ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

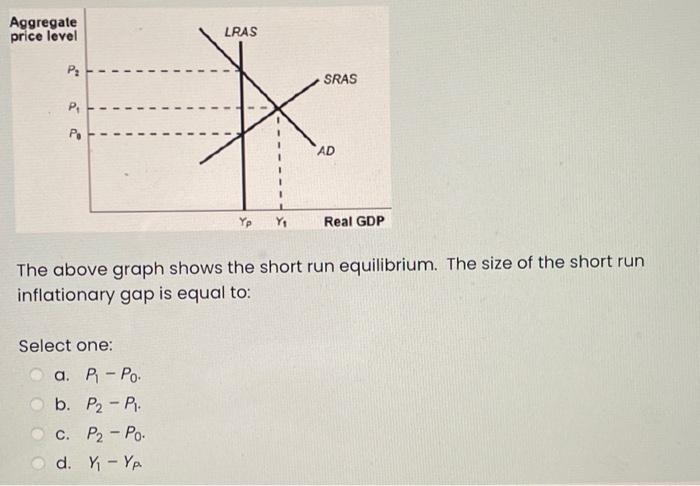

Transcribed Image Text:Aggregate

price level

P₂

P₁

Po

Select one:

LRAS

a. P₁ - Po.

b. P₂ - P.

C. P₂ - Po.

d. Y₁ - Yp

Yp Y₁

SRAS

AD

The above graph shows the short run equilibrium. The size of the short run

inflationary gap is equal to:

Real GDP

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A decrease in the nominal wage will cause the aggregate supply curve to a. become steeper. . b. shift inward. c. shift outward. . d. become flatterarrow_forwardPrice Level 0 A B Real GDP Comparing points A and B on this graph, which of the following is true? O At point B, there would be less employment and higher unemployment than at point A. O At point B, there would be a lower wage than at point A. O At point B, there is a higher price level that increases the quantity of real GDP supplied. O At point A, there is greater pressure on the price level and inflation than at point B. O At point A, with a lower wage rate, aggregate supply has decreased compared to point B.arrow_forwardPlease help solve.arrow_forward

- Answer both please otherwise we will give dounvotearrow_forwardPrice Level AS AD Yu YY Real National Income 4. Referring to the above diagram, which of the following is a true statement? A. Macroeconomic policy will be needed to address rising inflation. B. There is sufficient aggregate demand to cause inflationary pressures. C. The equilibrium in the economy is at a level of output above full employment. D. There is insufficient aggregate demand to reach full employment.arrow_forwardChanges in all of the following shift the LM curve except a. income. b. the money supply. c. the price level. d. money demand.arrow_forward

- GNen the following aggregate demand (aD) and aggregatesupply šchedult.() Price level Real Gpp Deman ded Real GDP Supplied Short-RuN 70 80 90 00 450 400 350 300 కం 40 450 500 250 550 4 the potential RGDP is 45o unets of us¢. Draw and Show the short-run economiC equilibrium and evaluate the situation comparing with the long run aggeegate suppy by ygregate (Lias) explain tHhiis sifuation. explaintis sifutión. 6)if aggregate demand increases by us$ 100. Araw and show the aew equilibrium vacues on tthe Same graph and find the Rew equilibrium po'ssible es lucrease In e bemand. GrRre te One suplancution for thus Aggregatarrow_forwardNeed in Less than 20 minsarrow_forwardReal GDP is $20 trillion, the quantity of money is $10 trillion, and the velocity of circulation is 4. What is the price level? The price level is ___ thank sss !!arrow_forward

- give me answer with details explaintion....arrow_forwardWhen the economy goes into a recession. real GOP---- and unemployment ___ .a. rises, risesb. rises, fallsc falls. risesd. falls, fallsarrow_forward2. Explaining short-run economic fluctuations A majority of economists believe that in the long run, real economic variables and nominal economic variables behave independently of one another. For example, an increase in the money supply, a no long-run effect on the quantity of goods and services the economy can produce, a and nominal variables is known as variable, will cause the price level, a AL AXIS However, in the short run, most economists believe that real and nominal variables are intertwined. Economists use the model of aggregate demand and aggregate supply to examine the economy's short-run fluctuations around the long-run output level. The following graph shows an incomplete short-run aggregate demand (AD) and aggregate supply (AS) diagram-it needs appropriate labels for the axes and curves. In the questions that follow you will identify some of the missing labels. AS variable, to increase but will have variable. The distinction between real variables ?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education