Concept explainers

Videos

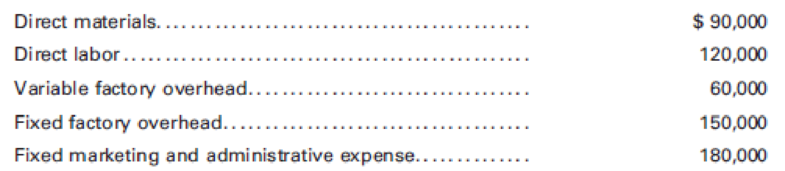

The chief executive officer of Acadia, Inc. attended a conference in which one of the sessions was devoted to variable costing. The CEO was impressed by the presentation and has asked that the following data of Acadia, Inc. be used to prepare comparative statements using variable costing and the company’s absorption costing. The data follow:

The factory produced 80,000 units during the period, and 70,000 units were sold for $700,000.

- 1. Prepare an income statement using variable costing.

- 2. Prepare an income statement using absorption costing.

(Round unit costs to three decimal places.)

Want to see the full answer?

Check out a sample textbook solution

Chapter 10 Solutions

Principles of Cost Accounting

Additional Business Textbook Solutions

Financial Accounting, Student Value Edition (4th Edition)

Intermediate Accounting (2nd Edition)

Advanced Financial Accounting

Managerial Accounting (5th Edition)

Managerial Accounting: Creating Value in a Dynamic Business Environment

Introduction To Managerial Accounting

- Jellison Company had the following operating data for its first two years of operations: Jellison produced 90,000 units in the first year and sold 80,000. In the second year, it produced 80,000 units and sold 90,000 units. The selling price per unit each year was 12. Jellison uses an actual costing system for product costing. Required: 1. Prepare income statements for both years using absorption costing. Has firm performance, as measured by income, improved or declined from Year 1 to Year 2? 2. Prepare income statements for both years using variable costing. Has firm performance, as measured by income, improved or declined from Year 1 to Year 2? 3. Which method do you think most accurately measures firm performance? Why?arrow_forwardEvans, Inc., has a unit-based costing system. Evanss Miami plant produces 10 different electronic products. The demand for each product is about the same. Although they differ in complexity, each product uses about the same labor time and materials. The plant has used direct labor hours for years to assign overhead to products. To help design engineers understand the assumed cost relationships, the Cost Accounting Department developed the following cost equation. (The equation describes the relationship between total manufacturing costs and direct labor hours; the equation is supported by a coefficient of determination of 60 percent.) Y=5,000,000+30X,whereX=directlaborhours The variable rate of 30 is broken down as follows: Because of competitive pressures, product engineering was given the charge to redesign products to reduce the total cost of manufacturing. Using the above cost relationships, product engineering adopted the strategy of redesigning to reduce direct labor content. As each design was completed, an engineering change order was cut, triggering a series of events such as design approval, vendor selection, bill of materials update, redrawing of schematic, test runs, changes in setup procedures, development of new inspection procedures, and so on. After one year of design changes, the normal volume of direct labor was reduced from 250,000 hours to 200,000 hours, with the same number of products being produced. Although each product differs in its labor content, the redesign efforts reduced the labor content for all products. On average, the labor content per unit of product dropped from 1.25 hours per unit to one hour per unit. Fixed overhead, however, increased from 5,000,000 to 6,600,000 per year. Suppose that a consultant was hired to explain the increase in fixed overhead costs. The consultants study revealed that the 30 per hour rate captured the unit-level variable costs; however, the cost behavior of other activities was quite different. For example, setting up equipment is a step-fixed cost, where each step is 2,000 setup hours, costing 90,000. The study also revealed that the cost of receiving goods is a function of the number of different components. This activity has a variable cost of 2,000 per component type and a fixed cost that follows a step-cost pattern. The step is defined by 20 components with a cost of 50,000 per step. Assume also that the consultant indicated that the design adopted by the engineers increased the demand for setups from 20,000 setup hours to 40,000 setup hours and the number of different components from 100 to 250. The demand for other non-unit-level activities remained unchanged. The consultant also recommended that management take a look at a rejected design for its products. This rejected design increased direct labor content from 250,000 hours to 260,000 hours, decreased the demand for setups from 20,000 hours to 10,000 hours, and decreased the demand for purchasing from 100 component types to 75 component types, while the demand for all other activities remained unchanged. Required: 1. Using normal volume, compute the manufacturing cost per labor hour before the year of design changes. What is the cost per unit of an average product? 2. Using normal volume after the one year of design changes, compute the manufacturing cost per hour. What is the cost per unit of an average product? 3. Before considering the consultants study, what do you think is the most likely explanation for the failure of the design changes to reduce manufacturing costs? Now use the information from the consultants study to explain the increase in the average cost per unit of product. What changes would you suggest to improve Evanss efforts to reduce costs? 4. Explain why the consultant recommended a second look at a rejected design. Provide computational support. What does this tell you about the strategic importance of cost management?arrow_forwardMethod of Least Squares, Predicting Cost for Different Time Periods from the One Used to Develop a Cost Formula Refer to the information for Farnsworth Company on the previous page. However, assume that Tracy has used the method of least squares on the receiving data and has gotten the following results: Required: 1. Using the results from the method of least squares, prepare a cost formula for the receiving activity. 2. Using the formula from Requirement 1, what is the predicted cost of receiving for a month in which 1,450 receiving orders are processed? (Note: Round your answer to the nearest dollar.) 3. Prepare a cost formula for the receiving activity for a quarter. Based on this formula, what is the predicted cost of receiving for a quarter in which 4,650 receiving orders are anticipated? Prepare a cost formula for the receiving activity for a year. Based on this formula, what is the predicted cost of receiving for a year in which 18,000 receiving orders are anticipated?arrow_forward

- Following is the revenue and cost data for Metlock Ltd. in the manufacturing of luxury shower curtains for the year ended December 31, 2022: NewsVariable manufacturing costs $34 per curtainVariable selling and administrative expenses $8 per curtain Fixed manufacturing overhead $53,900Fixed selling and administrative expenses $184,800 Units produced and sold 7, 700Selling price $84 per curtain. Prepare an income statement using absorption costing. Prepare an income statement using variable costing.arrow_forwardConsider the following information for Presidio Incorporated's most recent year of operations. Number of units produced Number of units sold Sales price per unit Direct materials per unit Direct labor per unit Variable manufacturing overhead per unit Fixed manufacturing overhead per unit ($282,960 2,400 units) Total variable selling expenses ($14 per unit sold) Total fixed general and administrative expenses Complete this question by entering your answers in the tabs below. Required: 2-a. Complete a full absorption costing income statement for Presidio. Assume there was no beginning inventory. 2-b. Complete a contribution margin income statement for Presidio. Assume there was no beginning inventory. 3. Compute the difference in profit between full absorption costing and variable costing. Req 2A Reg 2B 2,400 1,500 $ 630.00 65.00 95.00 45.00 117.90 Req 3 Gross Margin Less: Non-Manufacturing Expenses 21,000.00 74,000.00 Complete a full absorption costing income statement for Presidio.…arrow_forwardYou are working as a manager accountant for a retail company which markets and sells two products product 1 and product 2. The following information is available for last year. The actual fixed product overheads for the same period were 95000 and fixed administration overheads were 25000. a) Please develop both marginal costing and absorption costing income statements. b) elaborate the findings, key advantages and limitations. Please donot provide solution in image format provide solution in step by step format and fast solutionarrow_forward

- Absorption costing is a widely used accounting method for costing and reporting on the total production cost of goods or services within an organization. It involves allocating both variable and fixed manufacturing costs to the cost of products. With that in mind, consider the following scenario: ABC Manufacturing Company produces electronic gadgets. In a given accounting period, the company manufactured and sold 10,000 units of their flagship gadget. The following data is available: Direct materials cost per unit: $50 Direct labor cost per unit: $30 Variable manufacturing overhead cost per unit: $20 Fixed manufacturing overhead cost for the period: $50,000 Selling and administrative expenses (all fixed): $30,000 Selling price per gadget: $200 Using absorption costing, calculate the following: A. The total manufacturing cost per unit of the electronic gadget. B. The total cost of goods manufactured during the accounting period. C. The ending inventory value of the manufactured gadgets.…arrow_forwardAs a new accountant of the company, you are provided with the following information related to KOKO: Product Annual production and sales unit Direct material cost per unit Direct labour cost per unit Machine hours per unit Selling price per unit Koko 5,500 RM50 RM35 3 hours RM150 The company is considering of changing the traditional method to the Activity Based Costing (ABC) method. In order to adopt ABC method the following information is required: Activity Cost Cost Driver Pool Expected overhead Expected use of drivers per product Other products 3,500 costs Коко (RM) No of purchase orders Machine hours Maintenance Maintenance hours Number of inspections Total Purchasing 4,000 37,500 Machining 16,500 8,000 1,500 147,000 43,000 3,500 Quality control 1900 1600 17,500 245,000 Required: a. If the company decided to use the Activity Based Costing (ABC) method, determine the cost per unit of KOKO. Based on your answer in (a), advise whether the company should change to ABC method. Support…arrow_forwardThe managerial accountant at Organic Beverage Factory used spreadsheet software to run a regression analysis scenario and compile the following monthly cost data: Organic Beverage Factory Intercept coefficient X Variable 1 Coefficient $4,286,652 $28.21 R-square 0.6521 Which of the following is the correct cost equation showing the correlation of monthly costs, based on the results of the regression analysis compiled by the managerial accountant? O A. y $4,286,652 $28.21 O B. y $0.6521 $28.21x O C. y $28.21x + $4,286,652 O D. y 0.6521x + $4,286,652arrow_forward

- Please give me instruction on the following step by step: Variable Costing Income Statement The following data were adapted from a recent income statement of Bluth Company: (in millions) Sales $313,680 Operating costs: Cost of products sold $150,570 Marketing, administrative, and other expenses 100,380 Total operating costs $250,950 Income from operations $62,730 Assume that the variable amount of each category of operating costs is as follows: (in millions) Cost of products sold $84,690 Marketing, administrative, and other expenses 40,780 a. Based on the data given, prepare a variable costing income statement for Bluth Company, assuming that the company maintained constant inventory levels during the period. Bluth Company Variable Costing Income Statement (in millions) $ $ $ Fixed costs: $ Income from operations $ b. If Bluth Company reduced its…arrow_forwardThe following information is available from the accounting records of EVA Corporation:Fixed cost per period is $4800. Sales volume for the last period was $19 360, and variable cost was $13 552. Capacity per period is a sales volume of $32 000.Draw a detailed break-even chart on a grid such as the one provided. Marks are awarded for determining the revenue and cost functions, correctness of plotted points and lines, correct labeling of axes, and overall neatness of the graph.arrow_forwardHi-Tek Manufacturing, Inc., makes two types of industrial component parts-the B300 and the T500. An absorption costing income statement for the most recent period is shown: Hi-Tek Manufacturing Inc. Income Statement $ 1,714,000 1,237,202 476,798 Sales Cost of goods sold Gross margin Selling and administrative expenses 610,000 Net operating loss $ (133,202) Hi-Tek produced and sold 60,300 units of B300 at a price of $20 per unit and 12,700 units of T500 at a price of $40 per unit. The company's traditional cost system allocates manufacturing overhead to products using a plantwide overhead rate and direct labor dollars as the allocation base. Additional information relating to the company's two product lines is shown below: B300 T500 Total $ 400,800 $ 120,100 Direct materials $ 162,500 $ 563,300 162,600 511,302 Direct labor $ 42,500 Manufacturing overhead Cost of goods sold $ 1,237,202arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning