Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

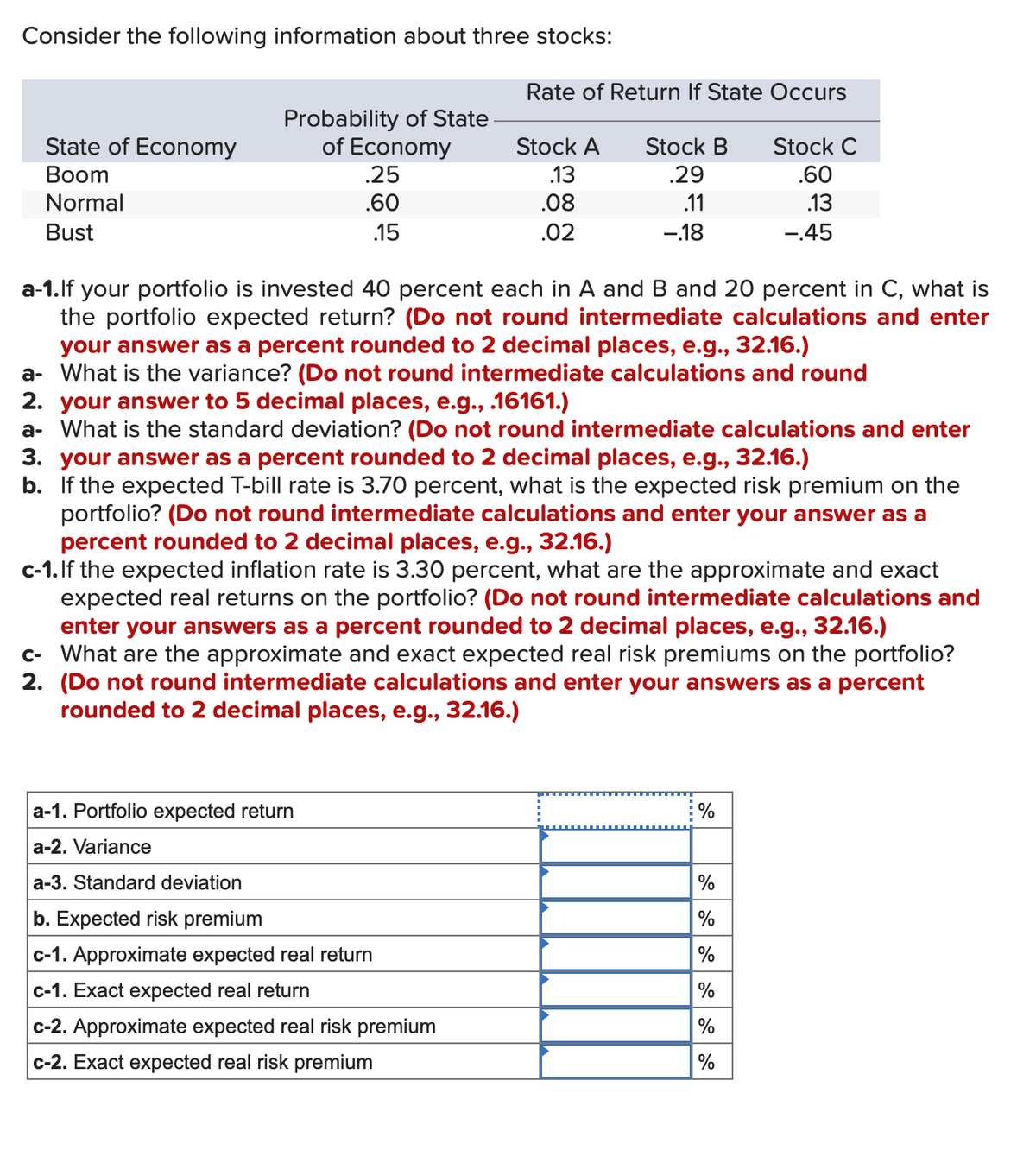

Transcribed Image Text:Consider the following information about three stocks:

Rate of Return If State Occurs

Probability of State

of Economy

.25

State of Economy

Stock A

Stock B

Stock C

Вoom

.13

.29

.60

Normal

.60

.08

.11

.13

Bust

.15

.02

-18

-45

a-1.lf your portfolio is invested 40 percent each in A and B and 20 percent in C, what is

the portfolio expected return? (Do not round intermediate calculations and enter

your answer as a percent rounded to 2 decimal places, e.g., 32.16.)

a- What is the variance? (Do not round intermediate calculations and round

2. your answer to 5 decimal places, e.g., .16161.)

a- What is the standard deviation? (Do not round intermediate calculations and enter

3. your answer as a percent rounded to 2 decimal places, e.g., 32.16.)

b. If the expected T-bill rate is 3.70 percent, what is the expected risk premium on the

portfolio? (Do not round intermediate calculations and enter your answer as a

percent rounded to 2 decimal places, e.g., 32.16.)

c-1. If the expected inflation rate is 3.30 percent, what are the approximate and exact

expected real returns on the portfolio? (Do not round intermediate calculations and

enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.)

c- What are the approximate and exact expected real risk premiums on the portfolio?

2. (Do not round intermediate calculations and enter your answers as a percent

rounded to 2 decimal places, e.g., 32.16.)

a-1. Portfolio expected return

%

a-2. Variance

a-3. Standard deviation

%

b. Expected risk premium

c-1. Approximate expected real return

%

c-1. Exact expected real return

c-2. Approximate expected real risk premium

%

c-2. Exact expected real risk premium

%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Suppose that many stocks are traded in the market and that it is possible to borrow at the risk-free rate, rƒ. The characteristics of two of the stocks are as follows: Stock Expected Return Standard Deviation A 8% 55% B 4% 45% Correlation = −1 Required: a. Calculate the expected rate of return on this risk-free portfolio? (Hint: Can a particular stock portfolio be formed to create a “synthetic” risk-free asset?) (Round your answer to 2 decimal places.) b. Could the equilibrium rƒ be greater than rate of return?arrow_forwardYou are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Op 1.45 1.20 0.75 1.00 Portfolio: X Y Z Market Risk-free Rp 11.00% 10.00 8.10 10.40 5.20 Information ratio Op 33.00% 28.00 18.00 23.00 0 Assume that the tracking error of Portfolio X is 9.10 percent. What is the information ratio for Portfolio X? Note: A negative value should be indicated by a minus sign. Do not round intermediate calculations. Round your answer to 4 decimal places. 02148 0arrow_forwardYou are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio Y Z Market Risk-free Rp 16.00% бр 32.00% 15.00 27.00 7.30 17.00 11.30 5.80 22.00 0 Bp 1.90 1.25 0.75 1.00 0 Assume that the tracking error of Portfolio X is 13.40 percent. What is the information ratio for Portfolio X? Note: A negative value should be indicated by a minus sign. Do not round intermediate calculations. Round your answer to 4 decimal places. Information ratioarrow_forward

- es Consider the following information on three stocks: State of Economy Boom Normal Bust Probability of State of Economy .20 .40 .40 Rate of Return If State Occurs Stock A .34 .25 .03 Stock B .46 .23 -.25 Stock C .50 .20 - .42 a-1. If your portfolio is invested 35 percent each in A and B and 30 percent in C, what is the portfolio expected return? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) a-2. What is the variance? (Do not round intermediate calculations and round your answer to 5 decimal places, e.g., .32161.) a-3. What is the standard deviation? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b. If the expected T-bill rate is 4.50 percent, what is the expected risk premium on the portfolio? (Do not round intermediate calculations abd enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) c-1. If the expected inflation rate…arrow_forwardVijayarrow_forwardYou are exploring the use of APT in making investment choices. You have identified three factors labelled F1, F2, and F3 with corresponding risk premia RP1 = 3%, RP2 = 6%, and RP3 = 2%. A stock with ticker ABC has historically shown returns which have followed the equation: rABC=0.14+.50F1+1.20F2+.8F3+eABC What is the equilibrium rate of return for stock ABC using the APT, if the T-bill rate is 5%?arrow_forward

- Stocks A and B have the following probability distributions of expected future returns: Probability A B 0.1 (7 %) (26 %) 0.1 3 0 0.5 14 22 0.2 20 26 0.1 36 50 Calculate the expected rate of return, , for Stock B ( = 14.20%.) Do not round intermediate calculations. Round your answer to two decimal places. % Calculate the standard deviation of expected returns, σA, for Stock A (σB = 18.68%.) Do not round intermediate calculations. Round your answer to two decimal places. % Now calculate the coefficient of variation for Stock B. Do not round intermediate calculations. Round your answer to two decimal places. Is it possible that most investors might regard Stock B as being less risky than Stock A? If Stock B is less highly correlated with the market than A, then it might have a higher beta than Stock A, and hence be more risky in a portfolio sense. If Stock B is more highly correlated with the market than A, then it might have a higher…arrow_forwardVijayarrow_forwardConsidering the attached set of securities and portfolio returns: Find the combination of the weights that minimizes CV of the portfolio. How does the CV of the optimal portfolio compare with the CVs of its constituents?arrow_forward

- Read the information for 3 stocks X, Y and Z below. Rate of return when state occurs (For Stock X, Y, and Z) State of Economy Probability of State Stock X Stock Y Stock Z Boom 0.3 0.4 0.45 0.6 Normal 0.5 0.2 0.15 0.08 Recession 0.2 0 -0.3 -0.4 If your portfolio includes 35 percent of X, 40 percent of Y and 25 percent of Z, answerthe following questions: (a) Calculate the portfolio expected return.(b) Calculate the variance and the standard deviation of the portfolio (c) If the expected T-bill rate is 3.80 percent, calculate the expected risk premiumon the portfolio.arrow_forwardParts A-C have already been answered, looking for answer D.arrow_forwardWhat is the required return for each stock? What is required return for stock B? Scenario Probability Stock A Stock B Market Risk-free rate Bust 0.25 -0.15 -0.05 Normal 0.55 0.2 0.1 Boom 0.2 0.4 0.3 Beta 1.2 0.9 Expected return 0.13 0.05arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education