ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

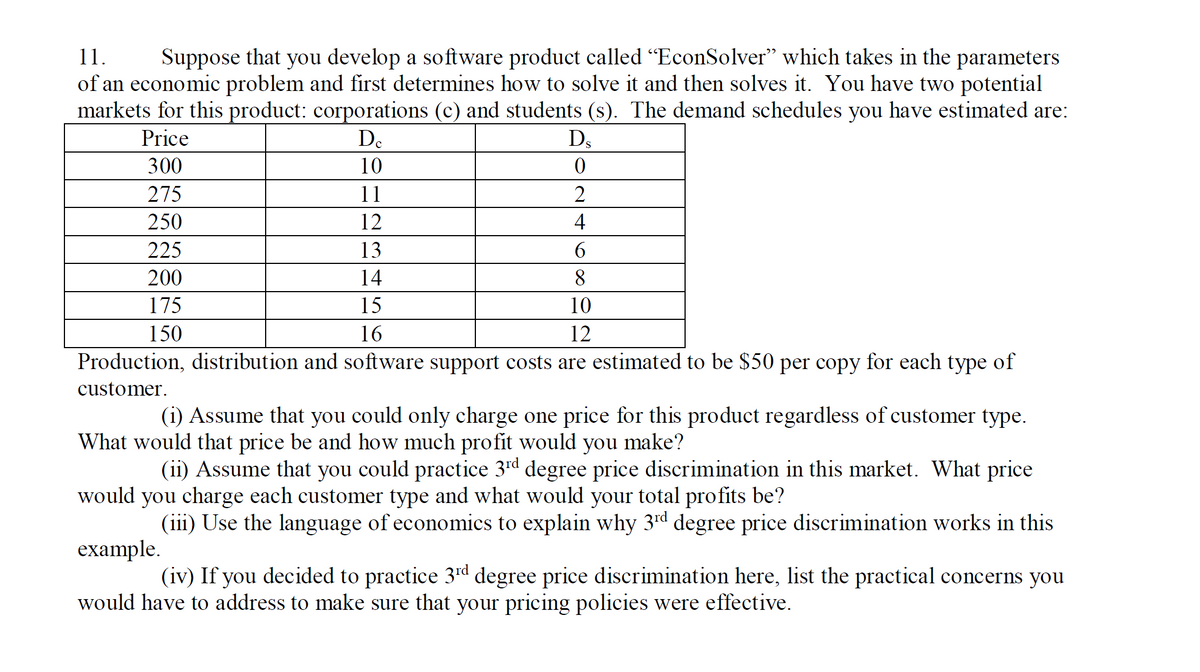

Transcribed Image Text:11.

Suppose that you develop a software product called "EconSolver" which takes in the parameters

of an economic problem and first determines how to solve it and then solves it. You have two potential

markets for this product: corporations (c) and students (s). The demand schedules you have estimated are:

Price

Dc

10

11

12

13

14

15

16

DS

0

2

4

6

8

10

12

Production, distribution and software support costs are estimated to be $50 per copy for each type of

customer.

300

275

250

225

200

175

150

(i) Assume that you could only charge one price for this product regardless of customer type.

What would that price be and how much profit would you make?

(ii) Assume that you could practice 3rd degree price discrimination in this market. What price

would you charge each customer type and what would your total profits be?

(iii) Use the language of economics to explain why 3rd degree price discrimination works in this

example.

(iv) If you decided to practice 3rd degree price discrimination here, list the practical concerns you

would have to address to make sure that your pricing policies were effective.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps

Follow-up Questions

Read through expert solutions to related follow-up questions below.

Follow-up Question

Please answer part (iv) of the above question

Solution

by Bartleby Expert

Follow-up Questions

Read through expert solutions to related follow-up questions below.

Follow-up Question

Please answer part (iv) of the above question

Solution

by Bartleby Expert

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Quiz: Demand i 5 2 Question 18- Module 3 Quiz: Demand - Connect W An increase in the demand for music downloads indicates that more music downloads are Multiple Choice #3 demanded because music download prices have decreased. demanded because sellers are putting music downloads on sale. demanded because sellers are selling more music downloads. demanded even if prices of music downloads stay the same. Q E $ 4 R % 5 T Saved U * 8 + ( ( 9 0 0arrow_forwardhelp please answer in text form with proper workings and explanation for each and every part and steps with concept and introduction no AI no copy paste remember answer must be in proper format with all workingarrow_forward12- 11- Price of Santa hats (5) 9. 2 1 2000 4000 6000 8000 Quantity of Santa hat Supply Demand 10000 Suppose a 3 dollar tax is imposed on the market for Santa hats depicted above. Consumers will then pay a post-tax price of dollars (give a whole number).arrow_forward

- 9. Let (inverse) demand be Pb = 84 - 1 Qb and (inverse) supply be Pv = 20 + 2 Qv. What quantity will buyers purchase if the market is competitive? Answer: your answer Submit Price ($) $200 $ 180 $ 160 $140 $120 $100 $80 $ 60 $40 $20 $0 0 10 20 Demand 30 40 Supply 50 Eqm 60 70 80 90arrow_forward1. Exercise 14.1 The price elasticity of demand for a textbook sold in the United States is estimated to be -2, whereas the price elasticity of demand for books sold overseas is -3. The U.S. market requires hardcover books with a marginal cost of $40; the overseas market is normally served with softcover texts on newsprint, having a marginal cost of only $15. The profit-maximizing price in the U.S. market is that MR P× (1+ × (1+)) and the profit-maximizing price in the overseas market is (Hint: Rememberarrow_forwardA1). The price, p, that a bookstore charges for a special gift edition of a popular trilogy is related to the demand, q, by the equation 100pq + q? = 5,000,000. Suppose the price is currently set at $40. (a). At what rate is the demand currently changing with respect to this price? (Include units) (b). At what rate is the revenue currently changing with respect to this price? (Hint: use the chain rule). (Include units). (c). Suppose the demand is currently increasing at a rate of 50 copies per month. How fast is the price currently changing per month? (again, assume the price is currently $40).Include units.arrow_forward

- Q4) Assume a market of a specific good. The demand and supply equation is as shown below: Pp = 70 – 3QD Ps = 5 + 20s The demand price elasticities is inelastic. From the firms' perspective, the revenue would be higher if price increases. Let's assume that the market is currently not at the equilibrium with the market price being higher by 2 units than the equilibrium price. 1. Find the market quantity 2. Find the new Consumer Surplus 3. Find the new Producer Surplusarrow_forwardQuestion 2: Suppose you have the following information about the demand and supply of cotton in the U.S.: Price 9 15 25 35 U.S. Supply 4 12 17 U.S. Demand 40 36 30 20 10 (a) Determine the equations of the supply and demand curves. Assume that the two equations are linear. (b) Determine the market equilibrium price and quantity. (c) Now suppose that the US can import an arbitrary quantity of cotton at a price of 15 Dollars. How many units will the U.S. import?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education