ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

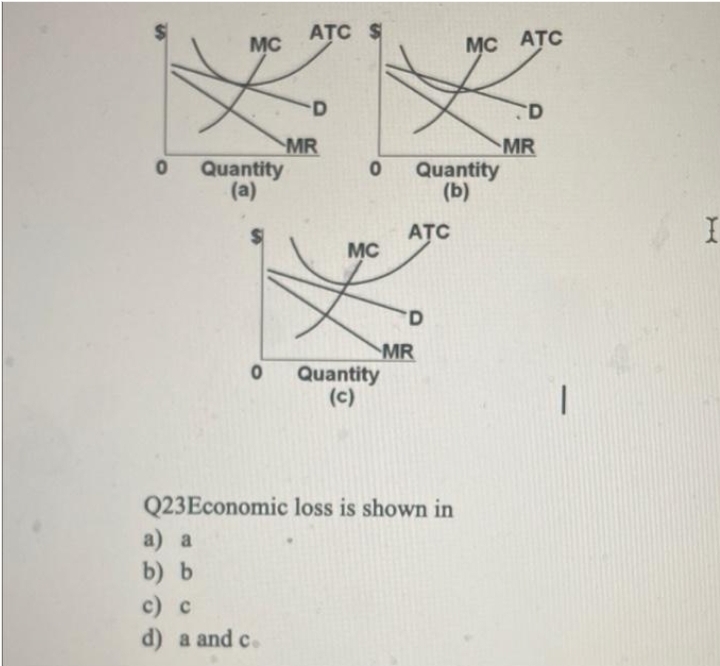

Transcribed Image Text:ATC $

MC

MC ATC

CD

MR

Quantity

(a)

MR

Quantity

(b)

ATC

MC

MR

Quantity

(c)

Q23Economic loss is shown in

а) a

b) b

с) с

d) a and c.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A firms should continue to produce in the short run as long as the price is at least equal to the * MR. MC. minimum ATC. minimum AVC. O AFC.arrow_forwardQUESTION 19 Assume short-run production. Select the statements that are true. O The marginal cost at a particular output level is the slope of a line from the origin to the corresponding point on the cost curve. Changes in fixed costs do not affect the shape or placement of the total cost curve. The average cost curve is everywhere above the average variable cost curve. The difference between the total cost and the total variable cost is a constant. 00000 The marginal cost is the slope of the total cost curve or the total variable cost curve... The "law of diminishing marginal returns" could also be termed the "law of increasing marginal costs" When total cost or total variable cost is increasing, there are increasing marginal returns to the variable input.arrow_forwardFill out chart am confusedarrow_forward

- A decrease in the price of a productive resource will result in each of the following except a(n): A.Downward shift in the average-cost curves for all products which use the resourceB. Increase in the quantities produced and sold of all products which use the resourceC. Rightward shift in the demand curves for all products which use the resourceD. Increase in the quantity demanded of this productive resourcearrow_forward3. (14 points) Let the production function be Q(K,L)=2K L. The cost of one unit of labor is w, the cost of one unit of capital is r, and the quanitity to produce is y. (a) (4 points) Set up the firm's cost-minimization problem, and clearly write down the con- Page 6 straint the firm faces. The cost minimization problem of the firm is min(KL) WL+rK. The constraint: y=2K!L!. anscribed Text (b) (5 points) What are two conditions that the optimal bundle L and K need to satisfy? Write down their expressions. Tangency: -=-; production: y = 2(K)! (L)!. (c) (5 points) Solve for the optimal bundle of L. and K that minimizes the firm's cost at y=144 by finding L and K", assuming that w $16 and r $81. By solving the system of two conditions in Part (b), it should be not that hard to get L = 162 and K* = 32.arrow_forwardI don’t think I’m understanding the question. Could I have an explanation of the mode to solve it?arrow_forward

- Cost (dollars) 150 100 50 0 5 10 D $15 20 B Output (teapots per day) 5. Refer to Figure above. Which one of the following statements are [TRUE/FALSE]? 0 A. The vertical gap between curves B and C is equal to average variable cost. [TRUE/FALSE] 0 B. Average fixed cost decreases with output. [TRUE/FALSE] 0 C. Line B comes closer to line C as output increases because of a decrease in average fixed cost. [TRUE/FALSE] D. The vertical gap between curves B and C is equal to average fixed cost. [TRUE/FALSE] 0 E. Curve D is the marginal cost curve. [TRUE/FALSE]arrow_forwardLump-Sum Tax The city government is considering two tax proposals: • A lump-sum tax of $300 on each producer of hamburgers. • A tax of $1 per burger, paid by producers of hamburgers. please helparrow_forwardQuestion 8 Which of the following is not a variable cost at the sandwich shop? O Cost of labor Cost of tomatoes O Cost of delivery Cost of rent Question 9arrow_forward

- . Rise in costs is a bad thing If rising costs are due to rising prices If rising costs are due to rising demand It is bad anyway Nonearrow_forward$1200 $1000 $1000 D3 $600 D3 D1 D2 \D1 D2 0 300 500 650 500 Computers Per Week Computers Per Week A Refer to the graphs. Suppose a firm is currently producing 500 computers per week and charging a price of $1,000. What happens to the firm's inventory of computers if there is a negative demand shock and prices are inflexible? Multiple Choice The firm's inventory will increase by 200 computers per week. The firm's inventory will not change. The firm's inventory will decrease by 150 computers per week. The firm's inventory will increase by 350 computers per week. rch 99+ Price Pricearrow_forward13. Firms in Competitive Markets The market for fertilizer is perfectly competitive. Firms in the market are producing output but are currently making economic losses. Which of the following statements is true about the price of fertilizer? Check all that apply. The price of fertilizer must be less than average total cost. Price and Costs The price of fertilizer must be less than marginal cost. The price of fertilizer must be equal to average variable cost. The following graphs show the cost curves faced by a typical firm, the demand for fertilizer, and possible price and supply curves. MC Firm ATC LAVC II II Quantity (? P P₂ Demand 1 Market Quantity S₁ S₂ (?)arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education