FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

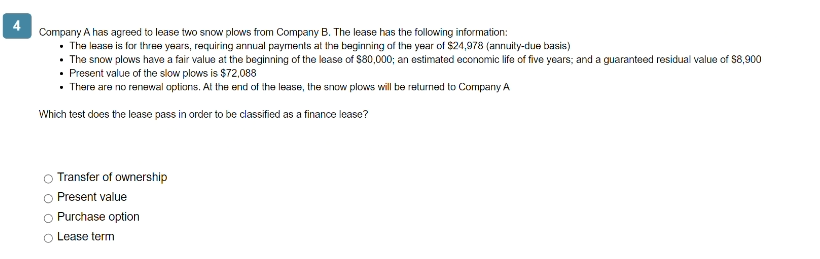

Transcribed Image Text:Company A has agreed to lease two snow plows from Company B. The lease has the following information:

• The lease is for three years, requiring annual payments at the beginning of the year of $24,978 (annuity-due basis)

• The snow plows have a fair value at the beginning of the lease of $80,000; an estimated economic life of five years; and a guaranteed residual value of $8,900

• Present value of the slow plows is $72,088

• There are no renewal options. At the end of the lease, the snow plows will be returned to Company A

Which test does the lease pass in order to be classified as a finance lease?

Transfer of ownership

O Present value

Purchase option

Lease term

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- On January 1, Year 1, Indiana Water (lessor) and Koontz Lake (lessee) agreed to a 9-year lease for equipment that has an economic life of 10 years. Koontz Lake made its first annual payment on January 1, Year 2 for $3,000. Thereafter, eight more annual payments are due. Title reverts to Koontz Lake at the end of the lease term. The equipment has a fair market value at the lease inception date of $20,500. The discount rate is 5%. Which one of the lease conditions below is not met? Select one: A. The present value of the minimum lease payments is at least 90% of the leased asset's value. B. The lease agreement contains a bargain purchase option. C. The lease term is at least 75% of the asset's remaining economic life. D. The lease agreement transfers ownership of the leased asset.arrow_forwardFederated Fabrications leased a tooling machine on January 1, 2024, for a three-year period ending December 31, 2026. . The lease agreement specified annual payments of $34,000 beginning with the first payment at the beginning of the lease, and each December 31 through 2025. . The company had the option to purchase the machine on December 30, 2026, for $43,000 when its fair value was expected to be $58,000, a sufficient difference that exercise seems reasonably certain. . The machine's estimated useful life was six years with no salvage value. Federated was aware that the lessor's implicit rate of return was 12%. Note: Use tables, Excel, or a financial calculator. (EV of $1. PV of $1. FVA of $1. PVA of $1. FVAD of $1 and PVAD of $1) Required: 1. Calculate the amount Federated should record as a right-of-use asset and lease llability for this finance lease. 2. Prepare an amortization schedule that describes the pattern of interest expense for Federated over the lease term. 3. Prepare…arrow_forwardFederated Fabrications leased a tooling machine on January 1, 2024, for a three-year period ending December 31, 2026 • The lease agreement specified annual payments of $47,000 beginning with the first payment at the beginning of the lease, and each December 31 through 2025. The company had the option to purchase the machine on December 30, 2026, for $56,000 when its fair value was expected to be $71,000, a sufficient difference that exercise seems reasonably certain. • The machine's estimated useful life was six years with no salvage value. Federated was aware that the lessor's implicit rate of return was 12%. Note: Use tables, Excel, or a financial calculator. (FV of $1. PV of $1. EVA of $1. PVA of $1. EVAD of $1 and PVAD of $1) Required: 1. Calculate the amount Federated should record as a right-of-use asset and lease liability for this finance lease. 2. Prepare an amortization schedule that describes the pattern of interest expense for Federated over the lease term. 3. Prepare the…arrow_forward

- Teal Mountain Company is negotiating to lease a piece of equipment to MTBA, Inc. MTBA requests that the lease be for 9 years. The equipment has a useful life of 10 years. Teal Mountain wants a guarantee that the residual value of the equipment at the end of the lease is at least $4,000. MTBA agrees to guarantee a residual value of this amount though it expects the residual value of the equipment to be only $2,500 at the end of the lease term.If the fair value of the equipment at lease commencement is $60,000, what would be the amount of the annual rental payments Teal Mountain demands of MTBA, assuming each payment will be made at the beginning of each year and Teal Mountain wishes to earn a rate of return on the lease of 6%? (For calculation purposes, use 5 decimal places as displayed in the factor table provided and round final answer to 0 decimal places, e.g. 5,275.)arrow_forwardABC Company leased equipment to Best Corporation under a lease agreement that qualifies as a direct finance lease. The cost of the asset is OMR 22,000. The lease contains a bargain purchase option that is effective at the end of the fifth year. The expected economic life of the asset is five years. The lease term is 5 years. The asset is expected to have a residual value of OMR 2,000 at the end of ten years. Using the straight-line method, what would Best record as annual depreciation? Select one: a. OMR 2,000 b. OMR 4,500 c. OMR 5,000 d. OMR 4,000arrow_forwardWildhorse Limited has signed a lease agreement with Lantus Corp. to lease equipment with an expected lifespan of eight years, no estimated salvage value, and a cost to Lantus, the lessor of $199,000. The terms of the lease are as follows: ● The lease term begins on January 1, 2019, and runs for 5 years. ● The lease requires payments of $45,359 at the beginning of each year starting January 1, 2019. ● At the end of the lease term, the equipment is to be returned to the lessor. ● Lantus’ implied interest rate is 7%, while Wildhorse’s borrowing rate is 8%. Wildhorse uses straight-line depreciation for similar equipment. The year-end for both companies is December 31. Assume that both companies follow ASPE. (a)Determine the present value of the minimum lease payments Ans 199,000 B.) Prepare Wildhorse’s lease amortization schedule using the effective interest method. (Round answers to 0 decimal places, e.g. 5,275.) Date Payment Interest Principal Balance…arrow_forward

- Gordon Inc., a private company that follows ASPE, entered into a lease agreement with Canada Leasing Corporation to lease a warehouse for six years. Annual lease payments are $21,000, payable at the beginning of each lease year. Gordon Inc. signed the lease agreement on January 1, 2021, and made the first payment on that date. At the end of the lease, the machine will revert back to Canada Leasing Corporation. The normal useful life of the warehouse is 10 years. At the time of the lease, the warehouse could be purchased for $108,000. Gordon does not know the implicit rate of the lease; Gordon's incremental borrowing rate is 10%. Gordon uses straight-line depreciation for this type of asset. Required: Using the three criteria under ASPE, prove whether this is an operating or capital lease. Prepare a lease amortization schedule for the lease. Round all amounts to the nearest dollar. Prepare the journal entries for 2021 and 2022 for Gordon Inc. Round amounts to the nearest…arrow_forwardMetlock Company leases a building and land. The lease term is 8 years and the annual fixed payments are $840,000. The lease arrangement gives Metlock the right to purchase the building and land for $13,550,000 at the end of the lease. Based on an economic analysis of the lease at the commencement date, Metlock is reasonably certain that the fair value of the leased assets at the end of lease term will be much higher than $13,550,000. What are the total lease payments in this lease arrangement? Total lease payments Click if you would like to Show Work for this question: Open Show Workarrow_forwardLessee enters into a three year lease of equipment and agrees to make the following annual payments at the end of each year 10,000 in year one, 12,000 in year two and 14,000 in year three. Discount rate is approx. 4, 235% and right of use asset is depreciated on a straight line basis over the lease term. What is the value of the lease liability at the end of years 2 & 3?arrow_forward

- Terms of a lease agreement and related facts were: a. Incremental costs of commissions for brokering the lease and consummating the completed lease transaction incurred by the lessor were $5,408. b. The retail cash selling price of the leased asset was $425,000. Its useful life was three years with no residual value. c. The lease term is three years and the lessor paid $425,000 to acquire the asset. d. Annual lease payments at the beginning of each year were $160,000. e. Lessor's implicit rate when calculating annual rental payments was 13%. (FV of $1, PV of $1, FVA of $1, PVA of $1, FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.) Required: 1. Prepare the appropriate entries for the lessor to record the lease and related payments at its beginning, January 1, 2018. 2. Calculate the effective rate of interest revenue after adjusting the net investment by initial direct costs. 3. Record any entry(s) necessary at December 31, 2018, the fiscal year-end.…arrow_forward(Lessor Computations and Entries, Sales-Type Lease with Unguaranteed Residual Value) George Company manufactures a check-in kiosk with an estimated economic life of 12 years and leases it to National Airlines for a period of 10 years. The normal selling price of the equipment is $278,072, and its unguaranteed residual value at the end of the lease term is estimated to be $20,000. National will pay annual payments of $40,000 at the beginning of each year and all maintenance, insurance, and taxes. George incurred costs of $180,000 in manufacturing the equipment and $4,000 in negotiating and closing the lease. George has determined that the collectibility of the lease payments is reasonably predictable,that no additional costs will be incurred, and that the implicit interest rate is 10%.Instructions(a) Discuss the nature of this lease in relation to the lessor and compute the amount of each of the following items.(1) Lease receivable.(2) Sales price.(3) Cost of sales.(b) Prepare a 10-year…arrow_forward6 Company A (lessee) has reached a lease agreement with Company B (assor) to kase a new carpet weaving machine beginning January 1, Year 1. The lease agreement contains the following information • The lease is for five years, requiring annual payments of $10,355.67 at the beginning of the year. • The weaving machine has a fair value at the beginning of the lease of $50,000; an estimated economic life of five years; and a guaranteed residual value of $2,500 (Company A expects that the value will be greater). • Present value of the weaving machine is $47,945.18. • There are no renewal options. At the end of the lease, the weaving machine will be returned to Company B. • Company A depreciates similar equipment that it purchases on a straight-line basis. • Company B sels the annual lease rate al 5% and Company A is aware of the rate. • The lease is a finance lease. COMPANY A LEASE AMORTIZATION SCHEDULE ANNUITY-DUE BASIS Annual Lease Payment Date January 1, Year 1 January 1, Year 1 January…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education