Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

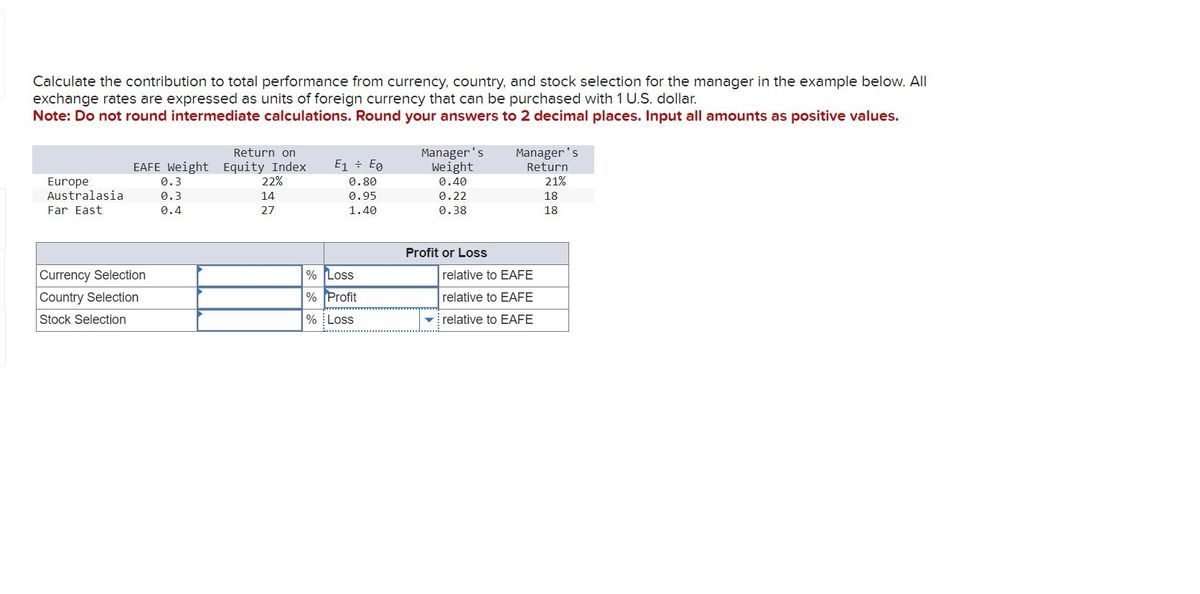

Transcribed Image Text:Calculate the contribution to total performance from currency, country, and stock selection for the manager in the example below. All

exchange rates are expressed as units of foreign currency that can be purchased with 1 U.S. dollar.

Note: Do not round intermediate calculations. Round your answers to 2 decimal places. Input all amounts as positive values.

Europe

Australasia

Far East

Return on

EAFE Weight Equity Index

22%

14

27

Currency Selection

Country Selection

Stock Selection

0.3

0.3

0.4

E₁ ÷ Eo

0.80

0.95

1.40

% Loss

% Profit

% Loss

Manager's

Weight

0.40

0.22

0.38

Profit or Loss

Manager's

Return

21%

18

18

relative to EAFE

relative to EAFE

relative to EAFE

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- You have the following quotations for the Chinese yuan (CNY) and the Australian dollar (A$) at the HSBC Bank in China and National Australia Bank in Australia. Can you make a locational arbitrage profit? If yes, calculate the arbitrage profit if you have A$1.76 million or CNY3.42 million. (enter the whole number without sign or symbol) Currency HSBC in China National Australia Bank in Australia Bid Ask Bid Ask Chinese yuan A$0.2010 A$0.2230 A$0.2420 A$0.2673 Australian dollar CNY4.4221 CNY4.9632 CNY3.8255 CNY4.1641arrow_forwardQuestion 3 Assuming the following quotes, calculate how a market trader at Citibank with $1,000,000 can make an intermarket arbitrage profit.: Citibank quotes U.S. dollar per pound: National Westminster quotes euros per pound: Deut $1.5900/£ €1.2000/£ quotes U.S. dollar per euro: $0.7550/€ Question 4 The Venezuelan government officially floated the Venezuelan bolivar (Bs) in February of 2002. Within weeks, its value had moved from the pre-float fix of BS774/S to Bs1028/S. a. Is this a devaluation or depreciation? b. By what percentage did its value change?arrow_forwardThe following table shows PPP exchange rates (the price of 1 U.S. dollar in units of the foreign currency) for several countries, determined based on the Big Mac Index. PPP exchange rate (1USS=) United States (US$) Argentina (Peso) Australia (A$) Brazil (Real) Britain (£) Canada (C$) Chile (Peso) China (Yuan) В.75 1.17 2.33 0.61 1.12 469 3.54 a. According to this data, what are the predicted exchange rates between the following countries? i. Argentina and Australia ii. Brazil and Canada iii. Chile and China iv. China and Canada b. Suppose that a Canadian dollar buys more silver in Australia than it buys in Mexico. What does purchasing-power parity imply should happen?arrow_forward

- What is the expected percentage change in the value of the foreign currency (e) if you combine all three techniques, which are equally weighted? Method Technical forecasting Fundamental forecasting Market-based forecasting O 0.3% O 4.6% O 4.7% 2.0% Forecasted e 2% -4% 8%arrow_forwardSuppose that you are a currency speculator, based in the U.S., att January 1st, the spot rate for the Canadian dollar is $0.68. This is have C$160,000.00 to use on these positions. Suppose that on February 10th, the Canadian dollar depreciates (a In order to purchase C$160,000.00 in spot market, you will need $107,200.00 alize on a possible depreciation of the Canadian dollar (C$). On t which futures contracts for Canadian dollars are being sold. You $139,360.00 $128,640.00 $150,080.00 d) to $0.67 in the spot market. (U.S. dollars) for the exchange.arrow_forwardPlease use the data below, to answer the following question. BigMac price in the US BigMac price in Mexico Current Exchange Rate O overvalued by 14.29% O undervalued by 14.29% O overvalued by 12.50% O undervalued by 12.50% USD 3.50 12 MXN 80 Based on PPP, the MXN is 1 USD - MXN 20 140 15 16 (2 hparrow_forward

- H3. The Central Bank of the Bahamas pegs the Bahamian Dollar to the United States Dollar at a price of 1 BSD per USD. As an analyst for XYZ Consulting Inc., you have been asked to predict the behavior of key macroeconomic variables in the Bahamas for different policy scenarios. Using all the appropriate diagrams, your analysis must describe the Bahamian money and output markets, as well as the foreign exchange market. To perform this task, you must assume that prices are sticky: fixed in the short-run and flexible in the long-run. The scenarios are: a) A temporary restrictive monetary policy in the Bahamas. b) A temporary restrictive fiscal policy in the Bahamas.arrow_forwardYou Answered Correct Answer Samuel Samosir works for Peregrine Investments in Jakarta, Indonesia. He focuses his time and attention on the U.S. dollar/Singapore dollar ($/S$) cross- rate. The current spot rate is $1.39/S$. After considerable study, he has concluded that the Singapore dollar will appreciate versus the U.S. dollar in the coming 90 days, probably to about $1.44/S$. He is considering trading options to profit and has the following options on the Singapore dollar to choose from Option choices on the Singapore dollar: Strike price (US$/Singapore dollar) Premium (US$/Singapore dollar) -0.132 Call on S$ -0.047 $1.371 $0.047 Put on S$ $1.37 Samuel decides to buy call options in Singapore dollars. What will be Samuel's profit/loss if the ending spot rate is $1.286/S$ in 90 days? Keep all decimal places. $0.006arrow_forwardThe table below contains the average returns, standard deviation of returns and correlation of returns with US indexfor different countries. All data are in US dollar terms. The US T-Bill rate is 3%. Determine which of thesecountries are suitable for a US based investor to diversifv into. Show the necessarv calculationsUS T-Bill Rate %3arrow_forward

- subject:international finance Most foreign currencies in the world are stated in terms of the number of units of foreign currency needed to buy one dollar Required a)Convert the following indirect quotes to direct quotes. I. Euro: €1.22/$ (indirect quote) II. Russia: Rub 30/$ (indirect quote) III. Canada: C$ 1.39/$ (indirect quote) IV. Denmark: DKr6.08/$ (indirect quote) b)Convert the following direct quotes to indirect quotes. I. Euro: $ 0.865/€ (direct quote) II. Russia: $ 0.050/ Rub (direct quote) III. Canada: $ 0.85/C$ (direct quote) IV. Denmark: $ 0.608/ DKr (direct quote) c)Define the spot transaction and outright forward transaction.arrow_forwardABC Bank quotes the following for the British pound and the New Zealand dollar: Quoted Bid Price Quoted Ask Price Value of a British pound (£) in $ $1.61 $1.62 Value of a New Zealand dollar (NZ$) in $ $.55 $.56 Value of a British pound in New Zealand dollars NZ$2.95 NZ$2.96 Assume you have $10,000 to conduct triangular arbitrage. What is your profit from this strategy? What is your profit?arrow_forwardQuestion 12 Given the following cross currency rates, identify an arbitrage trade and show the profit if you start with $1,000. (USD = U.S. dollar, SGD = Singapore dollar, CHF = Swiss franc) SGD:USD CHF:USD SGD:CHF 1,045.46 3.00 1.50 2.20arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education