Subpart (a):

The equilibrium price and the quantity of haircuts and total surplus.

Subpart (a):

Explanation of Solution

Demand curve: The demand equation is

Supply curve: The supply equation is

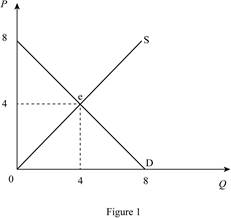

In Figure 1, horizontal axis measures quantity and vertical axis measures price. The curve D indicates demand and the curve S indicates supply. Market reaches the equilibrium at point ‘e’ where the demand curve intersects with supply curve.

Equilibrium price can be calculated as follows.

Equilibrium price is $4.

Equilibrium quantity can be calculated by substituting the equilibrium price in to supply equation.

Thus, equilibrium quantity is 4 units.

Consumer surplus is $8.

Producer surplus is $8.

Total surplus can be calculated as follows.

Total surplus is $16.

Concept introduction:

Consumer surplus: It is the difference between the highest willing price of the consumer and the actual price that the consumer pays.

Producer surplus: It is the difference between the minimum accepted price for the producer and the actual price received by the producer.

Equilibrium price: It is the market price determined by equating the supply to the demand. At this equilibrium point, the supply will be equal to the demand and there will be no excess demand or

Subpart (b):

The equilibrium price and the quantity of haircuts and total surplus.

Subpart (b):

Explanation of Solution

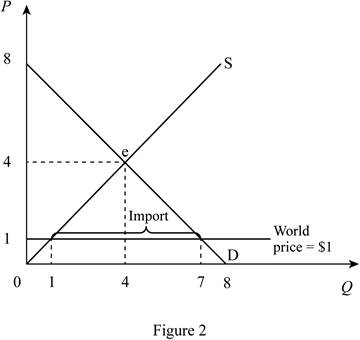

The world price for the good is $1. Thus, when the country opens the market for trade, the price becomes $1 in domestic country too. Figure 2 describe this situation.

In Figure 2, horizontal axis measures quantity and vertical axis measures price. The curve D indicates demand and the curve S indicates supply. Market reaches the equilibrium at point ‘e’ where the demand curve intersects with supply curve.

When the competitor (Rest of the world) sells a good at price $1, in domestic country equilibrium price become equal to world price. Thus, equilibrium price in the domestic country is $1.

Equilibrium domestic supply can be calculated by substituting the domestic equilibrium price in to supply equation.

Thus, equilibrium quantity is 1 unit.

Equilibrium domestic demand can be calculated by substituting the domestic equilibrium price in to demand equation.

Thus, equilibrium domestic demand is 7 units.

Total imports can be calculated as follows.

Domestic imports are 6 units.

Consumer surplus can be calculated as follows.

Consumer surplus is $24.5.

Producer surplus can be calculated as follows.

Producer surplus is $0.5.

Total surplus can be calculated as follows.

Total surplus is $25.

Concept introduction:

Consumer surplus: It is the difference between the highest willing price of the consumer and the actual price that the consumer pays.

Producer surplus: It is the difference between the minimum accepted price for the producer and the actual price received by the producer.

Equilibrium price: It is the market price determined by equating the supply to the demand. At this equilibrium point, the supply will be equal to the demand and there will be no excess demand or excess supply in an economy. Thus, the economy will be at equilibrium.

Subpar (c):

The equilibrium price and the quantity of haircuts and total surplus.

Subpar (c):

Explanation of Solution

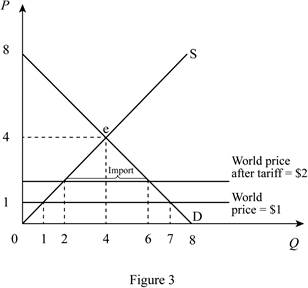

When domestic country impose tariff of $1, the price in domestic country increases from $1 to $2. This increase in price is shown in the Figure 3.

In Figure 3, horizontal axis measures quantity and vertical axis measures price. The curve D indicates demand and the curve S indicates supply. Market reaches the equilibrium at point ‘e’ where the demand curve intersects with supply curve. Price is increases from $1 to $2 due to the tariff of $1.

Domestic equilibrium price can be calculated as follows.

New domestic price is $2.

Equilibrium domestic supply can be calculated by substituting the domestic equilibrium price in to supply equation.

Thus, equilibrium quantity is 2 units.

Equilibrium domestic demand can be calculated by substituting the domestic equilibrium price in to demand equation.

Thus, equilibrium domestic demand is 6 units.

Total imports can be calculated as follows.

Domestic imports are 4 units.

Consumer surplus can be calculated as follows.

Consumer surplus is $18.

Producer surplus can be calculated as follows.

Producer surplus is $2.

Government revenue can be calculated as follows.

Government revenue is 4.

Total surplus can be calculated as follows.

Total surplus is $24.

Concept introduction:

Consumer surplus: It is the difference between the highest willing price of the consumer and the actual price that the consumer pays.

Producer surplus: It is the difference between the minimum accepted price for the producer and the actual price received by the producer.

Equilibrium price: It is the market price determined by equating the supply to the demand. At this equilibrium point, the supply will be equal to the demand and there will be no excess demand or excess supply in an economy. Thus, the economy will be at equilibrium.

Subpart (d):

Calculate total gains and deadweight loss .

Subpart (d):

Explanation of Solution

Total gains from opening up trade can be calculated as follows.

Total gains are$8.

Deadweight loss can be calculated as follows.

Deadweight loss is $1.

Want to see more full solutions like this?

Chapter 9 Solutions

Principles of Microeconomics

- For the statement below, argue in position for both in favor or opposed to the statement. Incompetent leaders can't be ethical leaders. Traditional leadership theories and moral standards are not adequate to help employees solve complex organizational issues.arrow_forwardpresentation on "Dandelion Insomnia." Poemarrow_forwardDon't used Ai solutionarrow_forward

- "Whether the regulator sells or gives away tradeable emission permits free of charge, the quantities of emissions produced by firms are the same." Assume that there are n identical profit-maximising firms where profit for each firm is given by π(e) with л'(e) > 0; π"(e) < 0 and e denotes emissions. Individual emissions summed over all firms gives E which generates environmental damages D(E). Show that the regulator achieves the optimal level of total pollution through a tradeable emission permit scheme, where the permits are distributed according to the following cases: Case (i) the firm purchases all permits; Case (ii) the firm receives all permits free; and Page 3 of 5 ES30031 Case (iii) the firm purchases a portion of its permits and receives the remainder free of charge.arrow_forwardcompare and/or contrast the two plays we've been reading, Antigone and A Doll's House.arrow_forwardPlease answer step by steparrow_forward

- Suppose there are two firms 1 and 2, whose abatement costs are given by c₁ (e₁) and C2 (е2), where e denotes emissions and subscripts denote the firm. We assume that c{(e) 0 for i = 1,2 and for any level of emission e we have c₁'(e) # c₂' (e). Furthermore, assume the two firms make different contributions towards pollution concentration in a nearby river captured by the transfer coefficients ε₁ and 2 such that for any level of emission e we have C₂'(e) # The regulator does not know the resulting C₁'(e) Τι environmental damages. Using an analytical approach explain carefully how the regulator may limit the concentration of pollution using (i) a Pigouvian tax scheme and (ii) uniform emissions standards. Discuss the cost-effectiveness of both approaches to control pollution.arrow_forwardBill’s father read that each year a car’s value declines by 10%. He also read that a new car’s value declines by 12% as it is driven off the dealer’s lot. Maintenance costs and the costs of “car problems” are only $200 per year during the 2-year warranty period. Then they jump to $750 per year, with an annual increase of $500 per year.Bill’s dad wants to keep his annual cost of car ownership low. The car he prefers cost $30,000 new, and he uses an interest rate of 8%. For this car, the new vehicle warranty is transferrable.(a) If he buys the car new, what is the minimum cost life? What is the minimum EUAC?(b) If he buys the car after it is 2 years old, what is the minimum cost life? What is the minimum EUAC?(c) If he buys the car after it is 4 years old, what is the minimum cost life? What is the minimum EUAC?(d) If he buys the car after it is 6 years old, what is the minimum cost life? What is the minimum EUAC?(e) What strategy do you recommend? Why? Please show each step and formula,…arrow_forwardO’Leary Engineering Corp. has been depreciating a $50,000 machine for the last 3 years. The asset was just sold for 60% of its first cost. What is the size of the recaptured depreciation or loss at disposal using the following depreciation methods?(a) Straight-line with N = 8 and S = 2000(b) Double declining balance with N = 8(c) 40% bonus depreciation with the balance using 7-year MACRS Please show every step and formula, don't use excel. The answer should be (a) $2000 loss, (b) $8000 deo recap, (c) $14257 dep recap, thank you.arrow_forward

- The cost of garbage pickup in Green Gulch is $4,500,000 for Year 1. The population is increasing at 6%, the nominal cost per ton is increasing at 5%, and the general inflation rate is estimated at 4%.(a) Estimate the cost in Year 4 in Year-1 dollars and in nominal dollars.(b) Reference a data source for trends in volume of garbage per person. How does including this change your answer? Please show every step and formula, don't use excel. The answer should be $6.20M, $5.2M, thank you.arrow_forwardPlease show each step with formulas, don't use Excel. The answer should be 4 years, $16,861.arrow_forwardAssume general inflation is 2.5% per year. What is the price tag in 8 years for an item that has an inflation rate of 4.5% that costs $700 today? Please show every step and formula, don't use excel. The answer should be $1203, thank you.arrow_forward

Principles of MicroeconomicsEconomicsISBN:9781305156050Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of MicroeconomicsEconomicsISBN:9781305156050Author:N. Gregory MankiwPublisher:Cengage Learning Principles of Economics, 7th Edition (MindTap Cou...EconomicsISBN:9781285165875Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics, 7th Edition (MindTap Cou...EconomicsISBN:9781285165875Author:N. Gregory MankiwPublisher:Cengage Learning Principles of Macroeconomics (MindTap Course List)EconomicsISBN:9781285165912Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Macroeconomics (MindTap Course List)EconomicsISBN:9781285165912Author:N. Gregory MankiwPublisher:Cengage Learning Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Microeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506893Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Macroeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506756Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Macroeconomics: Private and Public Choice (MindTa...EconomicsISBN:9781305506756Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning

Economics: Private and Public Choice (MindTap Cou...EconomicsISBN:9781305506725Author:James D. Gwartney, Richard L. Stroup, Russell S. Sobel, David A. MacphersonPublisher:Cengage Learning