Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

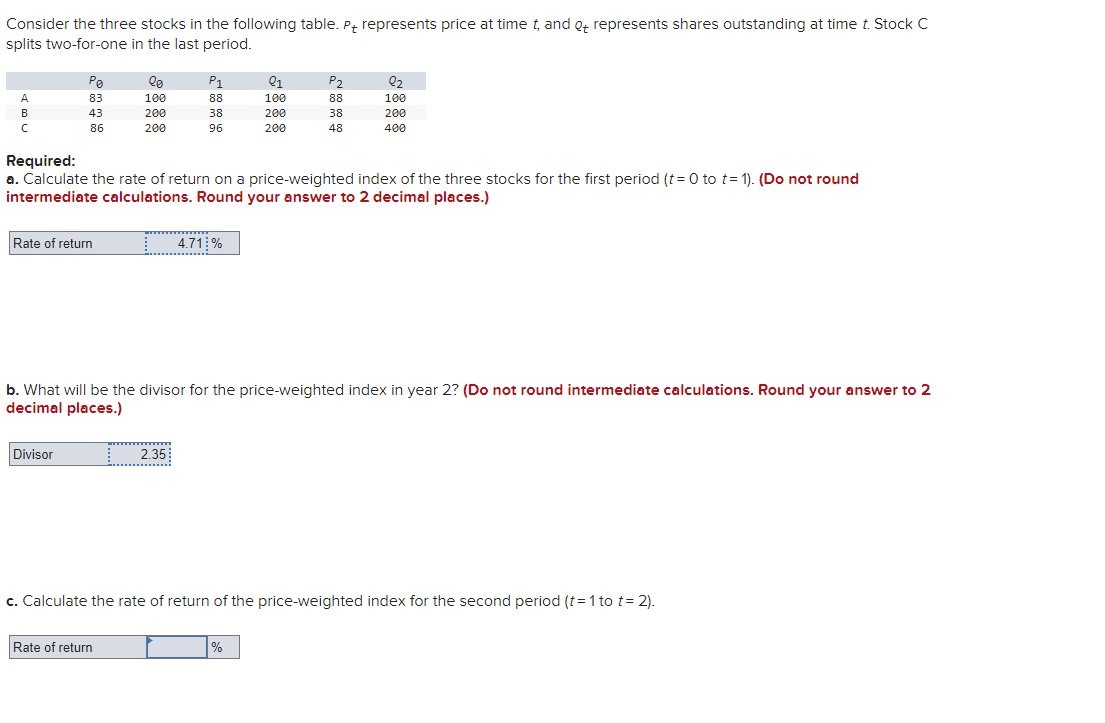

Transcribed Image Text:Consider the three stocks in the following table. P+ represents price at time t, and ot represents shares outstanding at time t. Stock C

splits two-for-one in the last period.

A

B

с

Po

83

43

86

Rate of return

Divisor

lo

100

200

200

Rate of return

L

P1

88

38

96

Required:

a. Calculate the rate of return on a price-weighted index of the three stocks for the first period (t=0 to t= 1). (Do not round

intermediate calculations. Round your answer to 2 decimal places.)

2.35

4.71%

……....

01

100

200

200

b. What will be the divisor for the price-weighted index in year 2? (Do not round intermediate calculations. Round your answer to 2

decimal places.)

P₂

88

38

48

%

2₂

100

200

400

c. Calculate the rate of return of the price-weighted index for the second period (t = 1 to t=2).

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- What is the expected return of Stock B given the information below about its returns across future states of nature? Enter return in decimal form, rounded to 4th digit, as in "0.1234"arrow_forwardConsider the three stocks in the following table. Pt represents price at time t, and Qt represents shares outstanding at time t. Stock C splits two-for-one in the last period. A B с Po 81 41 82 Rate of return 20 100 200 200 Divisor P1₁ 86 36 92 21 100 200 200 Required: a. Calculate the rate of return on a price-weighted index of the three stocks for the first period (t = 0 to t= 1). (Do not round intermediate calculations. Round your answer to 2 decimal places.) % P2 86 36 46 Q2 100 200 400 b. What will be the divisor for the price-weighted index in year 2? (Do not round intermediate calculations. Round your answer to 2 decimal places.)arrow_forwardb) Suppose that you observe the following information in Table 2 for stocks A and B: Table 2 Expected Return (%) 11% Stock Beta A 0.8 В 14% 1.5 The risk-free rate of return is 6% and the expected rate of return on the market index is 12%. Using the Single-Index Model, calculate the alpha of both stocks. Show your calculations. Explain what the alpha of the single-factor model represents and interpret your results.arrow_forward

- pm.3arrow_forward6arrow_forwardConsider the three stocks in the following table. Pt represents price at time t, and Qt represents shares outstanding at time t. Stock C splits two-for-one in the last period. A B C Po 82 42 84 Rate of return 00 100 Divisor 200 200 P1 87 37 94 01 100 200 200 % P2 87 Required: a. Calculate the rate of return on a price-weighted index of the three stocks for the first period (t = 0 to t= 1). (Do not round intermediate calculations. Round your answer to 2 decimal places.) 370 47 92 100 200 400 b. What will be the divisor for the price-weighted index in year 2? (Do not round intermediate calculations. Round your answer to 2 decimal places.) c. Calculate the rate of return of the price-weighted index for the second period (t=1 to t=2).arrow_forward

- Consider the three stocks in the following table. Pt represents price at time t, and Qt represents shares outstanding at time t. Stock C splits two-for-one in the last period. ABC Po 86 46 92 le 100 200 200 Rate of return P1 91 41 102 Q1 100 1.89 % 200 200 P2 91 41 51 Required: a. Calculate the rate of return on a price-weighted index of the three stocks for the first period (t = 0 to t = 1). (Do not round intermediate calculations. Round your answer to 2 decimal places.) 22 100 200 400arrow_forwardProblem 2-12 (Algo) Consider the three stocks in the following table. Pt represents price at time t, and Qt represents shares outstanding at time t. Stock C splits two for one in the last period. Stock Po A B P1 01 P2 02 00 140 145 145 145 145 145 135 290 130 290 130 290 270 290 280 290 145 580 C Required: Calculate the first-period rates of return on the following indexes of the three stocks (t = 0 to t = 1): Note: Do not round intermediate calculations. Round your answers to 2 decimal places. a. A market-value-weighted index. b. An equally weighted index. a. Rate of return b. Rate of return % %arrow_forwardConsider the following information: Stock Return if Market Return Is: Stock –13% 10% A 0 14 B –5 21 C –25 36 D 10 8 E 15 -10 What is the beta of each of the stocks? (Leave no cells blank - be certain to enter "0" wherever required. Use decimals, not percents, in your calculations. A negative value should be indicated by a minus sign. Round your answers to 1 decimal place.) Stock Beta A B C D Earrow_forward

- Consider the three stocks in the following table. Pt represents price at time t, and Qt represents shares outstanding at time t. Stock C splits two-for-one in the last period (t=2). Po A 100 B 60 C 120 Qo 100 200 200 P₁ 105 55 130 Rate of return b. An equally weighted index. Rate of return Q₁ 100 200 200 % P2 % 105 55 65 Calculate the first-period rates of return on the following indexes of the three stocks (t = O to t = 1): (Do not round intermediate calculations. Round your answers to 2 decimal places.) a. A market value-weighted index. Q2 100 200 400arrow_forwardConsider the three stocks in the following table. Pt represents price at time t, and Qt represents shares outstanding at time t. Stock C splits two for one in the last period. Stock A B C Po 90 45 80 90 425 450 650 a. Rate of return b. New divisor c. Rate of return P1 95 40 90 91 425 450 650 % P2 Required: a. Calculate the rate of return on a price-weighted index of the three stocks for the first period (t = 0 to t= 1). Note: Do not round intermediate calculations. Round your answer to 2 decimal places. b. Calculate the new divisor for the price-weighted index in year 2. Note: Do not round intermediate calculations. Round your answer to 2 decimal places. c. Calculate the rate of return for the second period (t=1 to t = 2). Note: Round your answer to 2 decimal places. % 92 425 450 95 40 45 1,300arrow_forwardWhat is the reward-to-risk ratio for Stock X, in decimal form? Round your answer to 4 decimal places (example: if your answer is .03579, you should enter .0358). Margin of error for correct responses: +/- .0005. expected return (implied by market price) Beta Stock X 9.6% 1.46 S&P500 12% ? T-bills 4% ?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education