ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

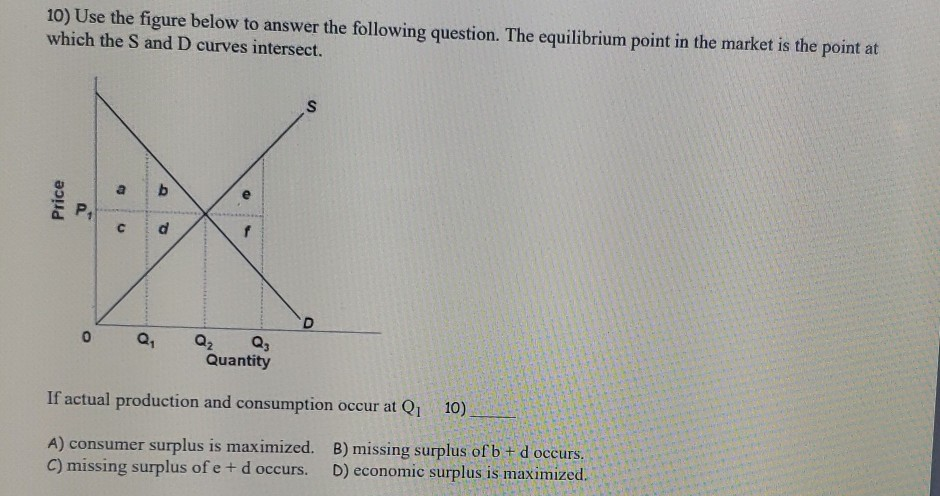

Transcribed Image Text:10) Use the figure below to answer the following question. The equilibrium point in the market is the point at

which the S and D curves intersect.

Price

P₁

0

a

C

Q₁

b

d

Q₂

@

Quantity

S

D

If actual production and consumption occur at Q₁

A) consumer surplus is maximized.

C) missing surplus of e + d occurs.

10)

B) missing surplus of b + d occurs.

D) economic surplus is maximized.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- II. What will happen to Demand(D), Supply(S), new Equilibrium Price(P*), and new Equilibrium Quantity(Q*) when the market condition changes as the following. Explain the reason and draw relevant graphs supporting your analysis. A. Market: Plywood in Florida Event: The Hurricane Center increases the probability of Hurricane to make a landfall in Florida B. Market: Bauxite Event: GM is able to increase the mph of its vehicles by using more aluminum in cars and so plans to use more aluminum. Bauxite is a resource in producing aluminum. C. Market: Skateboards Event: The price of fiberglass rises (Fiberglass is a substance used for making skateboards) D. Market: Hamburger Event: 1. A new processing technology lowers the production cost of hamburger patties AND, simultaneously, Event: 2. The Surgeon General advocates eating only 2 ounces of red meat per day for health concerns E. Market: Chicken Event 1. Avian flu spreads fast hurting chicken producers AND, simultaneously, Event 2.…arrow_forwardD(x) is the price, in dollars per unit, that consumers are willing to pay for x units of an item, and S(x) is the price, in dollars per unit, that producers are willing to accept for x units. Find (a) the equilibrium point, (b) the consumer surplus at the equilibrium point, and (c) the producer surplus at the equilibrium point. D(x)=(x−9)^2, S(x)=x^2+6x+57arrow_forwardConsumer surplus is a measure of the difference between: a) The price which a consumer has to pay and the cost of producing the good (in a diagram, the area between the market price, and the supply curve). b) The consumer’s willingness to pay, and the cost of production (the area between the demand curve and the supply curve). c) The value which a consumer places on a unit of the good, and the market price (the area between the demand curve and the market price line). d) The marginal revenue from sales and the marginal cost of sales (the area between the marginal revenue and the marginal cost curves).arrow_forward

- Neha buys an iPhone for $240 and gets a consumer surplus of $160. Her willingness to pay for an iPhone is . If she had bought the iPhone on sale for $180, her consumer surplus would have been . If the price of the iPhone had been $500, her consumer surplus would have beenarrow_forwardIII. Market Equilibrium 1. Complete the sentence: The market is in equilibrium when The demand function is Q = 5000 – 10p, and the supply function is Q = 200 + 6p. 2. Determine the equilibrium price and quantity.arrow_forwardAssume that you are told that because of some changes, the equilibrium price increased but it is unknown if the equilibrium quantity increased, remained the same, or decreased. Which of the following would be consistent with this outcome?a. There was a decrease in input costs and consumers expected lower income.b. Consumers expected a lower price and firms expected a higher price.c. There was a decrease in income (the good is inferior) and a decrease in the number of firms.d. There was a positive change in consumer tastes and an increase in productivity. When demand is _______ consumers are _______ to price changes and the price elasticity of demand is _______.a. elastic, relatively sensitive, greater than one (in absolute value)b. inelastic, completely insensitive, equal to one (in absolute value)c. inelastic, relatively sensitive, less than one (in absolute value)d. unit elastic, hyper-sensitive, equal to zeroe. perfectly elastic, hyper-sensitive, equal to one (in absolute value)…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education