Related questions

Concept explainers

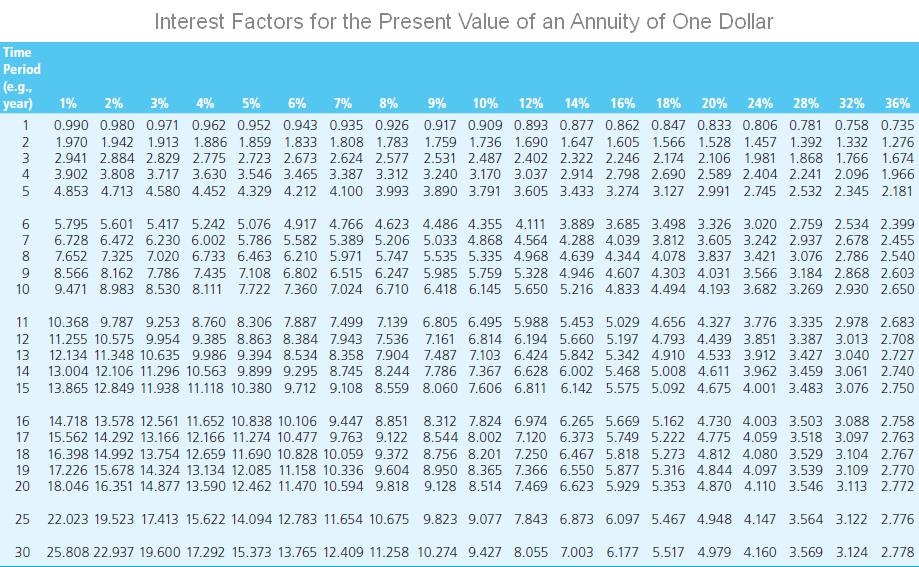

A $1,000 bond has a coupon of 5 percent and matures after twelve years. Assume that the bond pays interest annually.

-

What would be the

bond's price if comparable debt yields 8 percent? Use Appendix B and Appendix D to answer the question. Round your answer to the nearest dollar.$ ____________

-

What would be the price if comparable debt yields 8 percent and the bond matures after six years? Use Appendix B and Appendix D to answer the question. Round your answer to the nearest dollar.

$ _________---

-

What are the current yields and the yields to maturity in a and b? Round your answers to two decimal places.

The bond matures after twelve years:

CY: ______%

YTM: _________ %The bond matures after six years:

CY: _____ %

YTM: _____ %

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps

- Use the following information to answer the questions. Bond A Bond B Face Value 1000 1000 Coupon rate 10% 8% Coupons paid out Semi-annually Quarterly Years to maturity 4 4 Bond price 800 ? Suppose bond A and B have the same YTM. What is the yield to maturity of bond A? What is the price of bond B? What is the current yield of bond B? What is the EAR (effective annual rate) of these two bonds?arrow_forwardSuppose that the prices of zero-coupon bonds with various maturities are given in the following table. The face value of each bond is $1,000. Maturity (Years) 1 2 3 4 5 Required: a. Calculate the forward rate of interest for each year. b. How could you construct a 1-year forward loan beginning in year 3? c. How could you construct a 1-year forward loan beginning in year 4? Required A Price $940.93 Complete this question by entering your answers in the tabs below. 868.39 800.92 735.40 670.48 Required B Maturity (years) 2 3 Calculate the forward rate of interest for each year. Note: Round your answers to 2 decimal places. Required C Forward Rate % % Prov 12 of 12 Nextarrow_forward5) You purchase a 30 year bond with nominal semiannual coupon rate 7% and nominal semiannual yield rate of 6% and face value of $1,000. If you sell the bond immediately after receiving your 20th semiannual coupon payment for a price of $925, then find your actual semiannual nominal yield rate for the 10 year period, and find the buyer's semiannual nominal yield rate for the 20 year period.arrow_forward

- The current zero-coupon yield curve for risk-free bonds is as follows: What is the risk-free interest rate for a five-year maturity? The risk-free interest rate for a five-year maturity is _____%. (Round to two decimal places.)arrow_forwardA 9-year bond has a yield of 13.5% and a duration of 8.63 years. If the MARKET yield changes by 60 basis points, what is the percentage change in the bond’s price? Is this an increase or decrease? A 9-year bond has a yield of 13.5% and a duration of 8.63 years. If the BOND'S yield changes by 60 basis points, what is the percentage change in the bond’s price? Is this an increase or decrease? ( Explain well both question with proper step by step Answer) .arrow_forwardFind the duration of a bond with a settlement date of May 27, 2025, and maturity date November 15, 2036. The coupon rate of the bond is 6.0%, and the bond pays coupons semiannually. The bond is selling at a bond-equivalent yield to maturity of 8.0%. Use Spreadsheet 16.3. Note: Do not round intermediate calculations. Round your answers to 2 decimal places. X Answer is complete but not entirely correct. Macaulay duration Modified duration 11.98 X 11.52 Xarrow_forward

- A $1,000 bond has a 6.5 percent coupon and matures after ten years. If current interest rates are 8 percent, what should be the price of the bond? Assume that the bond pays interest annually. Use Appendix B and Appendix D to answer the question. Round your answer to the nearest dollar. $ If after six years interest rates are still 8 percent, what should be the price of the bond? Use Appendix B and Appendix D to answer the question. Assume that the bond pays interest annually. Round your answer to the nearest dollar. $ Change the interest rate in a and b to 6 percent and rework your answers. Assume that the bond pays interest annually. Round your answers to the nearest dollar. Price of the bond (ten years to maturity): $ Price of the bond (four years to maturity): $arrow_forwardConsider a bond with semiannual interest payments that has a Settlement Date of 8/15/2020, a Maturity Date of 2/15/2031, a Coupon Rate of 5.00%, a Market Price of $975, a Face Value of $1,000, and a Required Return of 5.35%. What is the Macaulay Duration using the Duration function on these bonds expressed as a decimal calculated to two decimal places if you purchase them at the current market price? For example, if your answer is 12.345 then enter as 12.35 in the answerarrow_forwardSuppose that the prices of zero-coupon bonds with various maturities are given in the following table. The face value of each bond is $1,000. Maturity (Years) 1 2 3 4 5 Price $983.78 865.89 797.92 732.00 660.24 Required: a. Calculate the forward rate of interest for each year. b. How could you construct a 1-year forward loan beginning in year 3? c. How could you construct a 1-year forward loan beginning in year 4?arrow_forward

- A General Power bond carries a coupon rate of 9.2%, has 9 years until maturity, and sells at a yield to maturity of 8.2%. (Assume annual interest payments.) a. What interest payments do bondholders receive each year? b. At what price does the bond sell? Note: Do not round intermediate calculations. Round your answer to 2 decimal places. c. What will happen to the bond price if the yield to maturity falls to 7.2%? Note: Do not round intermediate calculations. Round your answer to 2 decimal places. A a. Interest payments b. Price c. Price will byarrow_forwardA bond that matures in 8 years has a par value of $1,000 and an annual coupon payment of $70; its market interest rate is 9%. What is its price? A bond that matures in 12 years has a par value of $1,000 and an annual coupon rate of 10%; the market interest rate is 8%. What is its price? Which of those two bonds is a discount bond, and which is a premium bond? Explain.arrow_forwardGive typing answer with explanation and conclusion A 3-month zero-coupon bond is selling for $99.7 and a 10-year zero-coupon bond is selling for $55.7. Both bonds have a face value of $100. What's the 10-year - 3-month spread in their yields? Answer in percent, rounded to one decimal place.arrow_forward

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education