FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

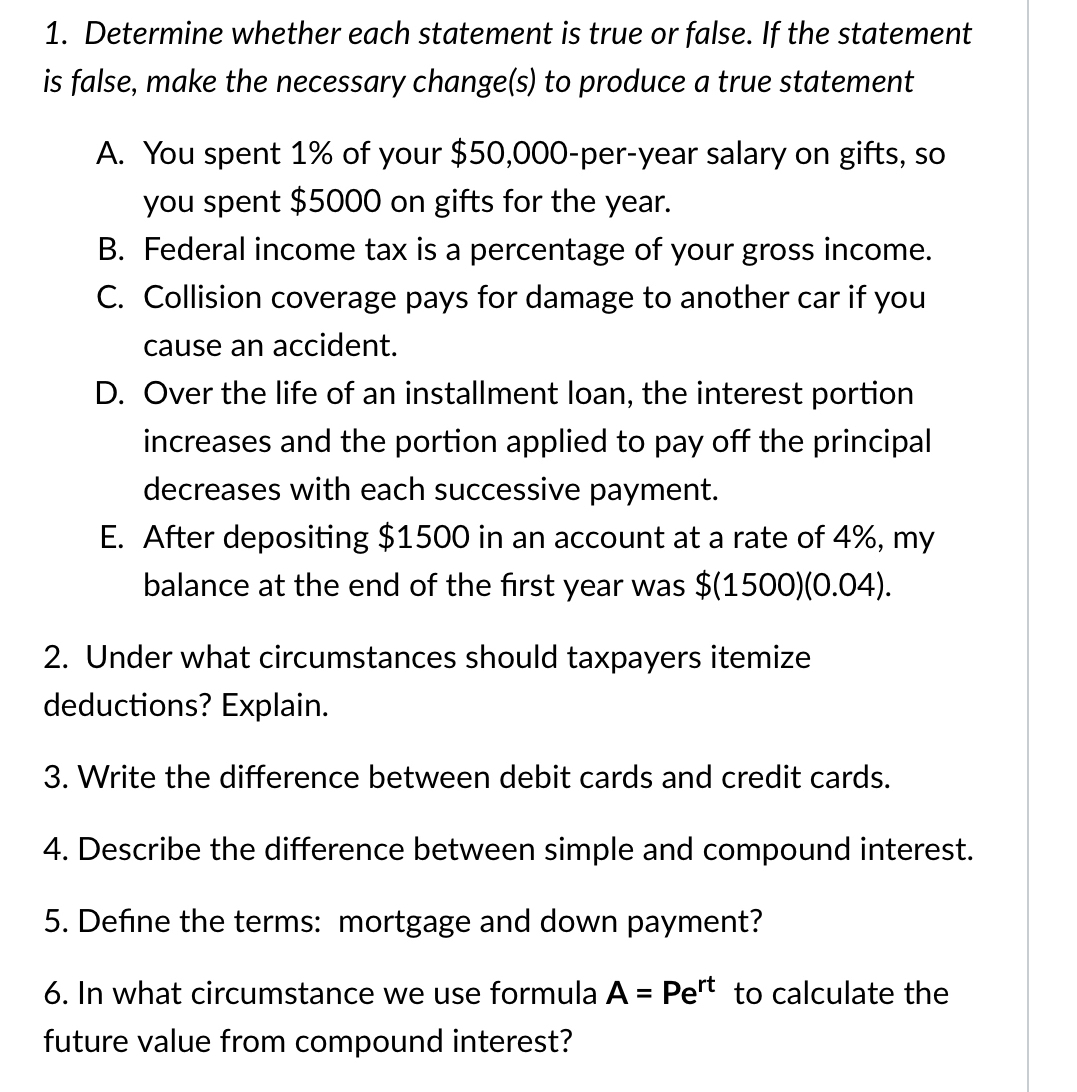

Transcribed Image Text:1. Determine whether each statement is true or false. If the statement

is false, make the necessary change(s) to produce a true statement

A. You spent 1% of your $50,000-per-year salary on gifts, so

you spent $5000 on gifts for the year.

B. Federal income tax is a percentage of your gross income.

C. Collision coverage pays for damage to another car if you

cause an accident.

D. Over the life of an installment loan, the interest portion

increases and the portion applied to pay off the principal

decreases with each successive payment.

E. After depositing $1500 in an account at a rate of 4%, my

balance at the end of the first year was $(1500)(0.04).

2. Under what circumstances should taxpayers itemize

deductions? Explain.

3. Write the difference between debit cards and credit cards.

4. Describe the difference between simple and compound interest.

5. Define the terms: mortgage and down payment?

6. In what circumstance we use formula A = Pert to calculate the

future value from compound interest?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- What dollar amount can you expect to receive if you file your taxes under a modest income? Select one:a. At least $350 over 12 months.b. At least $400 over 12 months.c. At least $250 over 12 months.d. At least $300 over 12 months.arrow_forward2. PLEASE, PERFORM THE EXERCISE IN EXCEL AND SHOW THE FORMULASEnrique Perez bought a house whose value is $1'900,000 cash. He paid $400,000 cash and the rest in 8 equal quarterly payments. If he is charged 10½ % nominal interest on the transaction, a) find the value of each of the quarterly paymentsb) find the total amount paid.c) Find the total amount of interest paid.d) Find the effective rate. Note:In the image, this is the original exercise, it is in Spanish, but it is easy to understand. Very important Note:It is necessary that you make a solution approach and then the result. Above all, to check the procedure and/or the formulas used, especially when you use excel.arrow_forwardAS an accountant at City Bank in Boston, Ken, the Loan Officer called you for some help on a loan application that he is working on. One of his customers is looking for a $50,000 loan for a car. He is offering him a 7% 5 year $50,000 loan and asking you to help him calculate the installment amount. This is the data Ken sent you: Face Amount of Loan $50,000 Contract Rate… 7% Term of the Loan….. 5 yearsarrow_forward

- Elizabeth makes the following interest-free loans during the year. Assume that tax avoidance is not a principal purpose of any of the loans. The relevant Federal rate is 5% and that the loans were outstanding for the last six months of the year. Borrower's Net Borrower Amount Investment Income Purpose of Loan Richard $5,000 $800 Gift Woody $8,000 $600 Stock purchase Irene $105,000 $0 Purchase principal residence By how much do each of these loans increase Elizabeth's gross income? If an amount is zero, enter "0". a. Richard is not subject to the imputed interest rules because the $10,000 gift loan exception does apply. Elizabeth's gross income from the loan is $ 0 b. The $10,000 exception does not income producing apply to the loan to Woody because the proceeds were used to purchase assets. Although the $100,000 exception applies to this loan, the amount of imputed interest is 1,000 X.Incorrect is $ 0 ✓. c. None of the exceptions apply gross income from the loan is $ to the loan to…arrow_forwardJoy had a tax refund of 733.43 due. She was able to get her tax refund immediately by paying a finance charge of 43.08 What simple interest rate is Joy paying for this loan assuming the following are true? Assume 360 days in a year. a) The tax refund check would be available in 5 days. b) The tax refund check would be available in 10 days. c) The tax refund check would be available in 20 days.arrow_forwardRussell bought a new hot tub today from Situation Hot Tubs. What is the present value of the cash flows associated with this transaction if the discount rate is 5.70 percent, he will receive a rebate of $527.00 from Situation Hot Tubs in 1 year, and he will pay $3,973.00 to Situation Hot Tubs in 4 years? Note: the correct answer is less than zero. $-2684.29(plus or minus 10$) $-3681.45(plus or minus 10$) $-2760.68(plus or minus 10$) $-2655.87(plus or minus 10$) None of the above has plus or minus $10 to correct answerarrow_forward

- A financial engineer designs a new financial instrument that she calls the SafetyNet. This instrument gives the holder access to the following cashflows: • For the first 4 years, the holder receives $95 per year starting one year from today (a total of 4 payments). • The holder does not receive any cashflows for year 5. • Starting at the end of year 6, the holder receives $60 growing at a rate of 4% per year forever. • The holder has to pay a “service fee” of $7 every year starting at the end of year 2; this goes on forever. The prevailing discount rate throughout is 6%. The financial engineer would like to determine a fair market price for this financial instrument. What do you suggest this price to be? Please show your work.arrow_forwardStefanie takes out a five year car loan and agrees to pay $500 every month. This scenario shows how money functions as a OA. store of value. B. standard of deferred payment. O c. unit of accounting. D. medium of exchange. Aarrow_forwardSubject;arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education