Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:uestion

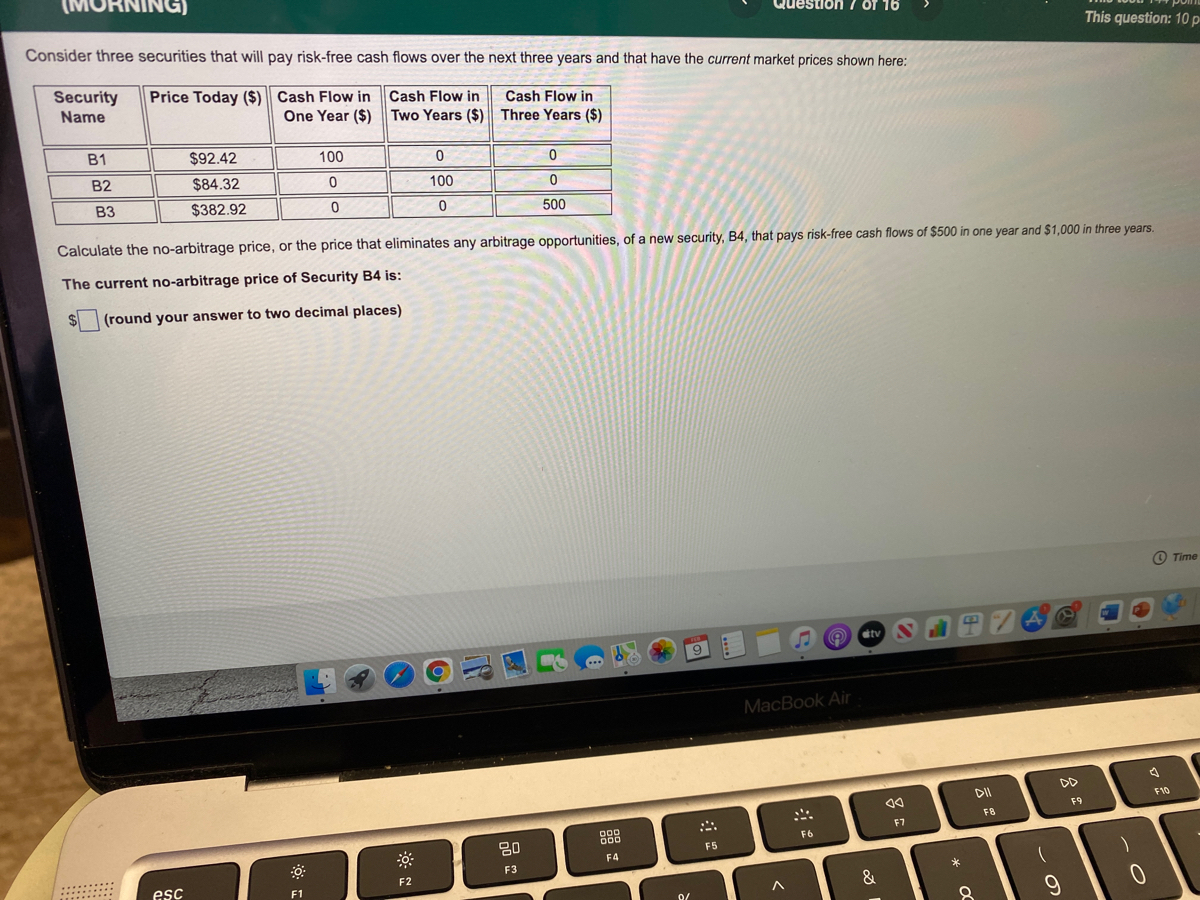

Consider three securities that will pay risk-free cash flows over the next three years and that have the current market prices shown here:

This question: 10p

Security

Price Today ($) Cash Flow in

Cash Flow in

Cash Flow in

Two Years ($) Three Years ($)

Name

One Year ($)

B1

$92.42

100

B2

$84.32

100

B3

$382.92

500

Calculate the no-arbitrage price, or the price that eliminates any arbitrage opportunities, of a new security, B4, that pays risk-free cash flows of $500 in one year and $1,000 in three years.

The current no-arbitrage price of Security B4 is:

(round your answer to two decimal places)

O Time

tv

9

MacBook Air

DD

DII

F10

F9

F8

888

F7

80

F6

F5

F4

F3

esc

F2

F1

&

* OC

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- You find the following Treasury bond quotes. To calculate the number of years until maturity, assume that it is currently May 2022. All of the bonds have a par value of $1,000 and pay semiannual coupons. Rate ?? 6.252 6.163 Maturity Month/Year May 36 May 41 May 51 Bid 103.5462 104.4952 ?? Asked 103.6340 104.6409 ?? Change Ask Yield +.3015 2.329 +.4293 +.5405 ?? 4.031 In the above table, find the Treasury bond that matures in May 2036. What is the coupon rate for this bond? Note: Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.arrow_forwardUsing the expectations hypothesis theory for the term structure of interest rates, determine the expected return for securities with maturities of two, three, and four years based on the following data. (Input your answers as a percent rounded to 2 decimal places.) 1-year T-bill at beginning of year 1 1-year T-bill at beginning of year 2 1-year T-bill at beginning of year 3 1-year T-bill at beginning of year 4 2-year security 3-year security 4-year security Expected Return % % % Interest Rate 61 98 7% 108arrow_forwardSuppose the quoted futures price for delivery in 1 year is $7.10. The current underlying price is $7 and the continuously compounded interest rate is 5%. The underlying does not pay dividends. How could you make a riskless arbitrage profit? Question 2Answer a. buy futures contracts, short sell the stock and invest in a bank account b. borrow from the bank to buy futures contracts and short sell the stock c. sell futures contracts, borrow and buy the stock d. sell future contacts, short sell the stock and invest in a bank accountarrow_forward

- A non-dividend paying asset is current priced at $25 and the risk-free interest rate is 8% per annum. Today, you enter into a six-month futures contract to buy a unit of this asset. Three months from now the underlying price has fallen to $18 (but note that the interest rate has not moved). Which of the answers below is closest to the fall in the futures price? Use discrete discounting. Question 7Answer a. $6.50 b. $5.50 c. $7.50 d. $4.50arrow_forwardUse the following information to answer. Coupon Payments are annual unless otherwise indicated! Years Face Coupon Market Security Rating Maturity Value Rate Price Treasury 1 $ 1,000 0.00% $ 965.00 Treasury 3 $ 1,000 1.90% $ 939.06 Treasury 5 $ 1,000 4.30% $ 932.42 Treasury 10 $ 1,000 6.80% $ 1,007.12 Treasury 15 $ 1,000 6.60% $ 908.25 Corp A A 5 $ 1,000 8.10% $ 990.00 Corp B BB 10 $ 1,000 7.90% $ 859.88 Corp C AA 15 $ 1,000 7.00% $ 660.00 What is the default risk premium for a BB debt security (round to two places)arrow_forwardFixed Income Securities4. Today is t = 0. You have just bought a five-year zero-coupon Treasurybond with $100 face value. You paid $80.(a) What is the annually compounded yield to maturity on the bond?(b) Suppose that yields at all maturities decrease to 2% immediately after you havepurchased the bond. Calculate the annualized holding period return if you sellthe bond one year after you have purchased it, at t = 1.(c) What is the annually compounded yield to maturity on the bond at t = 1?arrow_forward

- You find the following Treasury bond quotes. To calculate the number of years until maturity, assume that it is currently May 2022. All of the bonds have a par value of $1,000 and pay semiannual coupons. Rate ?? 6.152 6.153 Maturity Month/Year May 35 May 38 May 44 Bid 103.4586 104.4926 ?? Yield to maturity Asked 103.5314 % 104.6383 ?? Change Ask Yield +.3274 5.959 ?? 3.991 In the above table, find the Treasury bond that matures in May 2038. What is your yield to maturity if you buy this bond? Note: Do not round Intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16. +.4269 +.5379arrow_forwardyou are considering investing in a four year security which pays 6,000 in one year. 6,000 in two years, 6,000 in 3 years and 17,500 in 4 years. the security currently trades at a price of of 18,483.77. What is the yield to maturity of the security? What is duration?arrow_forwardConsider a long-term, zero coupon bond that has a face value of $100,000 and matures in thirteen years. If you require a return of 4.52%, what are you willing to pay for the instrument today? $56,286.96 $53,852.81 $95,675.47 $177,661.05arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education