ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

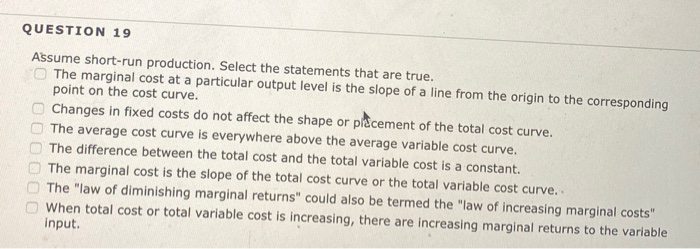

Transcribed Image Text:QUESTION 19

Assume short-run production. Select the statements that are true.

O The marginal cost at a particular output level is the slope of a line from the origin to the corresponding

point on the cost curve.

Changes in fixed costs do not affect the shape or placement of the total cost curve.

The average cost curve is everywhere above the average variable cost curve.

The difference between the total cost and the total variable cost is a constant.

00000

The marginal cost is the slope of the total cost curve or the total variable cost curve...

The "law of diminishing marginal returns" could also be termed the "law of increasing marginal costs"

When total cost or total variable cost is increasing, there are increasing marginal returns to the variable

input.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Moris just opened a chocolate place, it costs her $500 per day to pay for workers’ wages and an additional $2 for each chocolate they make. a. What are the total cost and average cost functions for Moris chocolates b. If Moris chocolate place is open 6 days a week and sells chocolates for $5 each, how many chocoolates does Moris place need to sell each week to break even on its accounting cost?arrow_forward4. Suppose a short-run total cost function is given by C= 600 + 40Q^0.3 + 5 Q^2: (a) Find out the fixxed cost, variable cost, marginal cost, average variable cost and average total cost.arrow_forwardTyped plzzz and Asap Thanksarrow_forward

- Using the numbers representing short run costs in the chart below, calculate the number that belongs in the blank space. q = quantity, TFC = Total Fixed Cost, TVC = Total Variable Cost, AVC = %3D %3D Average Variable Cost Recall that an "X" in the chart means that no number goes in that space. TFC TVC AVC 300 300 150 75 300 270 135 3. 300 370 123.33 4 300 480 300 650 130 300 840 140 1. 2. 6arrow_forwardGiven the cost information below, answer the following questions. Output Total Cost 0 $ 40.00 10 118.40 20 163.20 30 188.80 40 209.60 50 240.00 Instructions: Enter your answers rounded to two decimal places. a. When output is 10, total variable cost is $ . b. When output is 20, average fixed cost is $ . c. When output is 30, average variable cost is $ . d. When output is 40, average total cost is $ . e. When output is 50, marginal cost is $ .arrow_forward4. The shape of a firm's long-run average cost curve depends o how costs vary with scale of operation. Draw a long-run average cost curve for a firm that exhibits economies of scale, constant returns to scale, and diseconomies of scale. Identify each of these sections of the cost curve and explain why each section exemplifies its specific type of return to scale.arrow_forward

- 9:15 AM O Y O 65 Micro15 - Saved d. Righiward A_ 15. When returns to scale are decreasing, total output a. Increases b. Deсreases c. Does not change d. Varies IV. Match The term (column B) that best fits the phrases (Column A below. Column A Column B a. Marginal product A_1. Describe the functional relationship of input and output v_2. Production function b. Least-cost combination _C_3, Infinitesimal change c. Isocost line 4. Output yielded from the last unit of input d. isquant 5. TP divided by the number of variable inputs e. Production function 6. Refers to the declining trend to MP f. Counterproductive conditions 7. Illustrates the varied combinations of inputs at the same level of plant capacity g Finite change 8. Contains combinations of inputs that the same budget can purchase given constant prices h. Marginal rate of substitution 9. Price of labor inputs over price of capital inputs i. Economies of scale 10. Ration between output and input j. Diseconomies of scale k. Maximum…arrow_forwardCalculate the value of total cost when average cost is $35 and the no of inputs employed is 5arrow_forwardWhen fixed costs are ignored because they are irrelevant to a business's production decision, they are called O explicit costs. O implicit costs. Osunk costs. O opportunity costs.arrow_forward

- Given the cost information below, answer the following questions. Output Total Cost $10.00 10 88.40 20 133.20 30 158.80 40 179.60 50 210.00 Instructions: Enter your answers rounded to two decimal places. a. When output is 10, total variable cost is $ b. When output is 20, average fixed cost is $ c. When output is 30, average variable cost is $ d. When output is 40, average total cost is $ e. When output is 50, marginal cost is $arrow_forwardCalculate total costs at 4 units of output. Do not put a dollar sign in your answer. (The 6 columns are Quantity, Total Fixed Cost, Total Variable Cost, Total Cost, Average Total Cost, and Marginal Cost. The Quantity and Total Variable Cost columns have been filled in along with the first row for Total Fixed Cost. Average Total Costs and Marginal Costs are not calculated at a quantity of 0.) Quantity Total Fixed Cost Total Variable Cost Total Cost Average Total Cost Marginal Cost 0 15 0 XXXXX XXXXX 1 25 2 40 3 50 4 55 5 65 Calculate average total costs at 2 units of output. Calculate average total cost at 5 units of output. Calculate marginal cost at 4 units of output (moving from 3 units to 4 units). Can you tell if this is the short run or long run? Can you tell at which level of output profits will be maximized?arrow_forwardQuantity 1 2 3 4 5 6 7 Firm 4 Firm 3 Long-Run Total Cost (Dollars) Firm 1 Firm 1 180 350 510 660 800 930 1,050 Firm 2 120 250 390 540 700 870 1,050 Refer to Table above. Which firm has economies of scale and then diseconomies of scale over the entire range of output? Firm 2 Firm 3 150 300 450 600 750 900 1,050 Firm 4 210 340 490 660 850 1,060 1,290arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education