FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:l AT&T ?

5:05 PM

55%

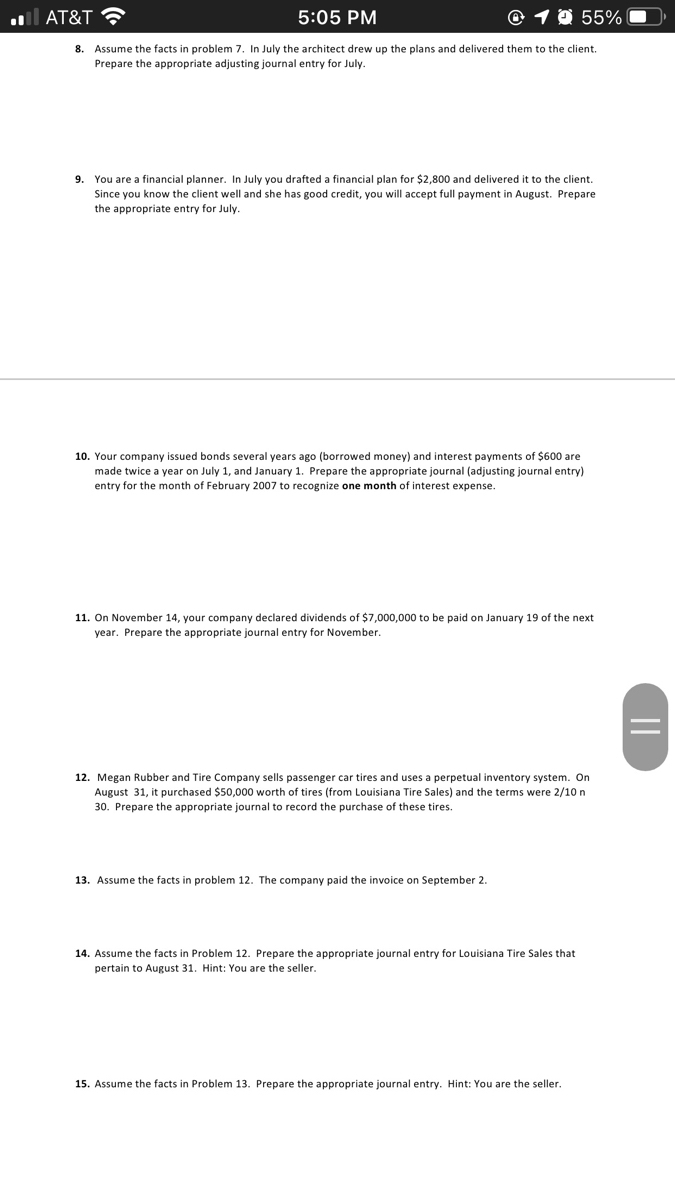

8. Assume the facts in problem 7. In July the architect drew up the plans and delivered them to the client.

Prepare the appropriate adjusting journal entry for July.

9. You are a financial planner. In July you drafted a financial plan for $2,800

Since you know the client well and she has good credit, you will accept full payment in August. Prepare

the appropriate entry for July.

delivered it to the client.

10. Your company issued bonds several years ago (borrowed money) and interest payments of $600 are

made twice a year on July 1, and January 1. Prepare the appropriate journal (adjusting journal entry)

entry for the month of February 2007 to recognize one month of interest expense.

11. On November 14, your company declared dividends of $7,000,000 to be paid on January 19 of the next

year. Prepare the appropriate journal entry for November.

12. Megan Rubber and Tire Company sells passenger car tires and uses a perpetual inventory system. On

August 31, it purchased $50,000 worth of tires (from Louisiana Tire Sales) and the terms were 2/10 n

30. Prepare the appropriate journal to record the purchase of these tires.

13. Assume the facts in problem 12. The company paid the invoice on September 2.

14. Assume the facts in Problem 12. Prepare the appropriate journal entry for Louisiana Tire Sales that

pertain to August 31. Hint: You are the seller.

15. Assume the facts

Problem 13. Prepare the appropriate journal entry. Hint: You are the seller.

Transcribed Image Text:l AT&T ?

5:05 PM

55%

Your company purchased six months worth

purchase price was $25,000.

1.

supplies on January 1. This is a credit purchase. The

f supplies was taken and $18,000 worth of

Assume the facts in problem 1. On March 31, an inventory

supplies was remaining in inventory.

2.

A one-year insurance policy was purchased on January 1, for $19,000. Cash was paid when the policy

was delivered.

3.

Assume the facts in problem 3. Record the appropriate adjusting journal entry for the month of

February.

5.

On March 1, 2016 conference room furniture for was purchased on credit for $12,000.

6.

Assume the facts in problem 5. The furniture has a 12 year life. Record the appropriate adjusting

entry.

On May 16, an architect was given $1,500 to draft house plans. The plans will be drawn up some time

in July. Prepare the appropriate journal entry for May.

7.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 7 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Blue, Inc., sells playground equipment to schools and municipalities. It mails invoices at the end of each month for all goods shipped during that month; credit terms are net 30 days. Sales and accounts receivable data for 20X1, 20X2, and 20X3 follow: Years Ending December 31, 20X1 20X2 20X3 Sales $ 1,785,980 $ 1,839,559 $ 1,986,724 Accounts receivable at year-end 220,189 227,896 267,094 Required: Calculate the rates of increase in sales and in receivables during 20X2 and 20X3. (Do not round intermediate calculations. Round "Sales grew" answers to the nearest whole percent and "Receivables grew" answers to 1 decimal place.) Do your calculations indicate any potential problems with Blue’s receivables?arrow_forwardWhich of the following summaries the effect of the payment of cash to settle the warranty claim in year 2 on the elements of the financial statementsarrow_forwardQuestion: The following transactions apply to Ozark Sales for Year 1: 1. The business was started when the company received $48,500 from the issue of common stock. 2. Purchased equipment inventory of $175,000 on account. 3. Sold equipment for $204,500 cash (not including sales tax). Sales tax of 7 percent is collected when the merchandise is sold. The merchandise had a cost of $129,500. 4. Provided a six-month warranty on the equipment sold. Based on industry estimates, the warranty claims would amount to 4 percent of sales. 5. Paid the sales tax to the state agency on $154,500 of the sales. 6. On September 1, Year 1, borrowed $21,500 from the local bank. The note had a 6 percent interest rate and matured on March 1, Year 2. 7. Paid $5,700 for warranty repairs during the year. 8. Paid operating expenses of $56,000 for the year. 9. Paid $124,100 of accounts payable. 10. Recorded accrued interest on the note issued in transaction no. 6. 1. Prepare the income statement for Year 1. 2.…arrow_forward

- Journal entries 1. Your company purchased six months worth of supplies on January 1. This is a credit purchase. The purchase price was $25,000. 2. Assume the facts in problem 1. On March 31, an inventory of supplies was taken and $18,000 worth of supplies was remaining in inventory. 3. A one-year insurance policy was purchased on January 1, for $19,000. Cash was paid when the policy was delivered. 4. Assume the facts in problem 3. Record the appropriate adjusting journal entry for the month of February. 5. On March 1, 2016 conference room furniture for was purchased on credit for $12,000. 6. Assume the facts in problem 5. The furniture has a 12 year life. Record the appropriate adjusting entry. 7. On May 16, an architect was given $1,500 to draft house plans. The plans will be drawn up some time in July. Prepare the appropriate journal entry for May.arrow_forwardLowell Company sells swimming pool supplies and equipment. The majority of Lowell's customers are small, family-owned businesses. Assume that Lowell Corporation completed the following transactions during the current year. Lowell's fiscal year ends on December 31. September 15 October 1 October 5 October 15 December 12 December 31 Required: Paid a supplier $129,500 for inventory previously purchased on credit. Borrowed $904,500 from Mass Bank for general use; signed an 11-month, 5% annual interest-bearing note for the money. Received a $42,250 customer deposit from Jim Scanlon for services to be performed in the future. Performed $19,800 of the services paid for by Mr. Scanlon. Received electric bill for $12,450. Lowell plans to pay the bill in early January. Determined wages of $52,900 earned but not yet paid on December 31 (disregard payroll taxes). 1.&2. Prepare journal entries for each of these transactions.arrow_forwardFinancial Transactions: Journalize the following transactions that occurred during the year: January 1: Received $100,000 cash in exchange for common stock. January 1: Purchased a delivery truck for $36,000 by paying $6,000 in cash and signing a note f remainder. January 15: Purchased $1,200 of supplies on account July 1: Paid $12,000 for an annual insurance policy. December 31: Made sales of $500,000 on the account. The Cost of Goods Sold was $300,000.arrow_forward

- 1. A company has a fiscal year-end of December 31: (1) on October 1, $13,000 was paid for a one-year fire insurance policy; (2) on June 30 the company advanced its chief financial officer $11,000; principal and interest at 5% on the note are due in one year; and (3) equipment costing $61,000 was purchased at the beginning of the year for cash.Prepare journal entries for each of the above transactions. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) 3. Equipment costing $61,000 was purchased at the beginning of the year for cash.arrow_forward1. During December, A Company started doing business and had gross credit trade sales of $800,000, terms 2/10 Net 30. The cost of goods sold of $480,000, selling general administration costs of $100,000, Interest Expense of $10,000; and an income tax rate of 30%. a. Prepare an income statement b. Prepare journal entries Assuming gross method and all payments for the trade sales were made within 10 days.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education