ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

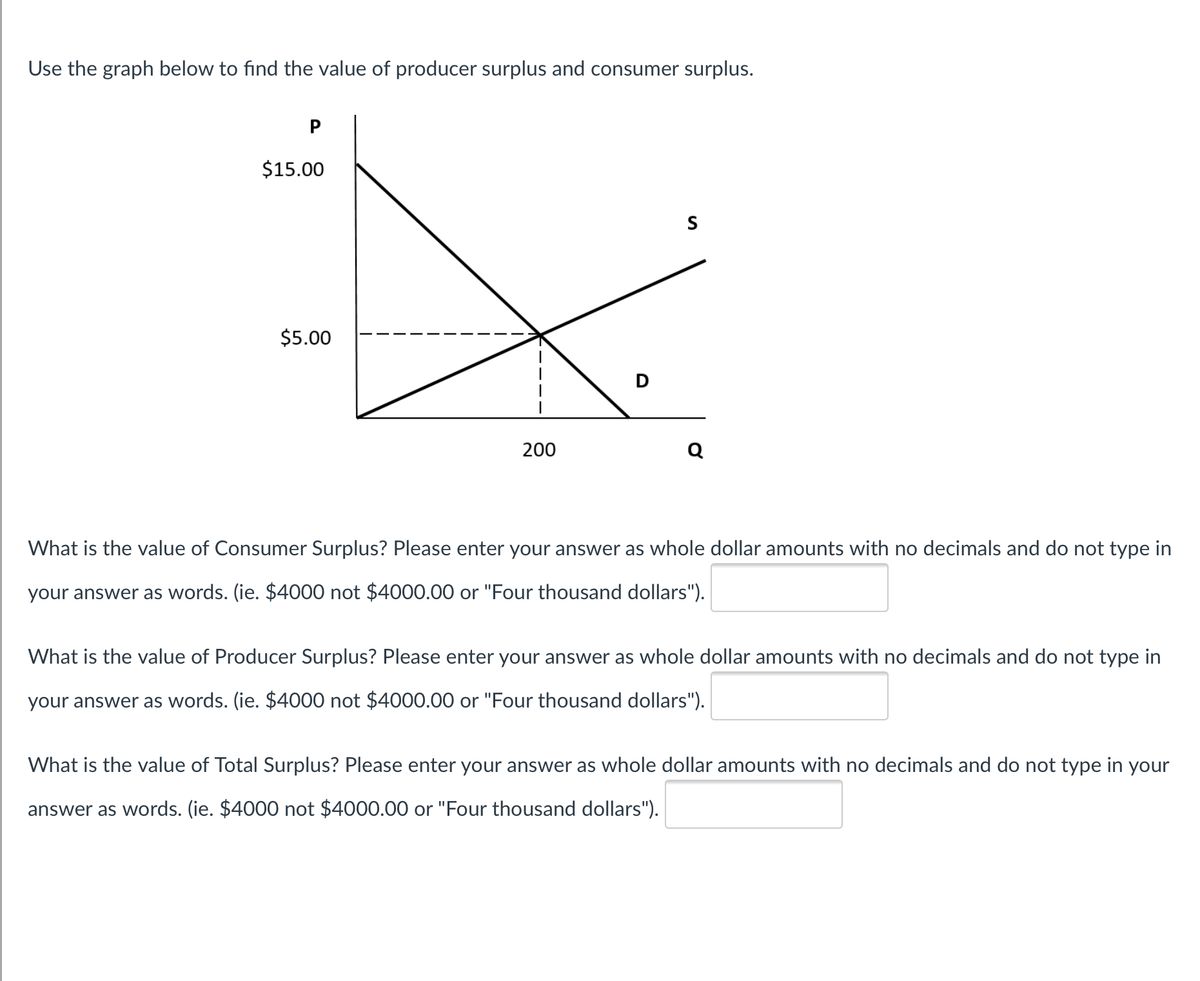

Transcribed Image Text:Use the graph below to find the value of producer surplus and consumer surplus.

$15.00

S

$5.00

D

200

Q

What is the value of Consumer Surplus? Please enter your answer as whole dollar amounts with no decimals and do not type in

your answer as words. (ie. $4000 not $4000.00 or "Four thousand dollars").

What is the value of Producer Surplus? Please enter your answer as whole dollar amounts with no decimals and do not type in

your answer as words. (ie. $4000 not $4000.00 or "Four thousand dollars").

What is the value of Total Surplus? Please enter your answer as whole dollar amounts with no decimals and do not type in your

answer as words. (ie. $4000 not $4000.00 or "Four thousand dollars").

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Please answer if you are 100% surearrow_forwarded Graphically, producer surplus is measured as the area Multiple Choice under the demand curve and below the actual price. under the demand curve and above the actual price. above the supply curve and above the actual price. above the supply curve and below the actual price.arrow_forwardQUESTION 8 In the above figure, the competitive (i.e. unregulated) market equilibrium quantity is? (Note #1: the x- axis is in thousands, so make sure to write out the entire number, i. e. 10 thousand as "10000") (Note #2: marginal benefit curve (MB) also represents demand)uppose the market demand for a good takes the form: Q subscript D equals 120 minus 1 fourth P and market supply takes the form: Q subscript S equals negative 30 plus 1 half P and production of each unit causes $30 in (external) damage. What is total surplus in this market? (Note: with external damages the overall benefit from a market is often referred to as "social welfare" instead of total surplus. Regardless, to answer this question subtract total external damages from consumer and producer surplus) QUESTION 8 40 40 S-MSC Price (dollars per vaccination) 20 20 30 30 50 60 10 10 MSB MB 0 10 20 30 40 50 60 Quantity (thousands of vaccinations per year) In the above figure, the competitive (i.e. unregulated) market…arrow_forward

- 34 q² and the supply curve p = 2+ q², find the producer surplus when the market is Given the demand curve p = in equilibrium. - Round your answer to three decimal places. The producer surplus is iarrow_forwardConsider a free market with demand equal to Q = 800 − 10P and supply equal to Q = 10P. What is the value of consumer surplus? What is the value of producer surplus?arrow_forwardFor years the government has subsidized higher education through grants; consider the demand and supply for college credit hours at a local private liberal arts collegeQD = 6,000 – 300PQS = 700P – 500 where P is the price, in hundreds of dollars, and Q is the number of credit hours per semester. Suppose the government subsidizes credit hours at a rate of $120 per hour. Calculate changes in consumer surplus. What is the size of the deadweight loss?arrow_forward

- What did Lewis mean when he wrote that there was a surplus of labor in agriculture? How does one measure that surplus? To what standard is labor in surplus, that is, in surplus relative to what?arrow_forwardQuestion 8 (1 point) Listen Junior's Sporting Goods sells camping equipment and outdoor gear. The company is willing to sell a particular fishing pole for as little as $55. Its main competitor is Sporty Gear, which is willing to sell the fishing pole for as little as $35. The current market price of that type of fishing pole is $75. What is the total producer surplus for the two firms? Your Answer: Answer Question 9 (1 point) Listen Karen can make 1 jackets or 17 ties in one day working at the clothing factory. Joe can make 8 jackets or 32 ties in one day working at the clothing factory. What is Joe's opportunity cost of producing 1 tie? Round your answer to one decimal place. Be sure to enter the correct units for what they are giving up. Your Answer: Answer unitsarrow_forwardThe market for N-95 masks is perfectly competitive. Market Demand is given by Q=486-2P and Market Supply is given by Q-2P. The government imposes a per-unit tax of $5, what is the market quantity with the tax? Note: you don't need to know who pays the tax to answer this question.arrow_forward

- Which of the following pairs of company profits and consumer surplus maximize welfare (or efficiency)? Question 8 options: Producer surplus = 90, Consumer surplus = 30 Producer surplus = 70, Consumer surplus = 70 Producer surplus = 100, Consumer surplus = 10 Producer surplus = 80, Consumer surplus = 50arrow_forwardConsider the market for a iced coffees. Each shop can make at most one drink. For shop A the marginal cost of making the coffee is $1.25, for shop B, it is $2.10, for shop C it is $3.00 and finally, for shop D it is $2.50. If the market price is P = $2.75 a. what is the quantity supplied? b. what is the total producer surplus?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education