ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

a, b, and c of this have already been solved (see attached). Attachment also includes original question.

(d) How much is the total surplus of this economy?

(e) Now suppose that the industry makes a one-time investment for $K amount of dollars to innovate in a new technology of production that allows every firm to reduce its cost of production to a 1/4 fraction of the previous cost. What is the new total surplus of the economy? Who is benefiting the most from the industry innovation?

(f) Is it reasonable to assume that in the long-run $K is exactly equal to the size of the industry profits? why?

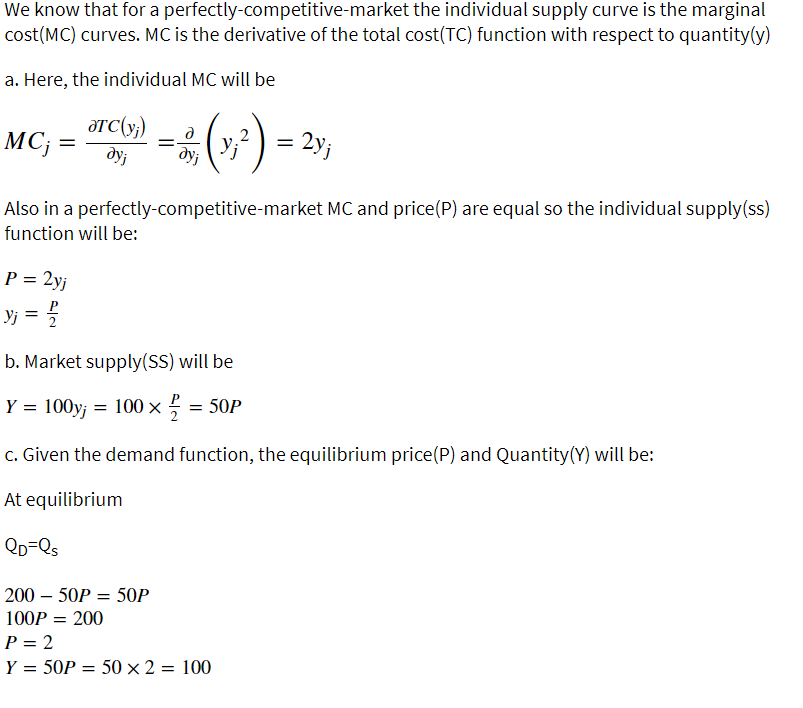

Transcribed Image Text:We know that for a perfectly-competitive-market the individual supply curve is the marginal

cost(MC) curves. MC is the derivative of the total cost(TC) function with respect to quantity(y)

a. Here, the individual MC will be

ÖTC(y;)

MC; =

(;) - 25,

- 2y;

%3D

%3D

dyj

Also in a perfectly-competitive-market MC and price(P) are equal so the individual supply(ss)

function will be:

P = 2yj

Yj

b. Market supply(SS) will be

P

Y = 100y; = 100 × = 50P

c. Given the demand function, the equilibrium price(P) and Quantity(Y) will be:

At equilibrium

QD=Qs

200 – 50P = 50P

100P = 200

%3D

P = 2

Y =

= 50P = 50× 2 = 100

Transcribed Image Text:Tech firms produce goods and services from labor and energy. The total cost in dollars to produce y

amount of goods and services for each firm j is c;(y;) = y? . There are 100 identical tech firms which

all behave competitively.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- a. What is the consumer surplus at a price of $7? b. What is producer surplus at a price of $7? Note:- Please avoid using ChatGPT and refrain from providing handwritten solutions; otherwise, I will definitely give a downvote. Also, be mindful of plagiarism. Answer completely and accurate answer. Rest assured, you will receive an upvote if the answer is accurate.arrow_forwardPRICE (Dollars per un QUANTITY (Units) Private Cost Demand Which of the following options could be represented by this graph? Oa. A local flower shop adorning the front porch with lots of flowers, which anyone passing by can appreciate. Ob. You next door neighbor burning wet wood in their backyard, resulting in smoke entering your house. Oc. Half of the people in a town getting their flu shots, thus reducing the chances of spreading the disease even to those without the shot. Od. Companies innovating and creating new technologies that end up benefitting the public.arrow_forwardQ4: Consider the market (supply and demand) for Wheat.Qd = 100 - 0.6P…………1Qs = -30 + 2P……...…...2a. Find the market equilibrium price and quantity?b. Find the market equilibrium price and quantity After imposing an ad valorem tax on production by 5% of good price.c. Find the market equilibrium price and quantity if producers receive a production subsidy of 10 SR per unit produced.arrow_forward

- 15arrow_forwardBetty is willing to pay up to $150 for a particular pair of boots. She is able to buy the boots for $120. The marginal cost of producing the boots is $60. How large is the total economic surplus associated with her purchase of the boots?arrow_forward2. In the following, we are going to use the microeconomic theory we have developed in class to explore the short run implications of the rise in the price of gasoline in 2022 due to various factors, including the war in Ukraine. We can use the "constant elasticity" demand function, Qg = Pey, as a framework for representing the demand for gasoline. The reason it is named as such is that the exponents for the price of gasoline (P) and income (Y), denote the price elasticity of demand (e) and income elasticity of demand () for all levels of each variable. a. Use the formula for price elasticity of demand to calculate the price elasticity of demand to show that it equals the parameter &. Note that you would receive an analogous result if you did this for income elasticity of demand. b. Use the following estimated values to "calibrate" the constant elasticity demand function, that is, use algebra to solve for a value for the parameter (phi) based on average annual consumption, average…arrow_forward

- D, E and F please thank youarrow_forward1) In the market for second hand cars, when the phenomenon of 'adverse selection'occurs this normally refers to the fact that(a) second hand cars are by definition worse than new cars.(b) only relatively poor people want to buy second hand cars.(c) sellers of relatively good cars withdraw from the market .(d) None of the above.2) Producer surplus will be zero at any quantity if(a) supply is perfectly inelastic.(b) supply is perfectly elastic .(c) demand is perfectly inelastic.(d) demand is perfectly elastic.arrow_forwardPrice P₂ b C d e 1) 2) P₁ D Q₁ Q₂ Quantity 3) If actual production and consumption occur at Q1 and the price is P2 a) deadweight loss equals area f. b) consumer surplus equals area a + b. c) producer surplus equals area c. d) producer surplus equals area c + b. If actual production and consumption occur at Q2 a) there is deadweight loss of f. b) economic surplus is below the maximum. c) consumer surplus and producer surplus is maximized. d) there is deadweight loss of d. If actual production and consumption occur at Q1 and the price is P1 deadweight loss equals area b. a) b) consumer surplus equals area a. c) consumer surplus equals area a + b. d) producer surplus equals area c + b. R? deadweight loss equals areaarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education