FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Topic Video

Question

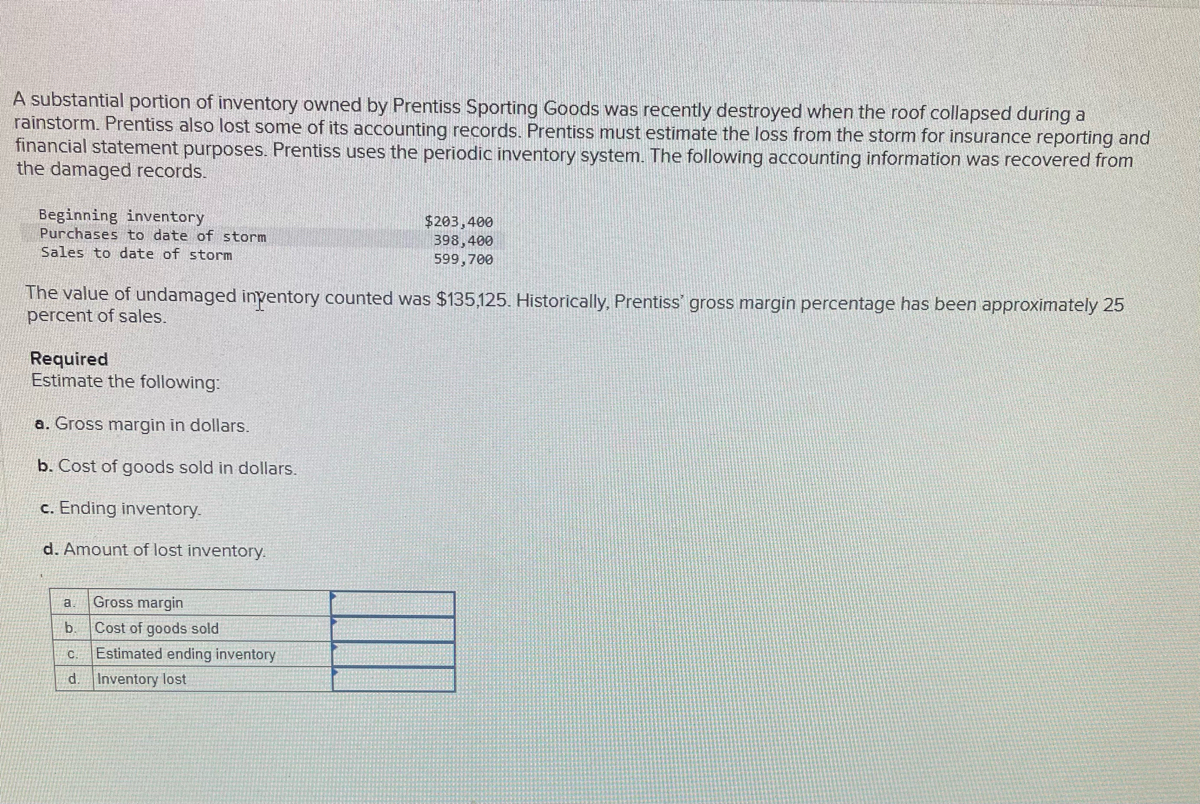

Transcribed Image Text:A substantial portion of inventory owned by Prentiss Sporting Goods was recently destroyed when the roof collapsed during a

rainstorm. Prentiss also lost some of its accounting records. Prentiss must estimate the loss from the storm for insurance reporting and

financial statement purposes. Prentiss uses the periodic inventory system. The following accounting information was recovered from

the damaged records.

Beginning inventory

Purchases to date of storm

$203,400

398,400

599,700

Sales to date of storm

The value of undamaged inyentory counted was $135,125. Historically, Prentiss' gross margin percentage has been approximately 25

percent of sales.

Required

Estimate the following:

a. Gross margin in dollars.

b. Cost of goods sold in dollars.

c. Ending inventory.

d. Amount of lost inventory.

Gross margin

a

b.

Cost of goods sold

C.

Estimated ending inventory

d. Inventory lost

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Cullumber Legler requires an estimate of the cost of goods lost by fire on March 9. Merchandise on hand on January 1 was $ 49,400. Purchases since January 1 were $ 93,600; freight-in, $ 4,420; purchase returns and allowances, $ 3,120. Sales are made at 33 1/3% above cost and totaled $ 156,000 to March 9. Goods costing $ 14,170 were left undamaged by the fire; remaining goods were destroyedarrow_forwardSheridan Legler requires an estimate of the cost of goods lost by fire on March 9. Merchandise on hand on January 1 was $44,080. Purchases since January 1 were $83, 520; freight - in, $3, 944; purchase returns and allowances, $2,784. Sales are made at 33 1/3% above cost and totaled $135,000 to March 9. Goods costing $12, 644 were left undamaged by the fire; remaining goods were destroyedarrow_forwardA substantlal portlon of Inventory owned by Prentiss Sporting Goods was recently destroyed when the roof collapsed during a ralnstorm. Prentiss also lost some of Its accounting records. Prentiss must estimate the loss from the storm for Insurance reporting and financial statement purposes. Prentiss uses the perlodic Inventory system. The following accounting information was recovered from the damaged records. Beginning inventory $196, eee 398, e00 Purchases to date of storm Sales to date of storm бее, вее The value of undamaged Inventory counted was $102,676. Hıstorically, Prentiss' gross margin percentage has been approximately 22 percent of sales. Required Estimate the following: a. Gross margin in dollars. b. Cost of goods sold in dollars. c. Ending Inventory. d. Amount of lost Inventory. a. Gross margin b. Cost of goods sold C. Estimated ending inventory d. Inventory lostarrow_forward

- Riverbed Inc.’s April 30 inventory was destroyed by the explosion of an underground oil tank. January 1 inventory was $322,000 and purchases for January through April totalled $790,000. Sales for the same period were $1.2 million. Riverbed 's normal gross profit percentage is 30%.Using the gross profit method, estimate the amount of Riverbed 's April 30 inventory that was destroyed. Estimated ending inventory destroyed in explosion $enter a dollar amount of the ending inventoryarrow_forwardIn 2022, Sargent Company experienced a major casualty loss. The roof of its warehouse collapsed in an ice storm and destroyed its entire inventory. The company began the year with inventory of $300. It made purchases of $5,640 but returned $80 worth of merchandise. Sales prior to the ice storm were $9,400. Sargent must use the gross profit method to determine inventory on hand on the date of the casualty. The following is an excerpt of its income statement for the last three years. 2019 2020 2021 Net Sales $5,000 $6,000 $9,000 Cost of Goods Sold 2,150 2,340 3,312 General and Administrative Expense 500 600 900 Depreciation Expense 125 200 325 Operating Income $2,225 $2,860 $4,463 Requirement. Assume that Sargent uses the most recent three years of net sales and cost of goods sold to determine its historical gross profit. What are estimated cost of goods sold, estimated gross profit, and estimated ending…arrow_forwardBrad Essary owned a small company that sold garden equipment. The equipment was expensive, and a perpetual system was maintained for control purposes. Even so, lost, damaged, and stolen merchandise normally amounted to 5 percent of the inventory balance. On June 14, Essary's warehouse was destroyed by fire. Just prior to the fire, the accounting records contained a $154,500 balance in the Inventory account. However, inventory costing $11,100 had been sold and delivered to customers but had not been recorded in the books at the time of the fire. The fire did not affect the showroom, which contained inventory that cost $41,200. Required Estimate the amount of inventory destroyed by fire. Inventory destroyed by firearrow_forward

- On September 1 of the current year, Scots Company experienced a flood that destroyed the company's entire inventory. Because the company had not completed its month end reporting for August, it must estimate the amount of inventory lost using the gross profit method. At the beginning of August, the company reported beginning inventory of $216,400. Inventory purchased during August was $192,910. Net Sales for the month of August were $544,400. Assuming the company's typical gross profit ratio is 40%, estimate the amount of inventory destroyed in the flood.arrow_forwardSandhill Legler requires an estimate of the cost of goods lost by fire on March 9. Merchandise on hand on January 1 was $ 37,240. Purchases since January 1 were $ 70,560; freight-in, $ 3,332; purchase returns and allowances, $ 2,352. Sales are made at 33 1/3% above cost and totaled $ 111,000 to March 9. Goods costing $ 10,682 were left undamaged by the fire; remaining goods were destroyed.arrow_forwardOn January 1, a store had inventory of $48,000. January purchases were $46,000 and January sales were $95,000. On February 1 a fire destroyed most of the inventory. The rate of gross profit was 20% of sales. Merchandise with a selling price of $5,000 remained undamaged after the fire. Compute the amount of the fire loss, assuming the store had no insurance coverage. Label all figures.arrow_forward

- 7. The inventory was destroyed by fire on December 31. The following data were obtained from the accounting records:arrow_forwardDuring the taking of its physical inventory on December 31, 20Y4, Barry's Bike Shop incorrectly counted its inventory as $225,870 instead of the correct amount of $179,251. The effect on the balance sheet and income statement would be a. assets overstated by $46,619; retained earnings understated by $46,619; and net income statement understated by $46,619 b. assets overstated by $46,619; retained earnings understated by $46,619; and no effect on the income statement c. assets, retained earnings, and net income all overstated by $46,619 d. assets and retained earnings overstated by $46,619; and net income understated by $46,619arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education