FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

A. Prepare CORIS RA Statement of

B. Prepare CORIS RA Statement of Financial Performance for the year ended December 31, 2020

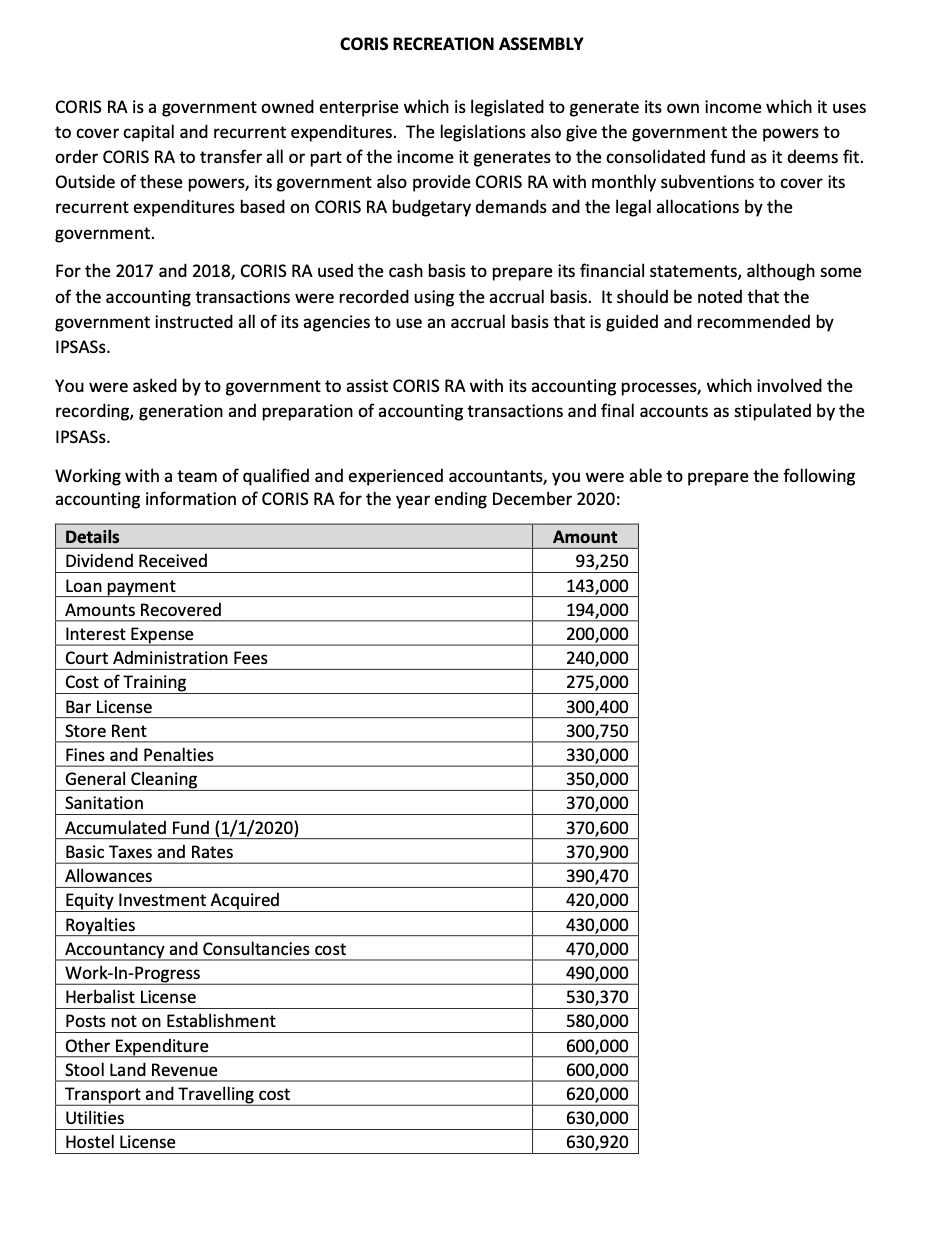

Transcribed Image Text:CORIS RECREATION ASSEMBLY

CORIS RA is a government owned enterprise which is legislated to generate its own income which it uses

to cover capital and recurrent expenditures. The legislations also give the government the powers to

order CORIS RA to transfer all or part of the income it generates to the consolidated fund as it deems fit.

Outside of these powers, its government also provide CORIS RA with monthly subventions to cover its

recurrent expenditures based on CORIS RA budgetary demands and the legal allocations by the

government.

For the 2017 and 2018, CORIS RA used the cash basis to prepare its financial statements, although some

of the accounting transactions were recorded using the accrual basis. It should be noted that the

government instructed all of its agencies to use an accrual basis that is guided and recommended by

IPSASS.

You were asked by to government to assist CORIS RA with its accounting processes, which involved the

recording, generation and preparation of accounting transactions and final accounts as stipulated by the

IPSASS.

Working with a team of qualified and experienced accountants, you were able to prepare the following

accounting information of CORIS RA for the year ending December 2020:

Details

Amount

Dividend Received

93,250

Loan payment

Amounts Recovered

143,000

194,000

200,000

240,000

275,000

Interest Expense

Court Administration Fees

Cost of Training

Bar License

300,400

300,750

330,000

Store Rent

Fines and Penalties

General Cleaning

350,000

370,000

370,600

Sanitation

Accumulated Fund (1/1/2020)

Basic Taxes and Rates

370,900

390,470

420,000

Allowances

Equity Investment Acquired

Royalties

Accountancy and Consultancies cost

Work-In-Progress

430,000

470,000

490,000

530,370

Herbalist License

Posts not on Establishment

580,000

Other Expenditure

600,000

600,000

620,000

630,000

630,920

Stool Land Revenue

Transport and Travelling cost

Utilities

Hostel License

Transcribed Image Text:Details

Amount

660,000

720,400

Advances to Staff

Local Park Fees

Inventory and Consumables

Special Services

800,000

820,000

820,900

840,300

870,000

Property Rate

Social Benefit

Market Tolls

Consumption of Fixed Assets

Infrastructure, Plant and Equipment

960,000

980,000

Permit Fees

990,000

990,320

1,140,700

Proceeds from Sale of Equity

Established Posts

Development Bonds Issued

1,300,000

2,300,600

2,330,000

2,930,00

6,120,800

Business Income

Loans Received

Local Fund

Rent from Land and Building

Central Government Salaries

12,000,000

12,300,240

15,000,600

Cash and Cash Equivalent @ (1/1/2020)

Parish Development Facility

NOTES

1. You are to ensure that CORIS RA adopts and maintain the accrual accounting basis when preparing

its financial statements

2. As of December 31, 2020, the Established Post had outstanding salaries of $180,000,000.00

3. Closing Inventory and Consumables as at December 31, 2020 stood at $170,000,000.00

Using the guidelines and formats set out in the applicable IPSASS, you are to:

A. Prepare CORIS RA Statement of Cash Flow for the year ended December 31, 2020

B. Prepare CORIS RA Statement of Financial Performance for the year ended December 31, 2020

C. Using the contents presented in the Units supported by information in the relevant IPSASS, give a

comprehensive definition (with examples) of revenue and expenditure appropriate for a Central

Government. I

D. The IPSASS indicated some benefits of Cash Flow Information. State any two of these benefits to

an entity and also the general public.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps with 4 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- CORIS RA is a government owned enterprise which is legislated to generate its own income which it uses to cover capital and recurrent expenditures. The legislations also give the government the powers to order CORIS RA to transfer all or part of the income it generates to the consolidated fund as it deems fit. Outside of these powers, its government also provide CORIS RA with monthly subventions to cover its recurrent expenditures based on CORIS RA budgetary demands and the legal allocations by the government. For the 2017 and 2018, CORIS RA used the cash basis to prepare its financial statements, although some of the accounting transactions were recorded using the accrual basis. It should be noted that the government instructed all of its agencies to use an accrual basis that is guided and recommended by IPSASs. You were asked by to government to assist CORIS RA with its accounting processes, which involved the recording, generation and preparation of accounting transactions and final…arrow_forwardCORIS RA is a government owned enterprise which is legislated to generate its own income which it uses to cover capital and recurrent expenditures. The legislations also give the government the powers to order CORIS RA to transfer all or part of the income it generates to the consolidated fund as it deems fit. Outside of these powers, its government also provide CORIS RA with monthly subventions to cover its recurrent expenditures based on CORIS RA budgetary demands and the legal allocations by the government. For the 2017 and 2018, CORIS RA used the cash basis to prepare its financial statements, although some of the accounting transactions were recorded using the accrual basis. It should be noted that the government instructed all of its agencies to use an accrual basis that is guided and recommended by IPSASs. You were asked by to government to assist CORIS RA with its accounting processes, which involved the recording, generation and preparation of accounting transactions and final…arrow_forwardCORIS RA is a government owned enterprise which is legislated to generate its own income which it uses to cover capital and recurrent expenditures. The legislations also give the government the powers to order CORIS RA to transfer all or part of the income it generates to the consolidated fund as it deems fit. Outside of these powers, its government also provide CORIS RA with monthly subventions to cover its recurrent expenditures based on CORIS RA budgetary demands and the legal allocations by the government. For the 2017 and 2018, CORIS RA used the cash basis to prepare its financial statements, although some of the accounting transactions were recorded using the accrual basis. It should be noted that the government instructed all of its agencies to use an accrual basis that is guided and recommended by IPSASs. You were asked by to government to assist CORIS RA with its accounting processes, which involved the recording, generation and preparation of accounting transactions and final…arrow_forward

- CORIS RA is a government owned enterprise which is legislated to generate its own income which it uses to cover capital and recurrent expenditures. The legislations also give the government the powers to order CORIS RA to transfer all or part of the income it generates to the consolidated fund as it deems fit. Outside of these powers, its government also provide CORIS RA with monthly subventions to cover its recurrent expenditures based on CORIS RA budgetary demands and the legal allocations by the government. For the 2017 and 2018, CORIS RA used the cash basis to prepare its financial statements, although some of the accounting transactions were recorded using the accrual basis. It should be noted that the government instructed all of its agencies to use an accrual basis that is guided and recommended by IPSASs. You were asked by to government to assist CORIS RA with its accounting processes, which involved the recording, generation and preparation of accounting transactions and final…arrow_forwardCORIS RA is a government owned enterprise which is legislated to generate its own income which it uses to cover capital and recurrent expenditures. The legislations also give the government the powers to order CORIS RA to transfer all or part of the income it generates to the consolidated fund as it deems fit. Outside of these powers, its government also provide CORIS RA with monthly subventions to cover its recurrent expenditures based on CORIS RA budgetary demands and the legal allocations by the government. For the 2017 and 2018, CORIS RA used the cash basis to prepare its financial statements, although some of the accounting transactions were recorded using the accrual basis. It should be noted that the government instructed all of its agencies to use an accrual basis that is guided and recommended by IPSASs. You were asked by to government to assist CORIS RA with its accounting processes, which involved the recording, generation and preparation of accounting transactions and final…arrow_forwardCORIS RECREATION ASSEMBLY CORIS RA is a government owned enterprise which is legislated to generate its own income which it uses to cover capital and recurrent expenditures. The legislations also give the government the powers to order CORIS RA to transfer all or part of the income it generates to the consolidated fund as it deems fit. Outside of these powers, its government also provide CORIS RA with monthly subventions to cover its recurrent expenditures based on CORIS RA budgetary demands and the legal allocations by the government. For the 2017 and 2018, CORIS RA used the cash basis to prepare its financial statements, although some of the accounting transactions were recorded using the accrual basis. It should be noted that the government instructed all of its agencies to use an accrual basis that is guided and recommended by IPSASs. You were asked by to government to assist CORIS RA with its accounting processes, which involved the recording, generation and preparation of…arrow_forward

- CORIS RA is a government owned enterprise which is legislated to generate its own incomewhich it uses to cover capital and recurrent expenditures. The legislations also give thegovernment the powers to order CORIS RA to transfer all or part of the income it generates tothe consolidated fund as it deems fit. Outside of these powers, its government also provideCORIS RA with monthly subventions to cover its recurrent expenditures based on CORIS RAbudgetary demands and the legal allocations by the government.For the 2017 and 2018, CORIS RA used the cash basis to prepare its financial statements,although some of the accounting transactions were recorded using the accrual basis. It should benoted that the government instructed all of its agencies to use an accrual basis that is guided andrecommended by IPSASs.You were asked by to government to assist CORIS RA with its accounting processes, whichinvolved the recording, generation and preparation of accounting transactions and final accountsas…arrow_forwardDoes the report reflect fund financial statements for governmental, proprietary, and fiduciary funds? List those statements. List the major governmental and proprietary funds (the funds that have separate columns in the governmental and proprietary fund statements).arrow_forwardThe City of Algonquin maintains its books to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations: Deferred inflows of resources—property taxes of $73,500 at the end of the previous fiscal year were recognized as property tax revenue in the current year's Statement of Revenues, Expenditures, and Changes in Fund Balance. The City levied property taxes for the current fiscal year in the amount of $13,789,400. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $309,200 is thought to be uncollectible, $365,000 would likely be collected during the 60-day period after the end of the fiscal year, and $52,800 would be collected after that time. The City had recognized the maximum of property taxes allowable under modified accrual accounting. In addition to the expenditures…arrow_forward

- The schedule of capital assets has a significant impact on the reconciliations between fund and government‐wide statements. The schedule that follows pertaining to governmental capital assets was excerpted from the annual report of Urbana, Illinois (with changed dates): A related schedule indicates the following: Capital outlays $ 3,358,611 Depreciation (2,268,579) $ 1,090,032 As required by GASB Statement No. 34, the annual report includes reconciliations between: (1) total fund balance, governmental funds (per the funds statements), and net position of governmental activities (per the government‐wide statements); and (2) net change in fund balance, governmental funds (per the funds statements), and change in net position of governmental activities (per the government‐wide statements). In what way would the data provided in the accompanying schedules be incorporated into the two reconciliations? Be specific. The amount deleted from the equipment account ($452,194) exactly…arrow_forwardPolk County's solid waste landfill operation is accounted for in a governmental fund. Polk used available cash to purchase equipment that is included in the estimated current cost of closure and post-closure care of this operation. How would this purchase affect the asset amount in Polk's governmental capital assets and the liability amount in Polk's government-wide financial statements? Asset Amount Liability Amount A.) Increase Decrease B.) Increase No effect C.) No effect Decrease D.) No effect No effectarrow_forwardPrepare CORIS RA Statement of Cash Flow for the year ended December 31, 2020arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education