a.

To determine: The betas for the stocks

Introduction: Systematic risk is also known as volatility or non- diversifiable risk. It is the risk that is assumed by everyone before investing in a market. This kind of risk is unpredictable.

a.

Answer to Problem 9PS

The beta value for aggressive and defensive stock is 2.00 and 0.30 respectively

Explanation of Solution

Given Information: Market return, aggressive stock and the defensive stock is given

Beta measures an investment’s volatility as it correlates to market volatility. When beta value more than 1, it means the investment has more systematic risk than the market. If beta less than 1, it means less systematic risk. When beta equals to 0, the investment has same systematic risk as the market.

So, the beta value is 2.00 and 0.30 for aggressive and defensive stock respectively.

b.

To determine: The expected

Introduction: Systematic risk is also known as volatility or non- diversifiable risk. It is the risk that is assumed by everyone before investing in a market. This kind of risk is unpredictable.

b.

Answer to Problem 9PS

The expected rate of return for aggressive stock and for the defensive stock is 18% and 9% respectively.

Explanation of Solution

Given Information: Market return, aggressive stock and the defensive stock is given

The

Calculation of expected rate of return (Aggressive Stock),

By substituting the value of 2% and 38%,

The expected rate of return (aggressive stock) is 18%

Calculation of expected rate of return (Defensive Stock),

The expected rate of return (Defensive stock) is 9%

c.

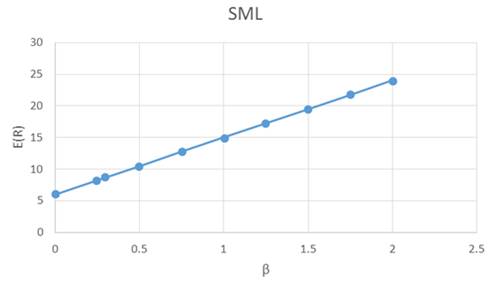

To determine: The SML for the economy

Introduction: Systematic risk is also known as volatility or non- diversifiable risk. It is the risk that is assumed by everyone before investing in a market. This kind of risk is unpredictable.

c.

Answer to Problem 9PS

The SML for the economy is shown in the graph

Explanation of Solution

Given Information: Market return, aggressive stock and the defensive stock is given

The capital asset pricing model describes the expected return on beta based security. This model is used for determine the expected return on asset, which is based on systematic risk.

The expected rate of return of each stock,

Now substituting the value of Expected rate of return on market,

So, SML is,

The SML with the market return in the graph is,

d.

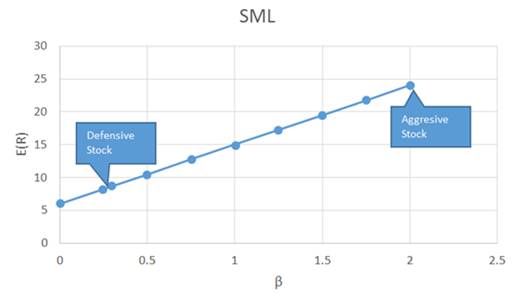

To determine: The alphas of each stock

Introduction: Systematic risk is also known as volatility or non- diversifiable risk. It is the risk that is assumed by everyone before investing in a market. This kind of risk is unpredictable.

d.

Answer to Problem 9PS

The alpha of defensive stock is 8.7% and for the aggressive stock is (-6%)

Explanation of Solution

Given Information: Market return, aggressive stock and the defensive stock is given

The capital asset pricing model describes the expected return on beta based security. This model is used for determine the expected return on asset, which is based on systematic risk.

The stocks on SML graph,

Calculation of alpha value for defensive stock,

Calculation of alpha value for aggressive stock,

So, the value of alpha is (-6%) for aggressive stock

e.

To determine: The hurdle rate used by the management for a project

Introduction: Systematic risk is also known as volatility or non- diversifiable risk. It is the risk that is assumed by everyone before investing in a market. This kind of risk is unpredictable.

e.

Answer to Problem 9PS

8.7% is the hurdle rate for the project

Explanation of Solution

Given Information: Market return, aggressive stock and the defensive stock is given

The capital asset pricing model describes the expected return on beta based security. This model is used for determine the expected return on asset, which is based on systematic risk.The hurdle rate can be calculated by the beta value of the project. The hurdle rate is the expected rate of return for the defensive stock.

Calculate the discount rate for the project,

By substituting the value of expected rate of market and beta value,

So, the hurdle rate is 8.7%

Want to see more full solutions like this?

Chapter 9 Solutions

INVESTMENTS(LL)W/CONNECT

- Consider the following table, which gives a security analyst’s expected return on two stocks in two particular scenarios for the rate of return on the market: Market Return Aggressive Stock Defensive Stock 5% -3 4% 24 36 9 a. What are the betas of the two stocks? (Do not round intermediate calculations. Round your answers to 2 decimal places.) b. What is the expected rate of return on each stock if the two scenarios for the market return are equally likely to be 5% or 24%? (Do not round intermediate calculations. Round your answers to 1 decimal place.) c. What hurdle rate should be used by the management of the aggressive firm for a project with the risk characteristics of the defensive firm’s stock if the two scenarios for the market return are equally likely? Also, assume a T-Bill rate of 4%. (Do not round intermediate calculations. Round your answer to 2 decimal places.)arrow_forwardConsider the following table, which gives a security analyst's expected return on two stocks in two particular scenarios for the rate of return on the market: Market Return Aggressive Stock Defensive Stock 4% -2% 5% 25 36 11 a. What are the betas of the two stocks? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Beta Aggressive stock Defensive stock b. What is the expected rate of return on each stock if the two scenarios for the market return are equally likely to be 4% or 25%? (Do not round intermediate calculations. Round your answers to 1 decimal place.) Expected Rate of Return Aggressive stock % Defensive stock % e. What hurdle rate should be used by the management of the aggressive firm for a project with the risk characteristics of the defensive firm's stock if the two scenarios for the market return are equally likely? Also, assume a T-Bill rate of 5%. (Do not round intermediate calculations. Round your answer to 2 decimal places.) Hurdle rate…arrow_forwardConsider the following table, which gives a security analyst's expected return on two stocks in two particular scenarios for the rate of return on the market: Market Return Aggressive Stock -4% 38 6% 24 Aggressive stock Defensive stock a. What are the betas of the two stocks? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Beta Aggressive stock Defensive stock Defensive Stock b. What is the expected rate of return on each stock if the two scenarios for the market return are equally likely to be 6% or 24%? (Do not round intermediate calculations. Round your answers to 1 decimal place.) Expected Rate of Return 5% 13 % %arrow_forward

- Consider the following table, which gives a security analyst’s expected return on two stocks and the market index in two scenarios: Scenario Probability Market Return Aggressive Stock Defensive Stock 1 0.5 6% 2.0% 5.0% 2 0.5 20 32 15 Required: a. What are the betas of the two stocks? (Round your answers to 2 decimal places.) b. What is the expected rate of return on each stock?arrow_forwardConsider the following table, which gives a security analyst's expected return on two stocks and the market index in two scenarios: Aggressive Scenario 1 Probability Market Return 0.5 2 0.5 7% 20 Stock 3.2% Defensive Stock 5.0% 31 14 Required: a. What are the betas of the two stocks? (Round your answers to 2 decimal places.) Beta A Beta D 2.14 0.69 b. What is the expected rate of return on each stock? (Round your answers to 2 decimal places.) Rate of return on A Rate of return on D 17.10 % 9.50% c. If the T-bill rate is 7%, what are the alphas of the two stocks? (Negative values should be indicated by a minus sign. Do not round intermediate calculations. Round your answers to 2 decimal places.)arrow_forwardConsider the following table, which gives a security analyst's expected return on two stocks in two particular scenarios for the rate of return on the market: Market Return 7% 23 Aggressive Stock -4% 37 Defensive Stock Hurdle rate 4% Required: a. What are the betas of the two stocks? 11 b. What is the expected rate of return on each stock if the two scenarios for the market return are equally likely? e. What hurdle rate should be used by the management of the aggressive firm for a project with the risk characteristics of the defensive firm's stock if market return is equally likely to be 7% or 23% ? Also, assume a T-Bill rate of 4%. Complete this question by entering your answers in the tabs below. Required A Required B What hurdle rate should be used by the management of the aggressive firm for a project with the risk characteristics of the defensive firm's stock if market return is equally likely to be 7% or 23% ? Also, assume a T-Bill rate of 4%. Note: Do not round intermediate…arrow_forward

- Consider the following data for two risk factors (1 and 2) and two securities (J and L):λ0 = 0.07 λ1 = 0.04 λ2 = 0.06bJ1 = 0.10 bJ2 = 1.60 bL1 = 1.80 bL2 = 2.45a. Compute the expected returns for both securities. b. Suppose that Security J is currently priced at $50 while the price of Security L is $15.00.Further, it is expected that both securities will pay a dividend of $0.95 during the coming year.What is the expected price of each security one year from now? c. Compute the correlation between stock A and stock B considering the following data.Standard deviation of stock A = 10 percentStandard deviation of stock B = 17 percentCovariance between the two stocks = 90.arrow_forwardConsider the following two scenarios for the economy and the expected returns in each scenario for the market portfolio, and aggressive stock A, and a defensive stock D. A. Find the beta of each stock B. If each scenario is equally likely, find the expected rate of return on the market portfolio and on each stock. C. If the T-bill rate is 4%, what does the CAPM say about the fair expected rate of return on the two stocks? D. Which stock seems to be a better buy on the basis of your answers to (a) through (c).arrow_forwardConsider the following table, which gives a security analyst's expected return on two stocks for two particular market returns: Market return Aggressive Stock Defensive Stock 7% 4% 2.5% 25 38 16 What are the betas of the two stocks?arrow_forward

- Consider the following table, which gives a security analyst’s expected return on two stocks and the market index in two scenarios: Scenario Probability Market Return Aggressive Stock Defensive Stock 1 0.5 6% 2.0% 5.0% 2 0.5 20 32 15 Required: a. What are the betas of the two stocks? (Round your answers to 2 decimal places.) Beta A : Beta D: b. What is the expected rate of return on each stock? (Round your answers to 2 decimal places.) % Rate of Return on A: % Rate of Return on B:arrow_forwardGiven that the formula for CAPM is Expected return= risk free rate + Beta*(Return on market - risk free rate), Security A has a beta of 1.16 and an expected return of .1137 and Security B has a beta of .92 and expected return of .0984. If these securities are assumed to be correctly priced, what is their risk free rate? Based on CAPM, what is the return on the market?arrow_forwardAssume that using the Security Market Line (SML) the required rate of return (RA) on stock A is found to be half of the required return (RB) on stock B. The risk-free rate (Rf) is one-fourth of the required return on A. Return on market portfolio is denoted by RM. Find the ratio of beta of A (bA) to beta of B (bB). (please show all workings)arrow_forward

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning