ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

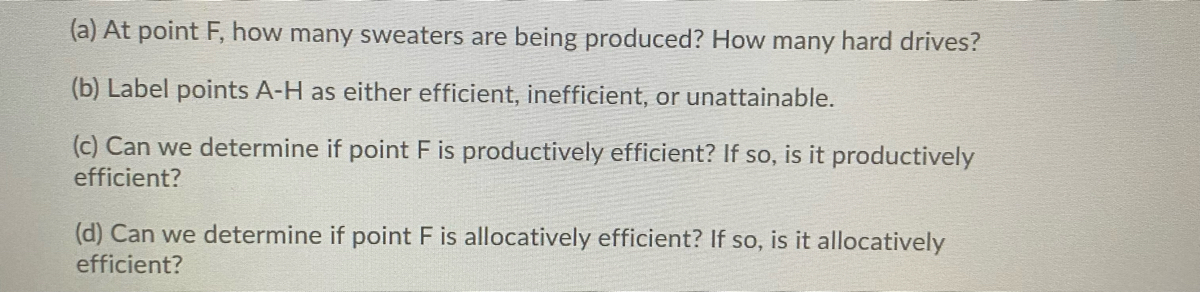

Transcribed Image Text:(a) At point F, how many sweaters are being produced? How many hard drives?

(b) Label points A-H as either efficient, inefficient, or unattainable.

(c) Can we determine if point F is productively efficient? If so, is it productively

efficient?

(d) Can we determine if point F is allocatively efficient? If so, is it allocatively

efficient?

Transcribed Image Text:Use the PPF to answer the following questions:

D.

Hard drives

A

525

E.

450

400

350

300

250

200

150

100

50

5 10 15 20 25 30 35 40 45 50

Sweaters

(thousands)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps

Knowledge Booster

Similar questions

- Constrained Optimization A firm wants to minimize the cost of producing 100 units of output given that the cost of labor (w) is $10 and the cost of capital (r) is $5. Output is produced according to the Cobb-Douglas production function: Q = 10L5K.5. What is the mix of inputs that minimizes the cost of producing 100 units?arrow_forwardA household is considering installing solar panels, but they need to understand what they are paying for electricity. They use an average of 15 kilowatt hours of electricity per day, and an average month is 30 days. They pay $0.22 per kilowatt hour for the first 350 kilowatt hours used in a month, and $0.19 per kilowatt hour after that (a) What is their average cost of electricity?(b)What is their marginal cost of electricity?arrow_forwardQuestion What is the production efficient q? C(q)= 100q-4q^2+0.2q^3+450arrow_forward

- Ike's Bikes is a major manufacturer of bicycles. Currently, the company produces bikes using only one factory. However, it is considering expanding production to two or even three factories. The following table shows the company's short-run average total cost (SRATC) each month for various levels of production if it uses one, two, or three factories. (Note: Q equals the total quantity of bikes produced by all factories.) NOTE: the options for the blank question is this Suppose Ike's Bikes is expecting to produce 500 bikes per month for several years. In this case, in the long run, it would choose to produce bikes using _______ (once factory OR two factory OR three factory)arrow_forward.(a) A firm has production function q(k,l) = k'/³1²/3, where k denotes the capital used and I denotes the labour employed. Suppose that each unit of capital costs v dollars and each unit of labour costs w dollars, so that the capital and labour costs are vk + wl. Use the Lagrange multiplier method to determine the values of k and I that minimise the cost of producing Q units of the firm's good. Find the corresponding minimised value, C, of this cost and the value, X*, of the Lagrange multiplier corresponding to the optimising values of k and l. Show that d* =arrow_forwardPlease explain steps to formulate the equation in (i)arrow_forward

- (a) Derive the first order condition showing how much labor and capital a producer should use to minimize the total costs of producing a given level of output. (b) What is the second order condition for the producer to achieve (a). (c) Draw a figure showing your answer to part (a) and another figure showing the opposite (i.e., a producer maximizing output with given total costs). How does either situation compare with a producer who has neither a total output constraint or a total cost constraint?arrow_forwardQUESTION 3 Zeus owns a factory which makes guitars which sell for $400 each. The number of guitars he can make in a month depends on the size of his crew. He pays each person on his crew $1500/month. He also pays rent on a building, which he has leased for the remainder of the year for $2000/month. The table below indicates how many guitars can be built, as a function of the size of his crew (the crew size excludes himself). You may assume all other cost, such as materials, are 0. Size of Crew Total # of Guitars 1 4 2 8 3 19 4 28 5 40 6 50 7 58 8 earns without a dollar sign and without a comma). 64 The size of the crew that maximizes the firm's profits is 9 67 10 70 11 72 12 The Marginal product of labor is the additional output per worker. Crew member delivers the greatest marginal product. 74 13 and Zeus dollars in profit per month (please record your answer 75arrow_forwardEconomics Questionarrow_forward

- For a certain company, the cost for producing x items is 60x + 300 and the revenue for selling x items is 100x – 0.5x². - The profit that the company makes is how much it takes in (revenue) minus how much it spends (cost). In economic models, one typically assumes that a company wants to maximize its profit, or at least wants to make a profit! Part a: Set up an expression for the profit from producing and selling x items. We assume that the company sells all of the items that it produces. (Hint: it is a quadratio polynomial.) Part b: Find two values of x that will create a profit of $300. The field below accepts a list of numbers or formulas separated by semicolons (e.g. 2; 4; 6 or x + 1; x – 1). The order of the list does not matter. To enter va, type sqrt(a). x = Part c: Is it possible for the company to make a profit of $15,000?arrow_forwardWhat does it mean when the initial allocation is interim Pareto Efficientarrow_forwardSuppose you have t = 5 hours in total to spend on some projects to make some money. The table below shows how many dollars you can make (Total Revenue) in each of the three projects I, II, III if you spend the corresponding number of hours on that project: How would you allocate your time across the projects?What is the maximum total money you could make?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education