ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

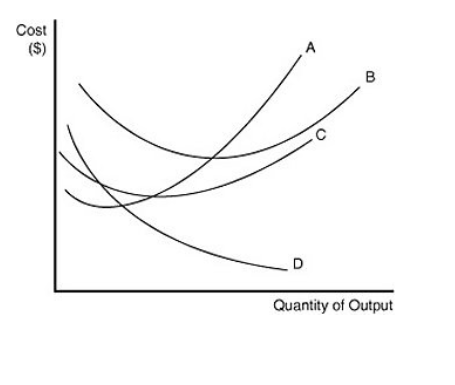

In the figure above, which of the following statements makes sense?

Group of answer choices

A) Average fixed cost is B, marginal cost is D,

B) Average fixed cost is C, marginal cost is B, average total cost is D and average variable cost is A.

C) Average fixed cost is A, marginal cost is B, average total cost is C and average variable cost is D.

D)Average fixed cost is D, marginal cost is A, average total cost is B and average variable cost is C

Transcribed Image Text:Cost

($)

D

B

Quantity of Output

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider an airline's decision about whether to cancel a particular flight that hasn't sold out. The following table provides data on the total cost of operating a 100-seat plane for various numbers of passengers. Total Cost Number of Passengers (Dollars per flight) 40,000 10 60,000 20 65,000 30 68,000 40 70,000 50 71,000 60 72,500 70 73,500 80 74,000 90 74,300 100 74,500 Given the information presented in the previous table, the fixed cost to operate this flight is s At each ticket price, a different number of consumers will be willing to purchase tickets for this flight. Assume that the price of a flight is fixed for the duration of ticket sales. Use the previous table as well as the following demand schedule to complete the questions that follow. Price Quantity Demanded (Dollars per ticket) (Tickets per flight) 1,000 700 30 400 90 200 100arrow_forwardLabel each of the following as sunk cost, opportunity cost, or incremental costs and briefly explain why: (Chapter 2) You are deciding which car to buy. Car A is $24,000 and car B is $32,000. The difference in price is $8,000. What kind of cost does this represent? Answer: Your company invested $300,000 into a study to determine the feasibility of introducing a new product line into the business. The study recommended 2 mutually exclusive feasible alternatives. What kind of cost does the $300K represent? Answer: You have 2 alternatives for a $10,000 investment. Investment A provides a $500 return and investment B provides a $700 return. If you choose Alternative B, what does the $500 return from Alternative A represent? Answer:arrow_forwardWhich of the following is correct? a) Total Fixed Cost = Total Cost + Total Variable Cost b) Total Cost = Total Variable Cost + Marginal Cost c) Average Fixed Cost = Average Total Cost – Average Variable Cost d) Average Total Cost = Marginal Cost + Average Fixed Costarrow_forward

- Question 6: For each of the total cost functions, write the expressions for the average cost, average fixed cost, average variable cost, and marginal cost: 1. TC (Q) = 5Q 2. TC (Q) = 120 +6Q 3. TC (Q) = 6Q² 4. TC (Q) = 140 +5Q²arrow_forwardCalculate total costs at 4 units of output. Do not put a dollar sign in your answer. (The 6 columns are Quantity, Total Fixed Cost, Total Variable Cost, Total Cost, Average Total Cost, and Marginal Cost. The Quantity and Total Variable Cost columns have been filled in along with the first row for Total Fixed Cost. Average Total Costs and Marginal Costs are not calculated at a quantity of 0.) Quantity Total Fixed Cost Total Variable Cost Total Cost Average Total Cost Marginal Cost 0 15 0 XXXXX XXXXX 1 25 2 40 3 50 4 55 5 65 Calculate average total costs at 2 units of output. Calculate average total cost at 5 units of output. Calculate marginal cost at 4 units of output (moving from 3 units to 4 units). Can you tell if this is the short run or long run? Can you tell at which level of output profits will be maximized?arrow_forwardIn Figure 2-a, the average variable cost curve is curve Group of answer choices A D C Barrow_forward

- Which of the following is always true?A) When marginal costs are less than average total costs, average total costs will be increasing.B) When average fixed costs are falling, marginal costs must be less than average fixed costs.C) When average fixed costs are rising, marginal costs must be greater than average total costs.D) When marginal costs are greater than average total costs, average total costs will be increasing.arrow_forwardThe Santa Clara County increases the property taxes for all fast food restaurants. Which cost curves will be affected as a result of this policy? 1. average total cost and average fixed cost. 2. average variable cost and average total cost. 3. average variable cost and marginal cost. 4. average variable cost and average fixed cost.arrow_forwardThe ratio of total cost to number of units produced defines: a. Incremental cost b. Average cost c. Marginal cost d. Opportunity cost.arrow_forward

- Businesses wanted to reduce their cost to the minimum without compromising the product quality and violating laws. The total fixed cost decreases if the output increases. Thus the business is left with the variable cost to manage. Notably, the concept of the economies of scale also works for the government, non-profit organizations and individuals. The entity becomes more efficient as it produces more output and reduces cost as a result. The organization can benefit from the economics of scale, consequently, the consumers enjoy lower prices, and the economy expands to increase more demand. For huge businesses, economies of scale provide a competitive advantage over small enterprises. There are two types of economies of scale. The cost that the management can control is internal, while the cause for the cost to decrease attributed to geographic location, government policies, and industry changes are externals. Typically the internal economy of scale is found in large businesses as a…arrow_forwardA. How much is the fixed cost to produce the natural-organic oil? B. How many barrels of natural-organic oil should the firm produce to maximize its profit? C. How much is the price of the natural-organic oil per barrel? D. At what production level would the marginal cost exceed the average cost? E. How many barrels of natural-organic oil reflect the lowest minimum average variable cost?arrow_forwardA book publisher hires editors, designers, and production and marketing managers who help prepare books for publication. Because these employees work on several books simultaneously, the number of people the company hires will neither increase nor decrease with the quantity of books the company publishes during any particular year. The salaries and benefits of people in these job categories will be included in Select one: a. fixed cost and marginal cost but not variable cost. b. fixed cost but not variable cost and total cost. c. marginal cost and total cost but not fixed cost. d. fixed cost and total cost but not variable cost. e. Average variable costarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education