ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

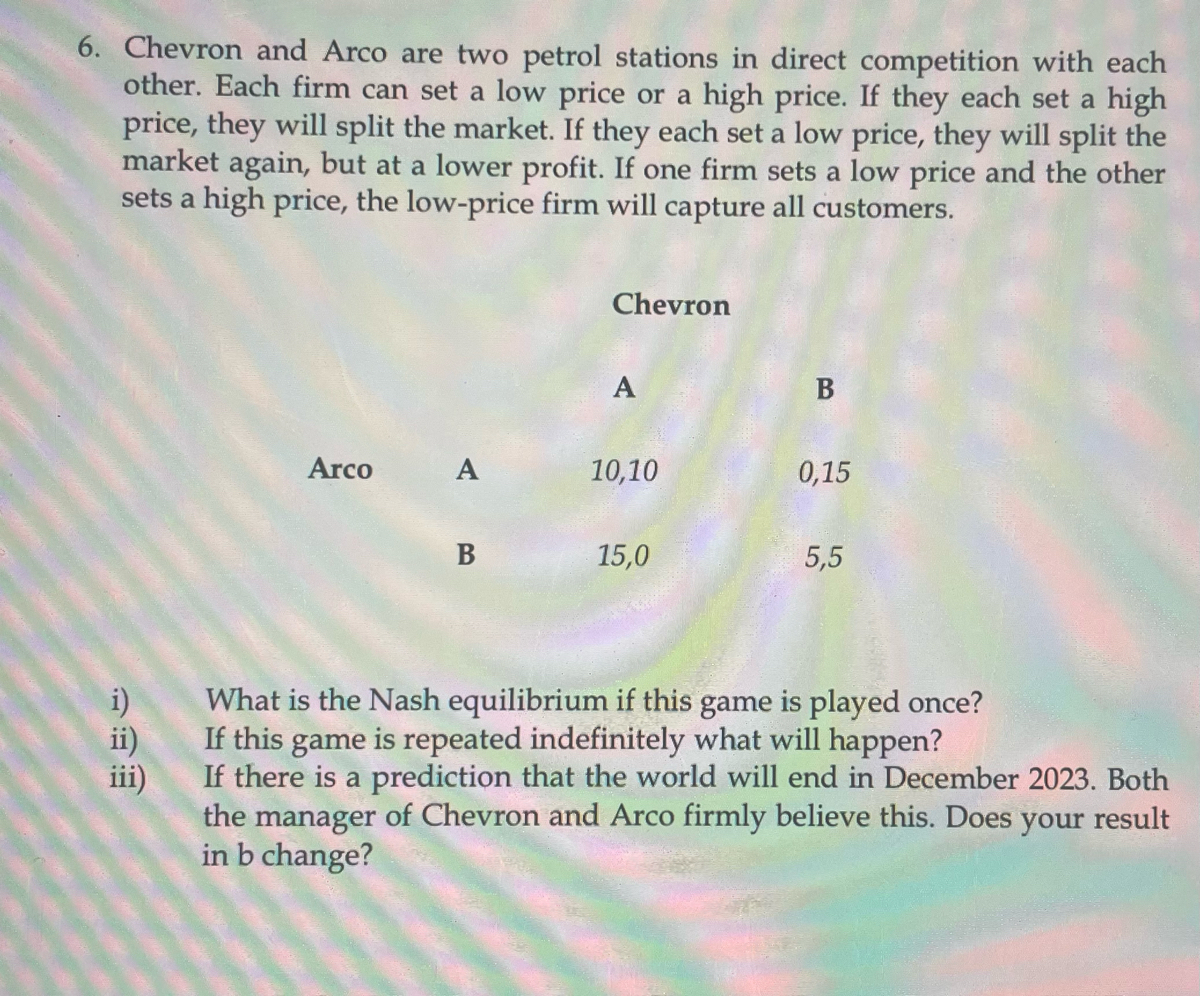

Transcribed Image Text:6. Chevron and Arco are two petrol stations in direct competition with each

other. Each firm can set a low price or a high price. If they each set a high

price, they will split the market. If they each set a low price, they will split the

market again, but at a lower profit. If one firm sets a low price and the other

sets a high price, the low-price firm will capture all customers.

Arco

38

A

B

Chevron

A

10,10

15,0

B

0,15

5,5

i) What is the Nash equilibrium if this game is played once?

If this game is repeated indefinitely what will happen?

If there is a prediction that the world will end in December 2023. Both

the manager of Chevron and Arco firmly believe this. Does your result

in b change?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 7. The table below shows the annual profits of two UK paint manufacturers. At present they both charge £20.00 per litre for gloss paint. Their annual profits are shown in box A. The other boxes show the effects on their profits of one or the other, or both firms reducing their price to £16.00 per litre. £20.00 Fenton's price i. ii. £16.00 A B £20.00 £6m each Mellow's price £9m for Fenton £3m for Mellow с £16.00 £3m for Fenton £9m for Mellow £4m each (a) Which of the two prices should Mellow charge if it assumes that Fenton will set its price at £20?. it assumes that Fenton will set its price at £16? ... (b) Which of the two prices should Fenton charge if i. ii. it assumes that Mellow will set its price at £20? it assumes that Mellow will set its price at £16? (c) Why is this known as a dominant strategy game? £20.00/£16.00 £20.00/£16.00 £20.00/£16.00 £20.00/£16.00 (d) Assume now that the 'game' between Fenton and Mellow has been played for some time with the result that they both learn…arrow_forward5. Individual Problems 9-5 Describe the difference in economic profit between a competitive firm and a monopolist in both the short and long run. Which should take longer to reach the long-run equilibrium? In the short run, both monopolists and competitive firms can competitive firms, but not monopolists earn positive economic profits. In the long run, can earn a positive economic profit. True or False: The adjustment to long-run equilibrium takes the same amount of time for monopolies and competitive industries. True O Falsearrow_forward1. When a monopoly advertises, the goal is to _____ because _____. Group of answer choices increase its demand as a share of market demand; the monopoly faces a significant portion of market demand increase market demand; the monopoly faces the entire market demand increase market demand; the monopoly produces a product that is identical to the output of all other sellers in the market increase its demand as a share of market demand; the monopoly faces a small portion of market demand 2. If given a choice, a person would prefer to experience the situation of which of the following families? Group of answer choices a family with income equal to the world poverty line a family with income equal to the United States poverty line a family with income double the world poverty line a family with income equal to the poverty line in the United States in 1970 3. A business using its bargaining power as a major buyer of labor to pay lower prices, including lower wages,…arrow_forward

- 8.In 2019, competition authorities threw out a merger of Asda and Sainsbury’s. What type of growth would the merger of Asda and Sainsbury’s have represented? a) Horizontal expansion b) Horizontal integration c) Conglomerate merger d) Vertical integration e) Horizontal alliancearrow_forward2. Suppose that the pizza market is monopolized by Domino's. Domino's has 100 identical plants to run, each with the same cost function as before, TC = 81 + 2q + q². The market demand is also the same as before QD = 1500 – 30P (a) What is Domino's revenue function? (b) What is Domino's profit maximizing level of output? What price does Domino's set to sell this level of output? (c) What is the profit earned at each one of Domino's plants?arrow_forwardCost (5) Please move point A to the minimum long-run average cost for a firm in an oligopoly and point B to the minimum long-run average cost for a firm in a purely competitive industry. LRAC LRAC исх A B Demand Why is the minimum long-run average cost important in determining an oligopoly? It occurs at a small fraction of industry demand. It is at the lowest possible cost among all firms. It occurs at a large fraction of industry demand. Firms cooperate with each other to achieve that low cost. Quantityarrow_forward

- 3. Firm A and Firm B are two firms in an industry. Firm A and Firm B are planning to merge. (a) Firm A and Firm B are Bertrand duopolists with identical and constant marginal costs. Post-merger marginal cost is lower than pre-merger. Use a figure that includes a downward-sloping linear market demand to show how the merger of Firm A and Firm B will lead to anticompetitive losses as well as cost-savings. (b) Firm A and Firm B are Cournot duopolists with identical marginal costs. Post- merger marginal cost is the same as pre-merger. Use a figure that includes a downward-sloping linear market demand to show how the merger of Firm A and Firm B will lead to anticompetitive losses. (c) Firm A and Firm B are Stackelberg competitors with identical marginal costs. Post-merger marginal cost is the same as pre-merger. Firm A is the Stackelberg leader. Use a figure that includes a downward-sloping linear market demand to show how the merger of Firm A and Firm B will lead to anticompetitive losses.…arrow_forward1. The table below shows the percentage of sales held by the four largest firms in an industry. Company A B C D Market share (percent of sales) 12 10 5 3 a) Calculate this industry's four-firm concentration ratio. b) Is this industry competitive? why? c) What market type does it most likely represent?arrow_forward6. Consider a duopoly in which inverse demand is given by P= 100-Q, where Pis the price and Q is aggregate output. The marginal cost of each firm is initially equal to 55 and there are no fixed costs. The firms compete by simultaneously setting quantities. (a) What is the equilibrium quantity of each firm, the equilibrium price and the profit of each firm? Now assume that one of the firms, firm 1, develops a new technology that reduces its own marginal cost to 25. (b) If firm 1 keeps this innovation for itself (so that the marginal cost of firm 2 is still 55), what will be the new equilibrium levels of output, price and profits of the two firms? What is the consumer surplus in the market? Do consumers benefit from the innovation?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education