower price. decreases by $50 from consumers who were already buying the good now paying a lower price.arrow_forward

- 2. 3-5: Attaining Market Equilibrium *3* The Wall Street Journal of March 20, 2020, reported on the "large surplus of oil" as there is not enough storage capacity to hold the refined oil. Assuming the price of oil is set by competitive market forces, which of the following sequence of events accurately describes how the surplus of oil would be eliminated? As price decreases, the: Quantity demanded decreases, quantity supplied increases, and a new equilibrium will be reached. O Quantity demanded increases, quantity supplied increases, and a new equilibrium will be reached. O Demand decreases, supply increases, and a new equilibrium will be reached. O Demand increases, supply decreases, and a new equilibrium will be reached. O Quantity demanded increases, quantity supplied decreases, and a new equilibrium will be reached.arrow_forward© Macmillan Learning The table contains the maximum willingness to pay of five college students wanting to buy a tablet on Amazon. Student Willingness to pay Anthony $500 Amanda $400 Lily $300 Francisco $200 Max $100 What is total consumer surplus for the five students? If the price increases from $300 to $500, what is the change in total consumer surplus? SA SAarrow_forwardO Macmillan Learning Suppose that Michelle buys a cappuccino from Paul's Cafe and Bakery for $4.25. Michelle was willing to pay up to $7.25 for the cappuccino, and Paul's Cafe and Bakery was willing to accept $1.75 for the cappuccino. Based on this information, answer the following questions. Michelle's consumer surplus: $ Paul's Cafe and Bakery's producer surplus: $arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education