FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

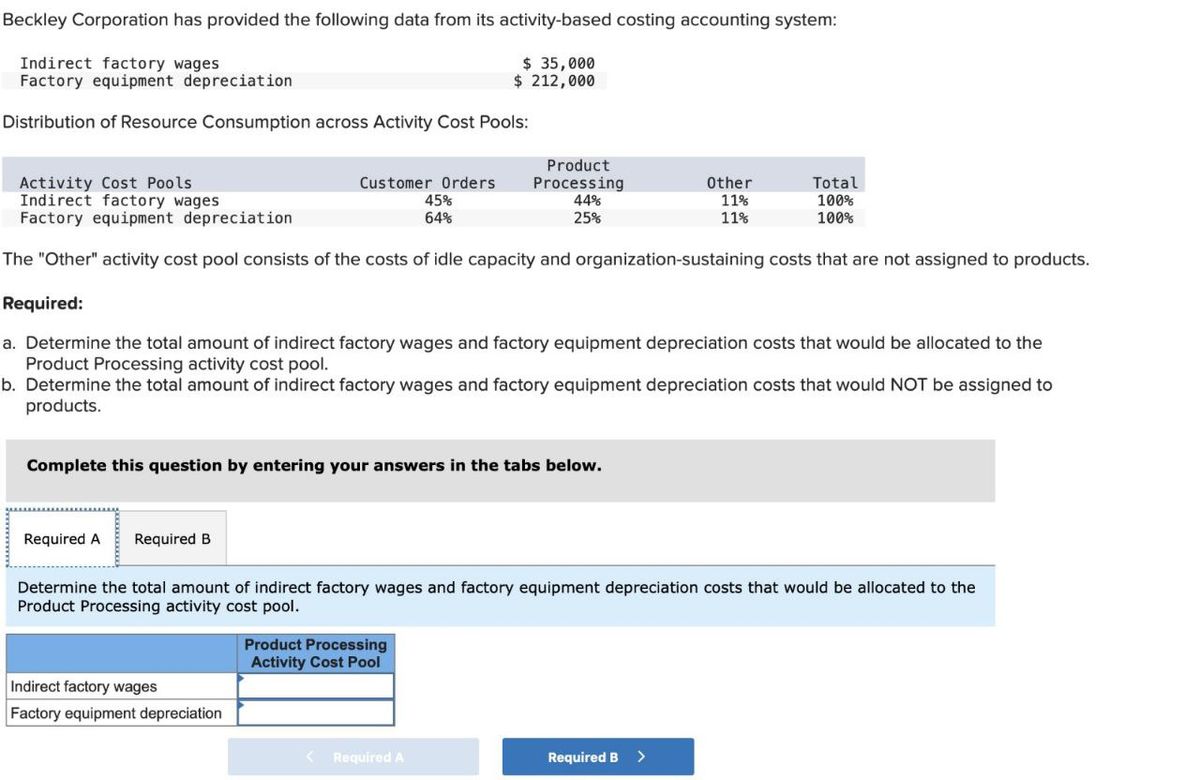

Transcribed Image Text:Beckley Corporation has provided the following data from its activity-based costing accounting system:

Indirect factory wages

Factory equipment depreciation

$ 35,000

$ 212,000

Distribution of Resource Consumption across Activity Cost Pools:

Activity Cost Pools

Indirect factory wages

Factory equipment depreciation

Customer Orders

45%

64%

Product

Processing

44%

25%

Other

11%

Total

100%

11%

100%

The "Other" activity cost pool consists of the costs of idle capacity and organization-sustaining costs that are not assigned to products.

Required:

a. Determine the total amount of indirect factory wages and factory equipment depreciation costs that would be allocated to the

Product Processing activity cost pool.

b. Determine the total amount of indirect factory wages and factory equipment depreciation costs that would NOT be assigned to

products.

Complete this question by entering your answers in the tabs below.

Required A

Required B

Determine the total amount of indirect factory wages and factory equipment depreciation costs that would be allocated to the

Product Processing activity cost pool.

Product Processing

Activity Cost Pool

Indirect factory wages

Factory equipment depreciation

Required A

Required B >

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- (Appendix 4B) Direct Method of Support Department Cost Allocation Stevenson Company is divided into two operating divisions: Battery and Small Motors. The company allocates power and general factory costs to each operating division using the direct method. Power costs are allocated on the basis of the number of machine hours and general factory costs on the basis of square footage. Support department cost allocations using the direct method are based on the following data: Operating Divisions Overhead costs Machine hours Square footage Direct labor hours Required: Battery Support Departments Small Motors Power $160,000 2,000 1,000 General Factory Battery $430,000 $163,000 2,000 8,000 Power 1,500 1. Calculate the allocation ratios for Power and General Factory. (Note: Carry these calculations out to four decimal places, if necessary.) General Factory 0.8000 ✓ 0.2727 X 7,500 18,000 Small Motors $84,600 2,000 20,000 60,000 0.2000 X 0.7273 2. Allocate the support service costs to the…arrow_forwardWeldon Corporation has provided the following data from its activity-based costing accounting system: Indirect factory wages Factory equipment depreciation Distribution of Resource Consumption across Activity Cost Pools: $ 340,000 $ 240,000 Customer Orders 25% 40% Product Processing 65% 40% Activity Cost Pools Indirect factory wages Factory equipment depreciation The "Other" activity cost pool consists of the costs of idle capacity and organization-sustaining costs that are not assigned to products. How much indirect factory wages and factory equipment depreciation cost would NOT be assigned to products using the activity-based costing system? Other 10% 20% Total 100% 100%arrow_forwardLion Corporation uses an activity-based costing system to assign overhead costs to products. In the first stage, two overhead costs--equipment depreciation and supervisory expense-are allocated to three activity cost pools--Machining, Order Filling, and Other--based on resource consumption. Data to perform these allocations appear below: Overhead costs: Equipment depreciation Supervisory expense Equipment depreciation Distribution of Resource Consumption Across Activity Cost Pools: Product C9 $ 47,000 Product UO $ 6,000 Total Supervisory expense 0.60 Activity Cost Pools O $18.00 per MH O $5.30 per MH O $2.82 per MH O $3.18 per MH Mac 0.60 In the second stage, Machining costs are assigned to products using machine- hours (MHS) and Order Filling costs are assigned to products using the number of orders. The costs in the Other activity cost pool are not assigned to products. Activity data for the company's two products follow: 6,900 Order Filling 3,100 0.10 MHS (Machining) 10,000 b.20 200…arrow_forward

- karan subject-Accountingarrow_forwardLarner Corporation is a diversified manufacturer of industrial goods. The company's activity-based costing system contains the following six activity cost pools and activity rates: Activity Cost Pool Labor-related Machine-related Machine setups Production orders Shipments $ 140.00 per shipment General factory $ 7.00 per direct labor-hour Cost and activity data have been supplied for the following products: Direct labor-hours Machine-hours Machine setups Production orders Shipments Activity Rates $7.00 per direct labor-hour Direct materials cost per unit Direct labor cost per unit Number of units produced per year $7.00 per machine-hour $30.00 per setup $200.00 per order Unit product cost Total Expected Activity J78 378 1,200 2,200 6 5 7 B52 30 50 1 1 1 Required: Compute the unit product cost of each product listed above. (Do not round intermediate calculations. Round your answers to 2 decimal places.) B52 378 $5.50 $ 4.75 4,000 B52 $32.00 $9.00 100arrow_forwardA company has provided the following data from its activity-based costing accounting system: Indirect factory wages $552,000 Factory equipment depreciation $332,000 Distribution of Resource Consumption across Activity Cost Pools: 14 Activity Cost Pools Customer Product Orders Processing Other Total Indirect factory wages 55% 35% 10% 100% Factory equipment depreciation 30% 50% 20% 100% The "Other" activity cost pool consists of the costs of idle capacity and organization- sustaining costs, How much indirect factory wages and factory equipment depreciation cost would NOT be assigned to products using the activity-based costing system? Multiple Choice $552,000 $332.000 $121,600 $0arrow_forward

- Nonearrow_forwardMeester Corporation has an activity-based costing system with three activity cost pools--Machining, Order Filling, and Other. In the first stage allocations, costs in the two overhead accounts, equipment depreciation and supervisory expense, are alloceted to three activity cost pools based on resource consumption, Data used in the first stage allocations follow Overhead costs: Equipment depreciation Supervisory expense $ 81,300 $ 2,200 Distribution of Resource Consumption Across Activity Cost Pools: Activity Cost Pools Machining Order Filling Other Equipment depreciation Supervisory expense 0.50 0.30 0. 20 e. 30 e.50 0.20 Mechining costs are assigned to products using machine-hours (MHs) and Order Filing costs are essigned to products using the number of orders. The costs in the Other activity cost pool are not assigned to products. Activity date for the companve o nroducts follaw You ae sren sharg Skop Share Activity MHs (Machining) Orders (Order Filling) Product Me 1,630 9,780 1,370…arrow_forwardHelm Corporation uses an activity-based costing system with three activity cost pools. The company has provided the following data concerning its costs and its activity-based costing system: Costs: Manufacturing overhead Selling and administrative expenses Total Distribution of resource consumption: Manufacturing overhe Selling and administrative expenses Activity Cost Pools Customer Support 85% 20% Order Size 5% 60% S O $348,000 O $188,500 $29,000 O $84,000 S Other 10% 20% The "Other" activity cost pool consists of the costs of idle capacity and organization-sustaining costs. 480,000 100,000 580,000 You have been asked to complete the first-stage allocation of costs to the activity cost pools. Total 100% 100% How much cost, in total, would be allocated in the first-stage allocation to the Order Size activity cost pool? Next ▸arrow_forward

- Dogarrow_forwardAn activity based costing system is used at Haldeman, SA to assign products overhead costs. First, the two overhead costs of Equipment depreciation and Water expense are allocated to three activity cost pools - Handling, Machining, and Other - based on resource consumption. The information used to perform these allocations is below: Overhead Costs: Equipment depreciation: $50,000 Water expense: $60,000 Distribution of Resource Consumption across Activity Cost Pools: Overhead Cost Activity Cost Pools Handling Machining Other Equipment depreciation 0.28 0.34 0.38 Water expense 0.32 0.22 0.46 The second stage of allocation is done by assigning the Handling costs to products on the basis of orders filled while products are assigned Machining costs based on machine hours. Costs assigned to the Other activity pool are not further assigned to products. Activity information for Haldeman's only two products is below: orders filled machine hours Product LS-157: 3,400 3,400…arrow_forwardwhat is the labor-related activity cost pool per DLH what is the machine-related activity cost pool per MH what is the machine setups activity cost pool per seteup what is the production orders activity cost per order what is the product testing activity cost per test what is the packaging activity cost per package what is the general factory activity cost per DLHarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education