Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

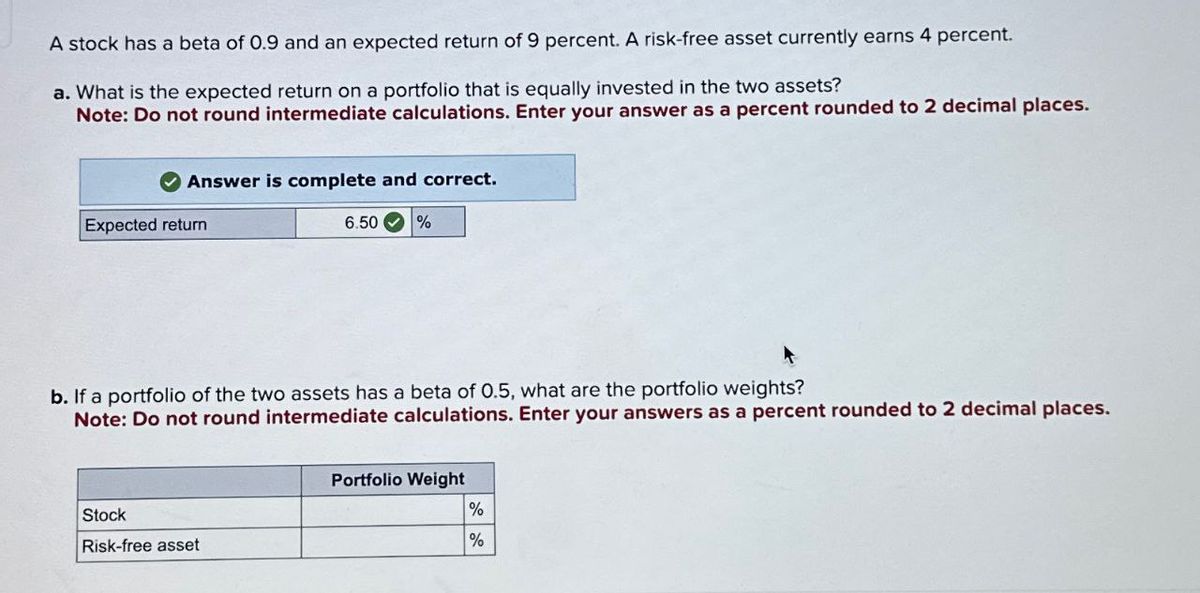

Transcribed Image Text:A stock has a beta of 0.9 and an expected return of 9 percent. A risk-free asset currently earns 4 percent.

a. What is the expected return on a portfolio that is equally invested in the two assets?

Note: Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.

Answer is complete and correct.

Expected return

6.50

%

b. If a portfolio of the two assets has a beta of 0.5, what are the portfolio weights?

Note: Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.

Stock

Risk-free asset

Portfolio Weight

%

%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Similar questions

- A stock has a beta of 1.26 and an expected return of 12.4 percent. A risk-free asset currently earns 4.1 percent. a. What is the expected return on a portfolio that is equally invested in the two assets? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b. If a portfolio of the two assets has a beta of .86, what are the portfolio weights? (Do not round intermediate calculations and round your answers to 4 decimal places, e.g., .1616.) c. If a portfolio of the two assets has an expected return of 11.6 percent, what is its beta? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) d. If a portfolio of the two assets has a beta of 2.46, what are the portfolio weights? (A negative answer should be indicated by a minus sign. Do not round intermediate calculations and round your answers to 4 decimal places, e.g., .1616.)arrow_forwardkindly be as detailed as possible with the calculations. Preferably in excel.arrow_forwardA stock has a beta of 1.39 and an expected return of 13.7 percent. A risk-free asset currently earns 4.75 percent. a. What is the expected return on a portfolio that is equally invested in the two assets? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.) b. If a portfolio of the two assets has a beta of .99, what are the portfolio weights? (Do not round intermediate calculations and round your answers to 4 decimal places, e.g., 1616.) c. If a portfolio of the two assets has an expected return of 12.9 percent, what is its beta? (Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16.) d. If a portfolio of the two assets has a beta of 2.59, what are the portfolio weights? (A negative answer should be indicated by a minus sign. Do not round intermediate calculations and round your answers to 4 decimal places, e.g., 1616.) a. Expected return b. Weight of stock Weight of risk-free…arrow_forward

- A stock has a beta of 1.2 and an expected return of 14 percent. A risk-free asset currently earns 3.8 percent. a. What is the expected return on a portfolio that is equally invested in the two assets? (Do not round intermediate calculations. Enter your answer as a percent rounded to 2 decimal places.) Expected return % b. If a portfolio of the two assets has a beta of 0.20, what are the portfolio weights? (Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places.) Stock Risk-free asset Portfolio Weight % % c. If a portfolio of the two assets has an expected return of 12.50 percent, what is its beta? (Do not round intermediate calculations. Round your answer to 4 decimal places.) Betaarrow_forwardParts A-C have already been answered, looking for answer D.arrow_forwardStart with A-C and I will submit seperately for D! Thank you :)arrow_forward

- please help someone!!arrow_forwardA stock has a beta of 1.22 and an expected return of 12 percent. A risk-free asset currently earns 3.9 percent. a. What is the expected return on a portfolio that is equally invested in the two assets? Note: Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16. b. If a portfolio of the two assets has a beta of .82, what are the portfolio weights? Note: Do not round intermediate calculations and round your answers to 4 decimal places, e.g., .1616. c. If a portfolio of the two assets has an expected return of 11.2 percent, what is its beta? Note: Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16. d. If a portfolio of the two assets has a beta of 2.42, what are the portfolio weights? Note: A negative answer should be indicated by a minus sign. Do not round intermediate calculations and round your answers to 4 decimal places, e.g., .1616. a. Expected return b. Weight of stock Weight of…arrow_forwardAlready have answers for A-C, just need D. Thank you! :)arrow_forward

- If a given stock in the portfolio had established 1.23 beta; the related expected return is at 11.7percent, and 3.5percent is the current earning of a risk-free asset; a. Determine the expected return on a portfolio that is equally invested in the two assets? b. If a portfolio of the two assets has a beta of 0.7, what are the portfolio weights? c. If a portfolio of the two assets has an expected return of 9%, what is its beta? d. If a portfolio of the two assets has a beta of 2.46, what are the portfolio weights? How do you interpret the weights for the two assets in this case? Discuss.arrow_forwardAn Equity has a beta of 0.9 and an expected return of 9%. A risk free asset currently earns 2%. i.) What is the expected return on a portfolio that is equally invested in two assets? ii.) If a portfolio of the two assets has an expected return of 6%, what is its beta? iii.) If a portfolio of the two assets has a beta of 1.5, what is its weight ? Iv.) If a portfolio of the two assets has a beta of 1.5, what are the portfolio weights? How do you interpret the weights for the two assets in this case? Explain.arrow_forwardYou own a portfolio equally invested in a risk-free asset and two stocks. One of the stocks has a beta of 1.16 and the total portfolio is equally as risky as the market. What must the beta be for the other stock in your portfolio? Note: Do not round intermediate calculations and round your answer to 2 decimal places, e.g., 32.16. Betaarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education