ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

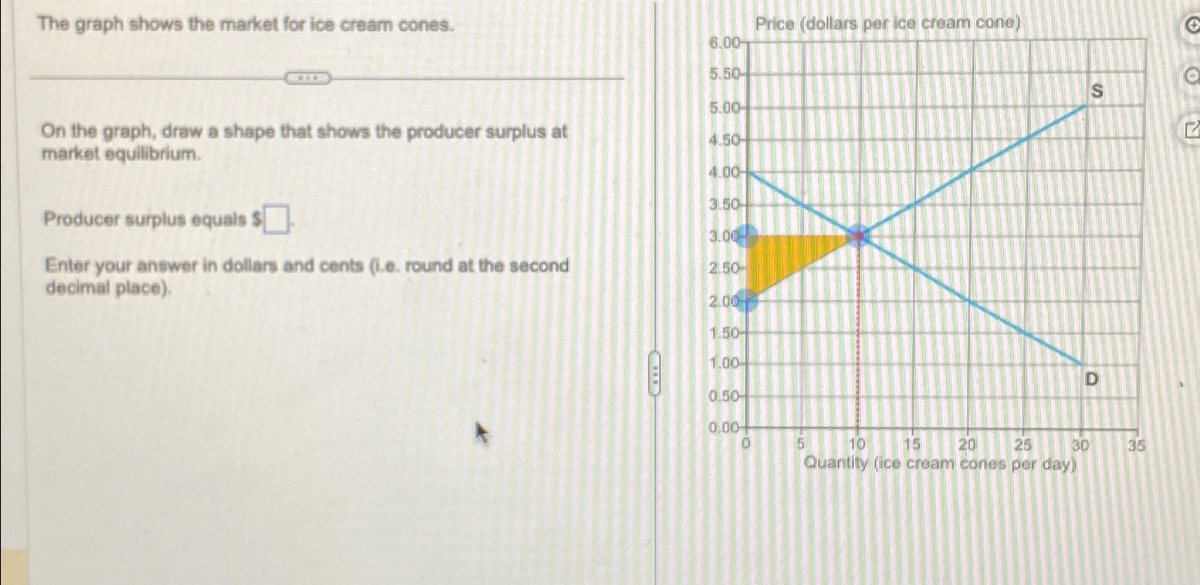

Transcribed Image Text:The graph shows the market for ice cream cones.

On the graph, draw a shape that shows the producer surplus at

market equilibrium.

Producer surplus equals $

Enter your answer in dollars and cents (i.e. round at the second

decimal place).

6.00-

5.50-

5.00

4.50-

4.00-

3.50-

3.00

2.50-

2.00

1.50-

1.00-

0.50

0.00

0

Price (dollars per ice cream cone)

5

10 15 20

30

25

Quantity (ice cream cones per day)

S

D

35

2

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A village has 4 farmers. Each summer, all the farmers graze their sheep on the village green. The cost of buying and caring for sheep is very small and can be regarded as 0. The value to a farmer of grazing a sheep on the green when a total of F sheep are grazing is v(F) per sheep: v(F) (price of a sheep) 1 $13 $12 3 $9 4 $7 $4 6+ $0 Suppose you are one of the 4 farmers in the game. Your optimal choice is to own (choose on) farmers chooses to own one (1) sheep. sheep if each of the other three Your optimal choice is to own (choose on). farmers chooses to own one (1) sheep. sheep if each of the other three 1 4.arrow_forwardAvis will pay a price as high as $900 for a new TV. After they purchase the TV they realize a consumer surplus of $200. What price did Avis pay for their new TV? Tyne vour numeric answer and submitarrow_forward' surplus For each of the scenarios, calculate the surplus and indicate if it is a producer surplus or a consumer Alice is willing to spend $30 on a pair of jeans, and has a coupon for $10 off which she found online. She selects and purchases a $35 pair of jeans which cost $35 pre-discount Alice has a Alice's surplus: $ producer surplus. surplus consumer Nicole has a hockey puck from the 2010 Winter Olympic Games and puts it up for sale on eBay. She will only sell the puck if the winning bid is greater than or equal to $500. After bidding closes, the last bid stands at $50o Nicole has a Nicole's surplus: $ producer surplus. consumer surplusarrow_forward

- 7. Producer Surplus Suppose the demand for tomato juice falls. Illustrate the effect this has on the market for tomato juice. Supply Demand Supply Demand Quantity of Tomato Juice Producer surplus in the market for tomato juice Price of Tomato Juicearrow_forwardng.cengage.com CENGAGE MINDTAP Chapter 08 Homework First, use the black point (plus symbol) to indicate the equilibrium price and quantity of electric scooters in the absence of a tax. Then use the green point (triangle symbol) to shade the area representing total consumer surplus (CS) at the equilibrium price. Next, use the purple point (diamond symbol) to shade the area representing total producer surplus (PS) at the equilibrium price. PRICE (Dollars per scooter) 300 270 Demand 240 210 180 150 120 90 Supply 60 30 Before Tax 0 0 140 280 420 560 700 840 980 QUANTITY (Scooters) 1120 1260 1400 Equilibrium A Consumer Surplus Producer Surplus Suppose the government imposes an excise tax on electric scooters. The black line on the following graph shows the tax wedge created by a tax of $120 per scooter. First, use the tan quadrilateral (dash symbols) to shade the area representing tax revenue. Next, use the green point (triangle symbol) to shade the area representing total consumer surplus…arrow_forwardQuestion 1 Laurasia has identified the following goods as its market basket. Here are the prices of those goods over three years. Compute the cost of that market basket in all three years. Instructions: Round your answers to two decimal places. Product Burgers Shoes Scissors Cost Basket Quantity 18 2015 3 2 2015 Price 2016 Price $ 8.00 $ 55.00 $ 7.00 $6.00 $ 50.00 $ 8.00 2016 2017 2017 Price $ 9.00 $ 45.00 $ 9.00arrow_forward

- Please helparrow_forwardI really need help with this question!arrow_forwardSuppose production is reduced by 60 percent for each of the suppliers in this industry. Draw a new market curve and answer the following questions based on your new supply curve and the original demand curve. In Table 3.1, the equilibrium market quantity would be Table 3,3 Individual Demand and Supply Schedules. Quantity Demanded By: Price 4.00 Ali Kelly Jessie Market 4 1 3.00 8 2.00 12 1.00 16 3.00 10 2.00 5 1.00 0 17 units Quantity Supplied by: Price Andy Maria Jose Market 4.00 15 15 11 9 7 5 12 units 25 units 9746 10 units 2 1234 11 7 3arrow_forward

- The following diagram shows supply and demand in the market for smartphones. Use the black point (plus symbol) to indicate the equilibrium price and quantity of smartphones. Then use the green point (triangle symbol) to fill the area representing consumer surplus, and use the purple point (diamond symbol) to fill the area representing producer surplus. PRICE (Dollars per phone) 300 270 240 210 180 150 60 30 0 0 Demand Supply 20 80 100 120 140 160 180 200 40 60 QUANTITY (Millions of phones) Total surplus in this market is $ million. Equilibrium Consumer Surplus Producer Surplus ?arrow_forwardA city passes a law that automobile prices may not increase. The auto market is currently in equilibrium. What will happen in that market if costs of producing autos increase? Selected answer will be automatically saved. For keyboard navigation, press up/down arrow keys to select an answer. a More than the allocatively efficient amount will be produced. b Less than the allocatively efficient amount will be produced. c The allocatively efficient amount will be produced but there will be a shortage. d The allocatively efficient amount will be produced but there will be a surplus.arrow_forwardProducer surplus and price changes The following graph shows the supply curve for a group of students looking to sell used smartphones. Each student has only one used smartphone to sell. Each rectangular segment under the supply curve represents the “cost,” or minimum acceptable price, for one student. Assume that anyone who has a cost just equal to the market price is willing to sell his or her used smartphone.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education