ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

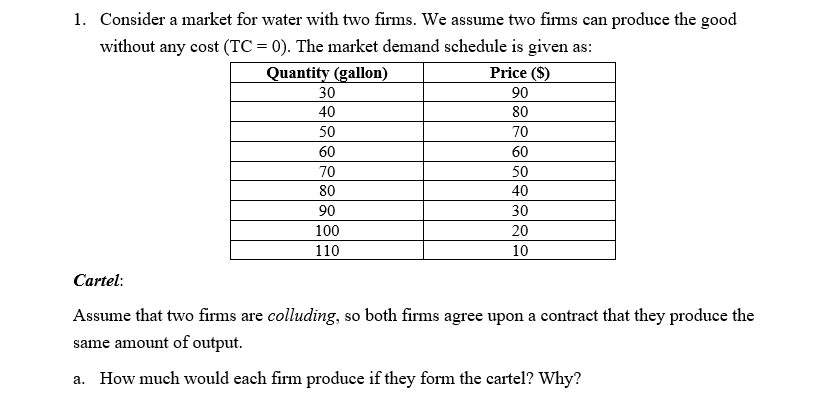

Transcribed Image Text:1. Consider a market for water with two firms. We assume two firms can produce the good

without any cost (TC= 0). The market demand schedule is given as:

Quantity (gallon)

Price ($)

30

90

40

80

50

70

60

60

70

50

80

40

90

30

100

20

110

10

Cartel:

Assume that two firms are colluding, so both firms agree upon a contract that they produce the

same amount of output.

a. How much would each firm produce if they form the cartel? Why?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider the following Cournot Duopoly diagram... Firm 1 Reaction Function r₁ A 6 C 0 E no Isoprofit curves for firm 1 Firm 2 Reaction Function 1₂ At what point is the Cournot equilibrium achieved? Q₁arrow_forwardQUESTION 1A) Two cournot competitors face inverse demand P = 50 - Q. Where, Q = q1+q2, is the total output of firms 1 and 2. What are the equilibrium output levels for q1 and q2, If firm 1 marginal cost is 1, and firm 2's marginal cost is 12? QUESTION 1B. Continuing with the inverse demand, P = 50 - Q, if each firm has a marginal cost of 0, what is the difference between the equilibrium price under Cournot competition and under Bertrand competition? b. C. d. a. The Cournot price is higher than the Bertrand price by 50. The Cournot price is lower than the Bertrand price by 25. The Cournot price is higher than the Bertrand price by 50/3. Equilibrium prices under Cournot and Bertrand are the same, so the difference is zero.arrow_forwardThe diagram illustrate an industry under oligopoly consisting of 10 equal-sized firms, and a particular firm in that industry. Each of the firms produces an identical product. To what output will an individual firm be restricted if the price is to be maintained?Assume that all firms are permitted to produce the same level of output. If the other firms stick to this output, how much would an individual firm be tempted to produce if it wished to maximize its own profit at the agreed price? If it undercut the cartel price, what and output would maximize its profit (assuming the other members did not retaliate)?arrow_forward

- The payoff matrix represents hypothetical profits (in thousands of dollars) that could be earned by two kumquat producers who have formed a cartel. Each seller must decide whether to abide by the quota or to exceed the quota. What is true of this game? Fun Fruit Exceed Quota Abide by Quota The Qinyang Terrace Exceed Quota FF = 15 FF = 10 QT = 15 QT = 22 Abide by Quota FF = 22 FF = 18 QT = 10 QT = 18 A. Both firms will choose to abide by the quota because that's where industry profit is maximized. B. Only Qinyang Terrace has a dominant strategy. C. Neither firm has a dominant strategy. D. The Nash equilibrium will occur where industry profit is the lowest possible number of all four outcomes. O E. If Fun Fruit decides to follow a maximin strategy, it will abide by the quota.arrow_forwardIf a market structure is an oligopoly, do Lexus, Cadillac, and Lincoln engage in sticky pricing? Who is the market leader?arrow_forwardSuppose that the central bank for this economy suddenly and unexpectedly decreases the money supply in an effort to reduce inflation. As a result of this unanticipated policy action, actual inflation falls to 3%. On the previous graph, use the black point (plus symbol labeled "B") to illustrate the short-run effects of this policy. Suppose that now, after a period of 3% inflation, households and firms begin to expect that the inflation rate will persist at the level of 3%. On the previous graph, use the purple line (diamond symbol) to draw SRPC₂, the short-run Phillips curve that is consistent with these expectations, assuming that it is parallel to SRPC₂- Finally, using the orange point (square symbol labeled "C"), indicate on the previous graph the new, long-run equilibrium for this economy. The inflation rate at point C is unemployment rate at point A. the inflation rate at point A, and the unemployment rate at point C is Was the central bank able to achieve its goal of lowering…arrow_forward

- Consider an industry that consists of 4 firms, all competing over the same market, given by the following demand equation: P=80-3Q All firms have the same Total Cost Function, given by: TC₁=10q,+2q Suppose the firms decide to collude and voluntarily restrict output and raise price, in order to increase profits. a) What price will be charged by the members of the cartel? Assume the head of the cartel is fair and distributes output q, equally among the 4 firms (since they have identical costs). b)What is the output of each individual firm? c) What is each individual firm's profit? We know that there is a built-in incentive for cartel members to cheat on the cartel. If, as a result, the cartel breaks down: d) What price will be charged in the market? e) Assuming each firm captures an equal share of the market, what now is each firm's output, q? f) What now is individual firm profit? g) Illustrate your answerarrow_forwardConsider two firms in the Australia market. The table below depicts each firm’s profits, depending on what price both firms charge. a. Find (if any) each firm's dominant strategy. b. Which strategy does each firm choose in equilibrium when collusion (joint agreement) is not allowed? c. Suppose that collusion is allowed between the two firms. Could these firms benefit from collusion? Why or why not?arrow_forwardPart 2: First Long Question There are two French bakeries in a small town: Le Meilleur Croissant (C), owned by Camille, and Le Meilleur Pain Au Chocolat (P), owned by Paul. In each period of an infinitely repeated game, they compete a la Bertrand, with market demand given by Q(pmin) = 10 - Pmin- Even though they sell identical goods, they have different marginal costs: cc = 2 and %3D Cp = 4 (Paul bakes just as well but is bad at business decisions). There are no fixed costs. Question 6 Turns out that Camille and Paul are married, and so they choose prices to maximize the joint profits of the two firms. Because both love baking and love each other, they also jointly decide that both firms should be selling positive amounts in their optimal plan. What prices do they choose? Pc = 6, pp = 11 Pc = 6.5, pp = 6.5 Pc = 6, pp = 6 Pc = 7, pp = 7 %3D O pc = 6, pp = 7arrow_forward

- Pleasant Island has two natural gas wells, one owned by Mack and the other owned by Tom. Each well has a valve that controls the rate of flow of gas, and the marginal cost of producing gas is zero. The table below gives the demand schedule for gas on this island. Price (dollars per unit) $100 88888; 70 50 30 20 10 0 Quantity Demanded (units per day) If Mack and Tom form a cartel and maximize their joint profits, the price of gas on Pleasant Island will be $ If Mack and Tom are forced to sell at the perfectly competitive price, the price of gas on Pleasant Island will be $ 5 15 25 35 45 55 65 per unit. (Enter your response as a whole number) per unit (Enter your response as a whole number)arrow_forwardQ8arrow_forwardSuppose that there are two firms producing a homogenous product and competing in Cournot fashion and let the market demand be given by 0 = 240 -5 Assume for simplicity that each firm operates with zero total cost. Find Cournot Nash equilibrium total surplus 72400 ৪9600 76800 81200arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education