Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

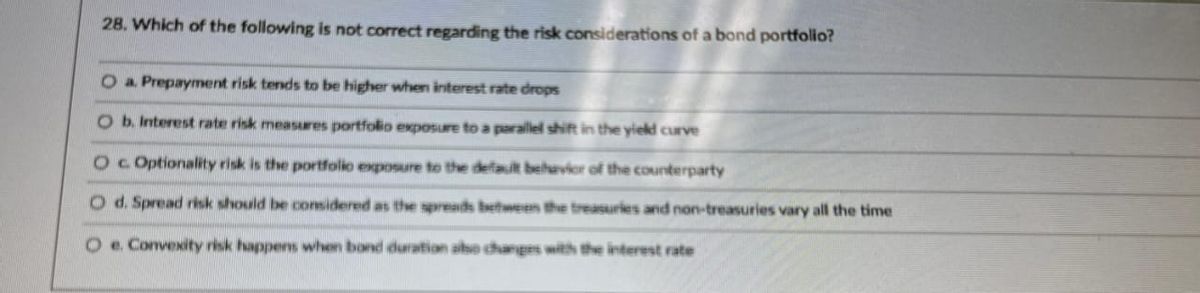

Transcribed Image Text:28. Which of the following is not correct regarding the risk considerations of a bond portfolio?

O a. Prepayment risk tends to be higher when interest rate drops

b. Interest rate risk measures portfolio exposure to a parallel shift in the yield curve

O c. Optionality risk is the portfolio exposure to the default behavior of the counterparty

O d. Spread risk should be considered as the spreads between the treasuries and non-treasuries vary all the time

Oe. Convexity risk happens when bond duration also changes with the interest rate

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- When a portfolio is diversified, what type of risk is reduced? Multiple Choice unsystematic risk systematic riskarrow_forwardUnsystematic risk: is compensated for by the risk premium. is measured by standard deviation. is related to the overall economy. can be effectively eliminated by portfolio diversification. is measured by beta.arrow_forward4. What are the various types of risk intrinsic to fixed-income portfolios?arrow_forward

- A portfolio's manager's views on the term structure of interest rates: "Yields reflect expected spot rates and risk premiums. Investors demand risk premiums for holding long-term bonds, and these risk premiums increase with maturity. This manager's views are most consistent with the: A. Segmented markets theory B. Local expectations theory C. Preferred habitat theory OD. Liquidity preference theoryarrow_forwardChanging the market risk premium A. Changes neither the y-intercept nor the slope of the security market line B. Changes only the y-intercept of the security market line C. Changes only the slope of the security market line D. Changes both the y-intercept and the slope of the security market linearrow_forwardWhich of the following statements is/are most CORRECT? O 11 A yield curve depicts the relationship between bond's 'time to maturity and its yield to maturity. 2) A premium bond's price will decline over time if the required return remains unchanged. 3) A discount bond's price will decline over time if the required return remains unchanged. 4) Both a and b are correct.arrow_forward

- 9.1 q1- How would you describe the relationship between risk and return for large portfolios of investments? Select one: a. There is no clear relationship. b. The relationship is precisely a positive linear relationship. c. The relationship approximates a positive linear relationship. d. The relationship approximates a negative linear relationship.arrow_forwardCheck all that are true with respect to the yield to maturity (YTM) and the expected return for a bond. Group of answer choices The expected return is based on the contractly obligated payments whereas the YTM is based on what the investors expect to receive The YTM is based on the promised payments whereas the expected return is based on the expected cash flows Higher YTMs always mean higher expected returns In the presence of non-zero default risk, the YTM will be higher than the expected return YTM is just another name for the expected returnarrow_forwardich of the following will not reduce risk in a portfolio? Select one: a. Selecting two securities that are perfectly positively correlated. b. Selecting two securities that are positively correlated. c. Selecting two securities that are perfectly negatively correlated. d. Selecting two securities that are negatively correlated.arrow_forward

- Which of the following statements is CORRECT? a. Lower beta stocks have higher required returns. b. A stock's beta indicates its diversifiable risk. c. Diversifiable risk cannot be completely diversified away. d. Two securities with the same stand-alone risk must have the same betas. e. The slope of the security market line is equal to the market risk premium.arrow_forwardGive typing answer with explanation and conclusion Question 16: Which of the following statements about convexity are true? I. Convexity accounts for the curvilinear function of bond rates II. A bond with a very low coupon and a long maturity will have low convexity III. A bond investor would seek to avoid bonds with high convexity. IV. Convexity is defined as the rate of change of the slope of the price/yield curve V. There is an inverse relationship between maturity and convexity a. I. b. II. III. IV. c. I. IV. d. II. IV. V. e. I. II. IV. V.arrow_forwardThe inverted yield curve predicts that bond prices will fall. Select one: True OR Falsearrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education