Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

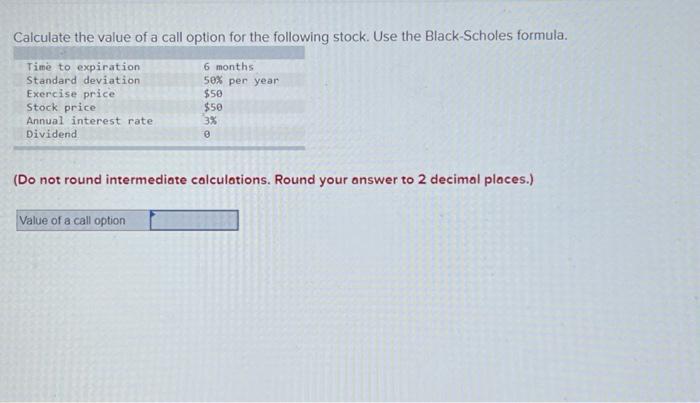

Transcribed Image Text:Calculate the value of a call option for the following stock. Use the Black-Scholes formula.

Time to expiration

Standard deviation

Exercise price

Stock price

Annual interest rate

Dividend

6 months

50% per year

$50

$50

3%

0

(Do not round intermediate calculations. Round your answer to 2 decimal places.)

Value of a call option

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Problem 1. Assume that the interest rate is 5%, contimuously compounded annually, and consider call and put options of both American and European style expiring in 6 months on non-dividend paying stock. For each of the following scenarios, check if you can find an arbitrage opportunity and, if you can, describe it: (i) The strike price of a European put option is $3 and the option is traded at $4. (ii) The shares are traded at $3 and the American call option is traded at $3.20.arrow_forwardUse the Black-Scholes formula for the following stock: Time to expiration 6 months Standard deviation 60% per year Exercise price $57 Stock price $57 Annual interest rate 3% Dividend 0 Recalculate the value of the call with the following changes: a. Time to expiration 3 months b. Standard deviation 25% per year c. Exercise price $64 d. Stock price $64 e. Interest rate 6% Select each scenario independently. Note: Round your answers to 2 decimal places.arrow_forwardD4) Finance Calculate the price of a 3-month American put option on a non-dividend-paying stock when the stock price is $50, the strike price is $50, the risk-free interest rate is 5% per annum, and the volatility is 25% per annum. Use a binomial tree with a time interval of 1 month.arrow_forward

- Use the Black-Scholes formula to find the value of a call option on the following stock: Time to expiration Standard deviation Exercise price Stock price Annual interest rate Dividend Value of the Call Option 6 months 60% per year $57 $64 38 0arrow_forwardThe stock price of Copious Corp. is currently $30. The stock price 1 year(s) from now will be either $34 or $27. The annual risk-free rate is 1.4%. Using the binomial model, what is the value of a call option with an exercise price of $30 and an expiration date 1 year(s) from now?arrow_forwardPut-Call Parity The current price of a stock is $33, and the annual risk-free rate is 6%. A call option with a strike price of $31 and with 1 year until expiration has a current value of $5.58. What is the value of a put option written on the stock with the same exercise price and expiration date as the call option? Do not round intermediate calculations. Round your answer to the nearest cent. $arrow_forward

- The current price of a non-dividend paying stock is $30. Use a two-step tree to value a European put option on the stock with a strike price of $32 that expires in 6 months. Each step is 3 months, the risk free rate is 896, and u = 1.1 and d = 0.9. O $2.24 $2.44 $2.64 $2.84arrow_forwardUse the Black-Scholes formula for the following stock: Time to expiration 6 months Standard deviation Exercise price Stock price 41% per year $42 $41 Annual interest rate 7% Dividend Calculate the value of a call option. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Value of a call optionarrow_forwardUse the Black-Scholes formula to find the value of the put option using the next data: Stock price: $5.03 Time to expiration: 176 days (365 days in a year) The volatility of a stock return: 65% per year Strike price: $5 Risk-free interest rate: 1% per yeararrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education