ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

At a market

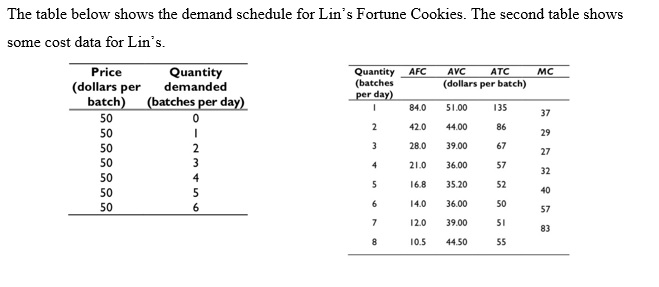

Transcribed Image Text:The text describes two tables related to Lin’s Fortune Cookies. The first table is a demand schedule indicating the relationship between price and quantity demanded. The second table provides cost data.

**Demand Schedule for Lin’s Fortune Cookies:**

- **Price (dollars per batch):** Constant at 50 for all entries.

- **Quantity Demanded (batches per day):** Increases from 0 to 6 as follows:

- 0 batches when the price is $50

- 1 batch

- 2 batches

- 3 batches

- 4 batches

- 5 batches

- 6 batches

**Cost Data for Lin’s:**

- **Quantity (batches per day):** Ranges from 1 to 8.

- **AFC (Average Fixed Cost) dollars per batch:**

- Starts at 84 for 1 batch and declines to 10.5 by 8 batches.

- **AVC (Average Variable Cost) dollars per batch:**

- Starts at 51, decreases initially and then stabilizes around 36 to 39.

- **ATC (Average Total Cost) dollars per batch:**

- Starts at 135, decreases to a low of 52, then exhibits a slight increase to 55.

- **MC (Marginal Cost) dollars per batch:**

- Starts at 37, varying non-linearly, with values such as 29, 22, 32, and rising to 55 by the 8th batch.

These tables help illustrate Lin's Fortune Cookies' demand behavior and cost structure in relation to production volumes.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- In perfect competition, why is a firm's marginal revenue curve also the demand curve for the firm's output? Clara sells handbags in a perfectly competitive market. The price of a handbag is $50. Draw Clara's marginal revenue curve. Label it. 100- 90- 80- 70- 60- 50- 40- 30- 20- 10- 0+ 0 Price (dollars per handbag) 6 8 Quantity (handbags per day) >>> Draw only the objects specified in the question. 2 4 10 oarrow_forwardUnder what conditions will a firm shut down temporarily? Explain. Under what conditions will a firm exit a market?arrow_forwardThe following graph plots daily cost curves for a firm operating in the competitive market for rompers. Hint: Once you have positioned the rectangle on the graph, select a point to observe its coordinates. (?) PRICE (Dollars per romper) 50 45 40 3.5 30 20 15 10 10 5 0 + 0 2 MC ATC AVC 4 6 8 12 14 16 QUANTITY (Thousands of rompers per day) 10 18 H 20 Profit or Lossarrow_forward

- You read in a business magazine that farmers are reaping high profits. With the theory of perfect competition in mind, what do you expect to happen over time (in the long run) to each of the following? a. The prices of agricultural products how will this affect the market equilibrium price of the agricultural products? Will it remain the same, increase or decrease?arrow_forwardBen opened his ice cream stand and he aims to maximize profits by making 100 ice cream cones a day. Ben planned to buy two ice cream makers, but his sister happened to have an extra one and she gave it to him for free. Ben's fixed costs decrease and the market price remains constant. The short run profit maximizing level of output a day a) becomes zero b) is still 100 ice cream cones c) is more than 100 ice cream cones d) is less than 100 ice cream conesarrow_forwardIn the long run with free entry and exit, is the price in a market equal tomarginal cost, average total cost, both, or neither? Explain with a diagram.arrow_forward

- Solve all this question..arrow_forwardTomas is the general manager for a local automated car wash. The market he operates is perfectly competitive. Every car wash in the area is charging $7 for a car wash, which is also the marginal cost per wash. What will happen to Tomas’ profits if he changes his price to $8. Why? What about the price of $5? What is his profit-maximizing price?arrow_forwardDoes a compentve firms price equal its marginal cost in a short run, on the long run or both? Explain, Does a competitive firms price equal the minimum of its average total cost in the short run, in the long run, or both ? Explainarrow_forward

- When would a profit-maximizing firm shut down in the short run?arrow_forwardSuppose Melody owns a business giving piano lessons. Assume that the market for piano lessons is perfectly competitive and that the equilibrium price of a piano lesson is $20. Melody's total costs vary depending on the number of piano lessons she offers each day, as shown in the table below. Number of lessons Total cost per day per day ($) 0 30 1 50 2 68 3 78 4 96 5 115 6 138 168 208 7 8 a. When Melody gives 3 lessons per day, what is her average variable cost? b. What is the profit-maximizing number of lessons for Melody to give each day? lessons per day c. What is Melody's daily economic profit at her profit-maximizing number of lessons? Instructions: If you are entering a negative number, be sure to include a negative sign (-). +Aarrow_forward$11.00 MC| $10.00 $9.00 ATC $8.00 $7.00 TRAVCI $6.00 $5.00 $4.00 $3.00 2 3 7 9 10 Quantity of Output (q) Pierre is a photographer in a perfectly competitive market. The graph shown above gives his MC, ATC and AVC curves. Suppose the market price is $10.50. How much profit does Pierre make? 22.5 24 20 O18 S per unitarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education