ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

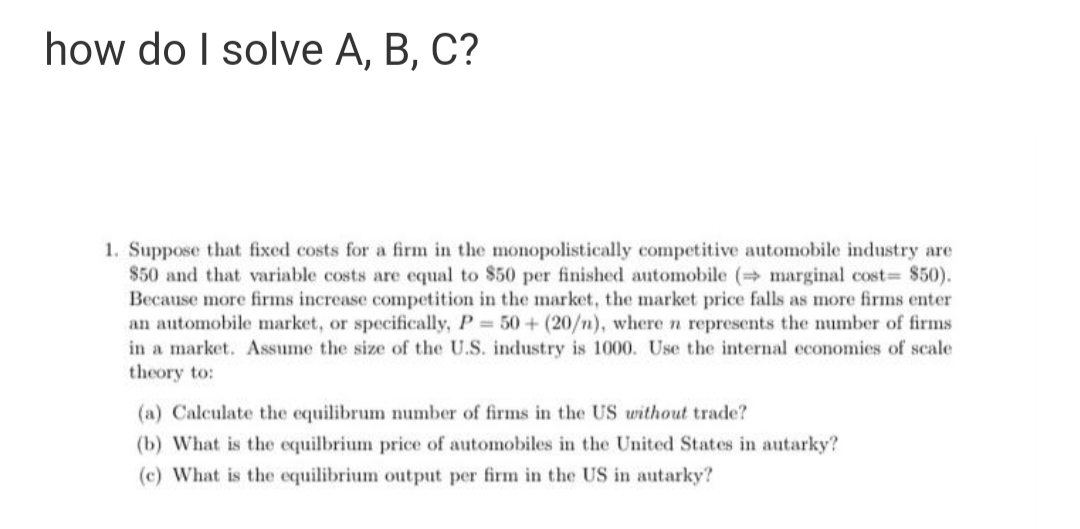

Transcribed Image Text:how do I solve A, B, C?

1. Suppose that fixed costs for a firm in the monopolistically competitive automobile industry are

$50 and that variable costs are equal to $50 per finished automobile ( marginal cost $50).

Because more firms increase competition in the market, the market price falls as more firms enter

an automobile market, or specifically, P 50+ (20/n), wheren represents the number of firms

in a market. Assume the size of the U.S. industry is 1000. Use the internal economies of scale

theory to:

(a) Calculate the equilibrum number of firms in the US without trade?

(b) What is the equilbrium price of automobiles in the United States in autarky?

(c) What is the equilibrium output per firm in the US in autarky?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 5 steps with 15 images

Knowledge Booster

Similar questions

- Suppose that demand is given by P = 1200 – Q and all firms have constant marginal cost of 800 per unit of output. If an innovator firm can reduce costs to 200 per unit of output, what price will it charge in order to capture the entire market?arrow_forward8. A monopolist with cost function c(q) = q faces two consumers whose demand functions are given below. Q₁ = 100-P 50-P Q₂ (a) Suppose the monopolist is a uniform pricing firm (i.e.the monopolist can- not engage in any price discrimination). Find the firm's optimal pricing strategy. Calculate the firm's Lerner index. (b) What is the deadweight loss associated with this pricing strategy, if any? (c) Now, assume that price discrimination is possible. Find the monopolist's optimal second degree price-discrimination strategy. (d) Find the monopolist's optimal third degree price-discrimination strategy.arrow_forward1. Consider the (inverse) market demand function for the market in streaming services. P = 120 - 4Q Assume further that the available technology results in Marginal Cost equal to $40. a) Graphically show the market outcome for monopoly, Cournot oligopoly and perfect competition. b) For monopoly, Cournot duopoly and perfect competition determine the optimal outcome. Clearly explain how you arrive at your answer. What are the market price and quantity under each market structure? c) What are the consumer surplus, producer surplus and total surplus under each scenario? d) Show the reaction function under Bertrand competition. What are the associated price and quantity?arrow_forward

- show all working.arrow_forward(b) Consider two firms, 1 and 2 , operating in a monopolistic competitive market. The cost functions of the firms are: TC_(1)=20+20 Q and TC_(2)=80+80Q, respectively. Would it be rational for both firms to compete in the world market, given the market demand curve of Q=100-P, and they have to bear a trade cost of $30 per unit? Explain with the help of a diagram. please give answer with compleete steps and diagram.arrow_forward1. It is 1908 and you are the CEO of Ford Motor Company. General Motors startedproducing cars this year and has quickly become your chief rival. Their recent entrance, as wellas your assembly line methods, allows you the advantage of producing cars faster and choosingyour output levels first. Assume the 1908 inverse demand function for cars is P = 3900 - Q(customers view cars as identical products at this point in time) and production costs are C(qi) =100qi. a. What is Ford’s profit-maximizing output level? GM's?b. What is the market equilibrium price?c. How much profit does each firm earn?d. As the assembly line is used by other firms, the first-mover advantage disappears (fast forward100 years to present day), and more firms have entered the market (e.g. FCA, Tesla, Hyundai,Toyota, Honda, etc.), what do you expect to happen to Ford’s profit (assume demand andcosts are the same)? Explain.e. From 1908 into the 1920s, Ford offered customers one car: the Model T. Further, Henry isfamous…arrow_forward

- You are the manager of the local movie theatre in a small town. Running a movie has a fixed cost of $2,000, but selling an extra ticket (i.e. accommodating an extra viewer) has zero marginal cost. Below are the demand schedules for your two types of customers: Price $ Adults Teens and Seniors 10 50 9 100 8 200 7 200 50 6 300 100 5 350 150 4 400 200 3 400 300 400 300 1 400 300 If you are to charge a single price (i.e., if price discrimination is prohibited), what price would you set for a ticket to maximize profit? How much profit do you make? Price = $ Profit = $ If you were allowed to price-discriminate, what price would you charge for an adult ticket? For senior/teen ticket? How much profit do you make? Price for adults = $ Price for seniors/teens= $ Profit = $arrow_forward7arrow_forwardUse the orange points (square symbol) to plot the initial short-run industry supply curve when there are 10 firms in the market. (Hint: You can disregard the portion of the supply curve that corresponds to prices where there is no output since this is the industry supply curve.) Next, use the purple points (diamond symbol) to plot the short-run industry supply curve when there are 15 firms. Finally, use the green points (triangle symbol) to plot the short-run industry supply curve when there are 20 firms. PRICE (Dollars per pound) 100 90 80 70 80 50 40 30 20 10 0 0 125 250 375 500 825 750 875 1000 1125 1250 QUANTITY (Thousands of pounds) Demand Because you know that competitive firms earn Supply (10 firms) True Supply (15 firms) If there were 10 firms in this market, the short-run equilibrium price of rhodium would be $ would . Therefore, in the long run, firms would False Supply (20 firms) per pound. From the graph, you can see that this means there will be ? per pound. At that price,…arrow_forward

- Suppose than an oligopolist is charging $20 per unit of output and selling 28 units each day. What is its daily total revenue? $ Also suppose that previously it had lowered its price from $20 to $18, rivals matched the price cut, and the firm's sales increased from 28 to 29 units. It also previously raised its price from $20 to $29, rivals ignored the price hike, and the firm's daily total revenue came in at $550. Which of the following is most logical to conclude? The firm's demand curve is (Click to select) < Prev Ne 28 of 50arrow_forward11. Consider the interaction between a retailer and a manufacturer. The manufacturer's marginal cost is 2 and it sets the price p in the first stage of the game. The retailer purchases the product from the manufacturer at this price (so the retailer treats p as its marginal cost) and sells the product at price r in the second stage of the game (this makes the retailer's profit function (r p)g). The market demand is q = 12 – 2r. What will be the prices set by the manufacturer and by the retailer?arrow_forwardIn 1983, Motorola accounted for seventy five percent of the mobile phone market. But by 2019, its market share had shrunk to just 2.2%. In 1983, the Motorola launched one of the world’s first commercially available mobile phones—the DynaTAC 8000X. Motorola went on to launch a few more devices over the next few years and quickly became a dominant player in the emerging industry. In the early days of the market, the company’s only serious competitor was Finnish multinational Nokia. By the mid-1990s, other competitors like Sony and Siemens started to gain some solid footing, which chipped away at Motorola’s dominance. In September 1995, the company’s market share was down to 32.1%. By January 1999, Nokia surpassed Motorola as the leading mobile phone manufacturer, accounting for 21.4% of global market share. That put it just slightly ahead of Motorola’s 20.8%. Describe the market for mobile phones in 1983 and illustrate how equilibrium price and quantity determined in this industry and…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education