FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

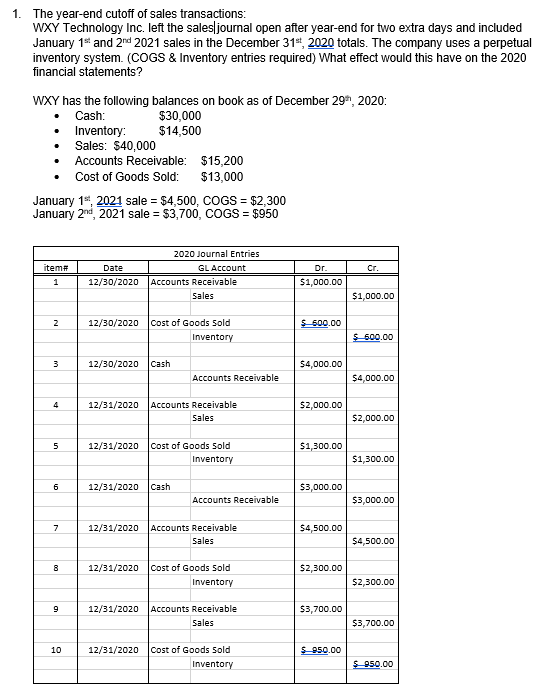

Transcribed Image Text:1. The year-end cutoff of sales transactions:

WXY Technology Inc. left the salesljourmal open after year-end for two extra days and included

January 1 and 2nd 2021 sales in the December 31*, 2020 totals. The company uses a perpetual

inventory system. (COGS & Inventory entries required) What effect would this have on the 2020

financial statements?

WXY has the following balances on book as of December 29, 2020:

Cash:

$30,000

$14,500

• Inventory:

• Sales: $40,000

• Accounts Receivable: $15,200

• Cost of Goods Sold:

$13,000

January 1*, 2021 sale = $4,500, COGS = $2,300

January 2nd, 2021 sale = $3,700, COGS = $950

2020 Journal Entries

item#

Date

GLAccount

Dr.

Cr.

1

12/30/2020

Accounts Receivable

$1,000.00

Sales

$1,000.00

2

12/30/2020

Cost of Goods Sold

S-500.00

Inventory

S600.00

3

12/30/2020

Cash

$4,000.00

Accounts Receivable

$4,000.00

4

12/31/2020

Accounts Receivable

$2,000.00

Sales

$2,000.00

5

12/31/2020

Cost of Goods Sold

$1,300.00

Inventory

$1,300.00

6

12/31/2020

Cash

$3,000.00

Accounts Receivable

$3,000.00

12/31/2020

Accounts Receivable

$4,500.00

Sales

$4,500.00

8

12/31/2020

Cost of Goods Sold

$2,300.00

Inventory

$2,300.00

9

12/31/2020

Accounts Receivable

$3,700.00

Sales

$3,700.00

10

12/31/2020

Cost of Goods Sold

S050.00

Inventory

도950.00

Transcribed Image Text:Use T-Account to show and calculate:

a) Balance for each account as WXY recorded at year end Dec. 31, 2020.

b) Identify the incorrect JE

c) Show Corrected Balance for each account, plus Gross Profit.

d) Determine the overstatements and/or understatements that would result from the

error, include Gross Profit.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 2 images

Knowledge Booster

Similar questions

- The financial statements of Crane, Inc's. 2025 annual report disclose the following information: (in millions) May 24, 2025 $250 ttempt in Progress Inventories Sales Cost of goods sold Net income (a) (b) 2025 Fiscal Year $3,900 1,300 320 May 25, 2024 $240 Inventory turnover 2024 $3,900 1,300 Compute Crane's (a) inventory turnover and (b) the average days to sell inventory for 2025 and 2024. (Round inventory turnover to 2 decimal places, e.g. 7.63 and average days to sell inventory to 1 decimal place, e.g. 65.1.) 300 Average days to sell inventory May 26, 2023 $200 2025 times days 2024 times daysarrow_forwardVaughn Limited, which uses a perpetual inventory system, purchased inventory costing $22,000 on February 1 by issuing a 3-month note payable bearing interest at 6%, with interest and principal due on May 1. The company's year end is on March 31 and the company records adjusting entries only at that time. (a) Your answer is correct. Prepare the journal entry to record the purchase of inventory on February 1. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts. List debit entry before credit entry.) (b) Date Account Titles Feb. 1 Inventory Notes Payable eTextbook and Media List of Accounts Mar. 31 Date Account Titles Debit 22000 Debit Credit Prepare the journal entry to record the accrual of interest expense on March 31. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required,…arrow_forwardVaughn Limited, which uses a perpetual inventory system, purchased inventory costing $22,000 on February 1 by issuing a 3-month note payable bearing interest at 6%, with interest and principal due on May 1. The company's year end is on March 31 and the company records adjusting entries only at that time. (a) Prepare the journal entry to record the purchase of inventory on February 1. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts. List debit entry before credit entry.) Date Account Titles Feb. 1 Debit Creditarrow_forward

- Emerald Corp. had total inventory of $65,000 at the beginning of February 2020. On February 2, it purchased inventory from a seller for $22,500 on credit with terms 2/15, n/30. Emerald received goods on February 10 and paid the total amount due on February 14. There were no other transactions during the month. Assuming a perpetual inventory system, what would be the cost of inventory at the end of February? =65000+22500(2%) =$64540 Steel Inc. was incorporated on January 1, 2019. At the end of 2019, it reported the following information for its first year of operations: net earnings $17,500, dividends $8,100, and contributed capital $180,000. At the end of 2020, it reported the following information: net earnings $28,000, dividends $11,000, and contributed capital $230,000. What was retained earnings at the end of 2020? 2019=0+17500-8100 =9400 2020=9400+28000-11000 =$25400arrow_forwardA company uses a perpetual system to record inventory transactions. The company purchases inventory on account on February 9, 2021, for $50,000 and then sells this inventory on account on March 7, 2021, for $70,000. Record the transactions for the purchase and sale of the inventory. (If no entry is required for a particular transaction/event select "No Journal Entry Required" in the first account field.)arrow_forwardAt year-end, the perpetual inventory records of Marigold Company showed merchandise inventory of $100,600. The company determined, however, that its actual inventory on hand was $96,900.Record the necessary adjusting entry. (Credit account titles are automatically indented when amount is entered. Do not indent manually.) Account Titles and Explanation Debit Credit eTextbook and Mediaarrow_forward

- The following selected accounts and the current balances apper in the ledger of Acct 201 Co., for the fiscal year ended May 31, 2020. To answer the questions below, it will be helpful to use a scratch piece of paper and prepare a multiple-step income statement (Note: not all of the listed accounts are used on the income statement. Select those that should appear on the income statement.) Advertising Expense $550Cost of Merchandise Sold 7,850Customer Refunds Payable 40Delivery Expense 16Depreciation Expense-Office Equipment 50Depreciation Expense-Store Equipment…arrow_forwardRecording Inventory Purchases and Sales on Account Record the entries for the following transactions for Shoppers Inc. Shoppers uses a perpetual inventory system and records sales taxes payable at the point of sale. a. On January 1, 2020, Shoppers Inc. purchased merchandise for resale for $56,000 on credit terms 1/15, n/30. Shoppers Inc. incurred a shipping charge of $288 on the purchase, which was immediately paid. Shoppers Inc. uses the gross method to record purchases. b. Shoppers Inc. sells $22,400 of inventory during the first week of January 2020, to customers for $40,000, with a sales tax rate of 5%. Of the total sales for the week, 30% are cash sales, and 70% are credit sales (n/30). c. On January 14, 2020, Shoppers Inc. pays the balance for purchases on account. d. Assume instead that Shoppers Inc. sells $24,000 of inventory during the first week of January 2020 to customers for $44,800, which includes a 5% sales tax. Of the total sales for the week, 30% are cash sales, and…arrow_forwardDuring 2021, your company completed the following summarized transactions. Prepare journal entries for the following events. 1. Your company sold $60,000 of merchandise to various customers for $150,000 on account, terms 2/10, n/30. Assume your company uses a PERIODIC inventory system and the GROSS method of discounts. 2. Accounts from transaction “#1." above for which the original amount was $70,000 were collected within the 10 day period. 3. Accounts from transaction "#1." above for which the original amount was $40,000 were collected 27 days after the sale. 4. One customer from transaction “#1" above returned a product which cost $410 and had been sold for $1,000. This customer had NOT paid his account so you credited his account. On December 1, 2021, you loaned $80,000 to another company and received a nine- month, 6% note. 5. 6. Your company wrote off $2,100 of past due accounts receivable. 7. At the end of the year, your company estimated bad debts would be 1% of GROSS sales for…arrow_forward

- Freedman Company estimates that sales this year of $12,000 will be returned next year and customers will be granted a full refund. Which of the following journal entries would Freedman Company record as part of its year-end adjustments assuming it uses the perpetual inventory system? a.Debit Estimated Returns Inventory for $12,000 and credit Income Summary for $12,000 b.Debit Sales Returns and Allowances for $12,000 and credit Cost of Goods Sold for $12,000 c.Debit Inventory Short and Over for $12,000 and credit Merchandise Inventory for $12,000 d.Debit Sales Returns and Allowances for $12,000 and credit Customer Refunds Payable for $12,000arrow_forwardDavis Inc. uses the gross method for recording purchase and sales discounts. They had the following transactions occur in October of 2022. Oct 1: Purchased inventory costing $5000, terms 2/10, n/30. Oct 8: Paid for the inventory purchased on Oct 1. Oct 18: Returned one-half of the inventory purchased on Oct 1 back to the supplier. The supplier will apply the return against future payables for Davis. Record the October transactions in the general journal assuming Davis Inc. uses the periodic and perpetual inventory.arrow_forwardDuring August 2024, Lima Company recorded the following: Requirements • Sales of $133,300 ($122,000 on account; $11,300 for cash). Ignore Cost of 1. Journalize Lima's transactions during August 2024, assuming Lima uses the direct write-off method. Goods Sold. • Collections on account, $106,400. 2. Journalize Lima's transactions during August 2024, assuming Lima uses the allowance method. • Write-offs of uncollectible receivables, $990. • Recovery of receivable previously written off, $800. Requirement 1. Journalize Lima's transactions during August 2024, assuming Lima uses the direct write-off method. Sales of $133,300 ($122,000 on account, $11,300 for cash). Ignore Cost of Goods Sold. (Record debits first, then credits. Select the explanation on the last line of the journal entratable. Prepare a single compound journal entry.) Accounts and Explanation Debit Credit Date Augarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education