ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

{kind=link}

Question

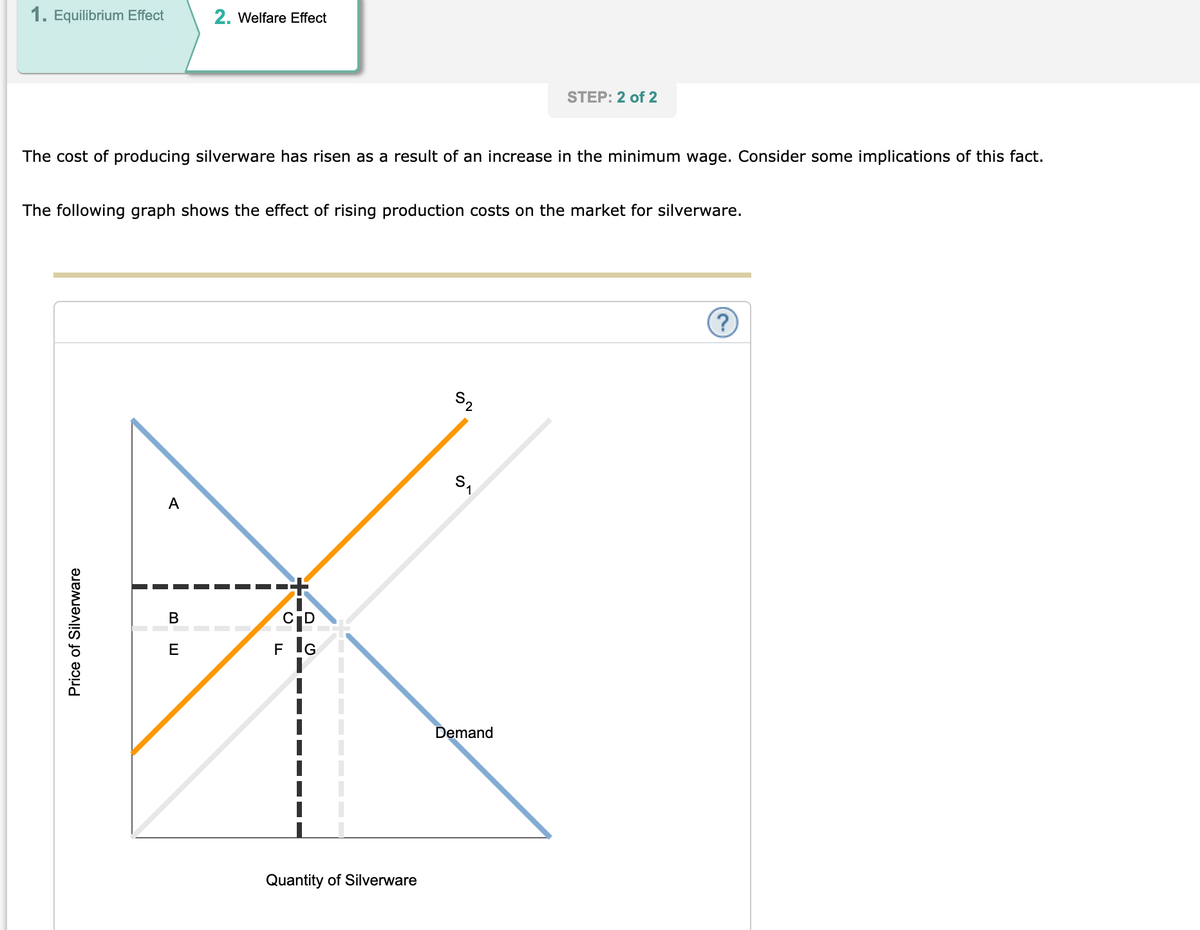

1) Complete the first two rows of the following table by indicating which areas on the graph represent

|

|

A |

B |

C |

D |

E |

F |

G |

|

|

Initial Consumer Surplus |

|

|

|

|

|

|

|

|

|

Initial Producer Surplus |

|

|

|

|

|

|

|

|

|

New Consumer Surplus |

|

|

|

|

|

|

|

|

|

New Producer Surplus |

|

|

|

|

|

|

|

|

2) True or False: Consumers are hurt most by rising production costs when the supply of silverware is very elastic.

|

True |

|

False |

Transcribed Image Text:1. Equilibrium Effect

2. Welfare Effect

STEP: 2 of 2

The cost of producing silverware has risen as a result of an increase in the minimum wage. Consider some implications of this fact.

The following graph shows the effect of rising production costs on the market for silverware.

S2

А

В

E

F IG

Demand

Quantity of Silverware

Price of Silverware

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- There are six potential consumers of computer games, each willing to buy only one game. The willingness to pay (WTP) of each is shown in the table. Consumer 1 2 3 4 5 6 f WTP $40 3.5 30 25 20 15 a. Suppose the market price is $29. What is the total consumer surplus? b. The market price decreases to $19. What is the total consumer surplus now? 59 Incorrect Incorrect Question Source: Krugman/Wells Se-Microeconomics | Publaher Worarrow_forwardIdentify the Surpluses. The graph to the right shows a supply curve and a demand curve and several areas in between. Identify the areas on the figure that represent the following: a. Consumer surplus in the market equilibrium: b. Producer surplus in the market equilibrium: c. Total surplus in the market equilibrium: d. Consumer surplus when the price is $6: e. Producer surplus when the price is $6: f. Total surplus when the price is $6: g. Consumer surplus when the quantity is 60: h. Producer surplus when the quantity is 60: i. Total surplus when the quantity is 60: Consumer and producer surplus 30- 28- 26- 24- 22- 20- 18 A 18- 16- 14- 12- B 10- D 6 Price 4- EL F - CE Supply Demand 0 20 40 60 80 100 120 140 160 180 Quantityarrow_forwardSuppose the daily demand curve for gasoline is as provided in the accompanying graph. a. Calculate the consumer surplus in the market for gasoline if the market price is $3.50. Consumer surplus = $ ___________ million Now suppose the price decreases to $2.50 per gallon. Move the price line on the graph to reflect this change, then calculate the new consumer surplus. New consumer surplus = $________millionarrow_forward

- 8. Total economic surplus The following diagram shows supply and demand in the market for tablets. Use the black point (plus symbol) to indicate the equilibrium price and quantity of tablets. Then use the green point (triangle symbol) to fill the area representing consumer surplus, and use the purple point (diamond symbol) to fill the area representing producer surplus.arrow_forwardThe graph shows the market for ice cream cones. On the graph, draw a shape that shows the producer surplus at market equilibrium. Producer surplus equals $ Enter your answer in dollars and cents (i.e. round at the second decimal place). 6.00- 5.50- 5.00 4.50- 4.00- 3.50- 3.00 2.50- 2.00 1.50- 1.00- 0.50 0.00 0 Price (dollars per ice cream cone) 5 10 15 20 30 25 Quantity (ice cream cones per day) S D 35 2arrow_forward2. 3-5: Attaining Market Equilibrium *3* The Wall Street Journal of March 20, 2020, reported on the "large surplus of oil" as there is not enough storage capacity to hold the refined oil. Assuming the price of oil is set by competitive market forces, which of the following sequence of events accurately describes how the surplus of oil would be eliminated? As price decreases, the: Quantity demanded decreases, quantity supplied increases, and a new equilibrium will be reached. O Quantity demanded increases, quantity supplied increases, and a new equilibrium will be reached. O Demand decreases, supply increases, and a new equilibrium will be reached. O Demand increases, supply decreases, and a new equilibrium will be reached. O Quantity demanded increases, quantity supplied decreases, and a new equilibrium will be reached.arrow_forward

- Table 1: Market for Skis P 0 20 40 60 80 Qd 25 20 15 10 5 100 0 Qs 0 4 8 12 16 20arrow_forward8. Consider the market for the Mona Lisa painting given by the following demand and supply curves: D: P = 1000-50QD and S: Qs=1 a. Draw the market for Mona Lisa paintings below. Label graph and axes. b. Calculate the equilibrium price and quantity of Mona Lisa paintings. Label P* and Q* on your graph from part a. C. Calculate consumer surplus and producer surplus. Label these (CS and PS) on your graph from part a. Suppose the French government imposed a $300 tax on buyers of Mona Lisa paintings. d. On the following graph, show the effect of the tax. Clearly label PBUYER PSELLER P, Q, QTAX CSTAX PSTAX, the tax revenue (TR), and DWL. (Here CSTAX PSTAX refer to consumer and producer surplus after the tax is imposed.) Calculate consumer surplus (CSTAX), producer surplus (PSTAX), deadweight loss (DWL), and the total tax revenue (TR) under the new tax. I e.arrow_forwardIn a supply-and-demand graph, producer surplus can be pictured as the Select one: a. vertical intercept of the supply curve. b. area between the demand curve and the supply curve to the left of equilibrium output. c. area under the supply curve to the left of equilibrium output. d. area under the demand curve to the left of equilibrium output. e. area between the equilibrium price line and the supply curve to the left of equilibrium output.arrow_forward

- Question 29 Describe where producer surplus is on the graph (use words or you can also draw and attach a drawing or photo of a drawing).arrow_forwardHere’s a quick problem to test whether you really understand what producer surplus and consumer surplus mean, rather than just relying on the geometry of demand and supply. For each of the two diagrams that follow, calculate producer surplus, consumer surplus, and total surplus. Assume the curves are perfectly vertical and perfectly horizontal.arrow_forward© Macmillan Learning b. How much does this new technology increase consumer surplus? Increase in consumer surplus: $ 1050 Increase in producer surplus: $ Incorrect c. How much does this new technology increase producer surplus? 1050 Incorrect d. How much does this new technology increase total (or social) surplus?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education