Videos

Multiple Products. Materials, and Processes

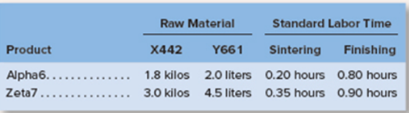

Mickley Corporation produces two products. Alpha’s and Zeta’s, which pass through two operations. Sintering and

Finishing. Each of the products uses two raw materials−X442 and Y661. The company uses a

Information relating to materials purchased and materials used in production during May follows:

The following additional information is available:

a. The company recognizes price variances when materials are purchased.

b. The standard labor rate is $19.80 per hour in Sintering and $19.20 per hour in Finishing.

c. During May, 1,200 direct labor-hours were worked in Sintering at a total labor cost of $27,000, and 2,850 direct labor-hours were worked in Finishing at a total labor cost of $59.850.

d. Production during May was 1,500 Alpha6s and 2.000 Zeta7s.

Required:

1. Prepare a standard cost card for each product, showing the standard cost of direct materials and direct labor.

2. Compute the materials price and quantity variances for each material.

3. Compute the labor rate and efficiency variances for each operation.

.

1

Standard cost card

A standard cost card contains all the information regarding standard quantities, rates, hours etc. It shows total cost of producing one unit.

To prepare: Standard cost card for both the given products, showing cost of direct materials and labor.

Answer to Problem 21P

Total standard cost of alpha6s is determined as $28.42 and of zeta7s is $41.01.

Explanation of Solution

Standard cost card of Alpha6s:

| Particulars | Standard Quantity or standard hours | Standard price or standard rate | Standard cost (in $) | ||

| Direct material (X442) | 1.8 | Kilos | $3.5 | Per kilo | 6.3 |

| Direct material (Y661) | 2.0 | Liters | $1.4 | Per liter | 2.8 |

| Direct labor (Sintering) | 0.2 | Hours | $19.8 | Per hour | 3.96 |

| Direct labor (Finishing) | 0.8 | Hours | $19.2 | Per hour | 15.36 |

| Total | 28.42 | ||||

Standard cost card of zeta7s:

| Particulars | Standard Quantity or standard hours | Standard price or standard rate | Standard cost (in $) | ||

| Direct material (X442) | 3.0 | Kilos | $3.5 | Per kilo | 10.5 |

| Direct material (Y661) | 4.5 | Liters | $1.4 | Per liter | 6.3 |

| Direct labor (Sintering) | 0.35 | Hours | $19.8 | Per hour | 6.93 |

| Direct labor (Finishing) | 0.9 | Hours | $19.2 | Per hour | 17.28 |

| Total | 41.01 | ||||

So, total standard cost of Alpha6s is $28.42 and of zeta7s is $41.01.

2

Variances

A variance shows difference between actual amount of cost incurred and the budgeted cost. Variances can either be favorable or unfavorable.

To calculate: Amount of material price variance and quantity variance.

Answer to Problem 21P

Material price variance for material X442 is $1,450 unfavorable and for material Y661 is $775 favorable.

material quantity variance for material X442 is $700 favorable and for material Y661 is $1,400 unfavorable.

Explanation of Solution

Formula to calculate material price variance is:

For material X442, actual price will be:

Standard price is given as $3.5 per kilo and actual quantity purchased is 14,500. So, material price variance will be:

For material Y661, actual price will be:

Standard price is given as $1.4 per liter and actual quantity purchased is 15,500. So, material price will be:

Formula to calculate material quantity variance is:

For material X442, actual quantity is given as 8,500 kilos and standard price is $3.5 per kilo. Standard quantity will be calculated as:

So, Material quantity variance will be:

For material Y661, actual quantity is given as 13,000 liters and standard price is $1.4 per liter. Standard quantity will be calculated as:

So, material quantity variance will be:

3

Variances

Variances related to labor show difference among actual cost incurred on labor and the standard cost. Variances are considered favorable when standard cost is more than that of actual cost.

Amount of labor rate and efficiency variances.

Answer to Problem 21P

Labor rate variance for sintering is $3,240 unfavorable and for finishing is $5,130 unfavorable.

Labor efficiency variance for sintering is $3,960 unfavorable and for finishing is $2,880 favorable.

Explanation of Solution

Formula to calculate labor rate variance is:

For sintering, standard rate is $19.80 per hour, actual hours worked are 1,200 and actual rate will be $22.5 per hour ($27,000/1,200). Labor rate variance will be:

For finishing, standard rate is $19.20 per hour, actual hours worked are 2,850 and actual rate will be $21 per hour ($59,850/2,850). So, labor rate variance will be:

Formula to calculate labor efficiency variance is:

For sintering, actual hours are 1,200, standard rate is $19.8 and standard hours will be 1,000 ((0.2*1,500)+(0.35*2,000)). So, the labor efficiency variance will be:

For finishing, actual hours are 2,850, standard rate is $19.2 and standard hours will be 3,000 ((0.8*1,500 + 0.9*2,000))

Want to see more full solutions like this?

Chapter 9 Solutions

Loose Leaf For Introduction To Managerial Accounting

- Chrzan, Incorporated, manufactures and sells two products: Product EO and Product NO. Data concerning the expected production of each product and the expected total direct labor-hours (DLHs) required to produce that output appear below: Product E0 Product Ne Total direct labor-hours Activity Cost Pools Labor-related Production orders Order size The company is considering adopting an activity-based costing system with the following activity cost pools, activity measures, and expected activity: Estimated Overhead Cost Multiple Choice $33.94 per MH $54.20 per MH Direct Expected Labor-Hours Production Per Unit 10.1 410 1,550 9.1 $51.98 per MH $21.40 per MH Activity Measures DLHS orders MHs Total Direct Labor- Hours $ 301,890 61,087 585,366 $948,343 The activity rate for the Order Size activity cost pool under activity-based costing is closest to: 4,141 14, 105 18,246 Product E 4,141 850 5,550 Expected Activity Product NO 14, 105 950 5,250 Total 18,246 1,800 10,800arrow_forwardHarrison Company makes two products and uses a traditional costing system in which a single plantwide predetermined overhead rate is computed based on direct labor-hours. Data for the two products for the upcoming year follow: Direct materials cost per unit Direct labor cost per unit Direct labor-hours per unit Number of units produced Rascon $14.00 $ 2.60 0.20 19,000 These products are customized to some degree for specific customers. Required: 1. The company's manufacturing overhead costs for the year are expected to be $376,250. Using the company's traditional costing system, compute the unit product costs for the two products. 2. Management is considering an activity-based absorption costing system in which half of the overhead would continue to be allocated based on direct labor-hours and half would be allocated based on engineering design time. This time is expected to be distributed as follows during the upcoming year: Rascon Parcel 4,700 4,700 Engineering design time (in hours)…arrow_forwardRequired information [The following information applies to the questions displayed below.] Rusties Company recently implemented an activity-based costing system. At the beginning of the year, management made the following estimates of cost and activity in the company's five activity cost pools: Activity Cost Pool Labor-related Purchase orders Product testing Template etching General factory Required: 1. Compute the activity rate for each of the activity cost pools. Activity Cost Pool Labor-related Activity Measure Direct labor-hours Number of orders Number of tests Number of templates Machine-hours Purchase orders Product testing Template etching General factory Activity Rate per DLH per order per test per template per MH < Prev Expected Overhead Cost $ 18,000 $ 1,050 $ 3,500 $ 700 $ 50,000 5 of 5 Expected Activity 2,000 DLHS 525 orders 350 tests 28 templates 10,000 MHS ww Nextarrow_forward

- The controller of PUSO Co. estimates the amount of materials handling overhead cost that should be allocated to the firm's two product using the data below: Specialty Windows 7,000 Wall Mirrors Total expected units produced Total expected materials move Expected direct labor per unit 8,000 900 300 7 5 The total materials handling cost for the year is expected to be P38, 448. If the materials handling cost is allocated on the basis of direct labor-hours, how much of the total material handling cost should be allocated to the specialty windows?arrow_forwardSuki Company uses activity-based costing to compute product costs for external reports. The company has three activity cost pools and applies overhead using predetermined overhead rates for each activity cost pool. Estimated costs and activities for the current year are presented below for the three activity cost pools: Estimated Overhead Cost Activity 1 Activity 2 Activity 3 Actual activity for the current year was as follows: Actual Activity Activity 1 Activity 2 Activity 3 $34,300 $20,520 $36,112 O a. $30,026.50 O b. $36,112.00 OC. $36,107.00 O d. $35,773.45 1,415 1,805 1,585 0 Expected Activity 1,400 1,800 1,600 The amount of overhead applied for Activity 3 during the year was closest to: Øarrow_forwardHarrison Company makes two products and uses a traditional costing system in which a single plantwide predetermined overhead rate is computed based on direct labor-hours. Data for the two products for the upcoming year follow: Direct materials cost per unit Direct labor cost per unit Direct labor-hours per unit Number of units produced. Rascon. $ 11.00 $ 2.80 0.50 10,000 These products are customized to some degree for specific customers. Required: 1. The company's manufacturing overhead costs for the year are expected to be $606,100. Using the company's traditional costing system, compute the unit product costs for the two products. 2. Management is considering an activity-based absorption costing system in which half of the overhead would continue to be allocated based on direct labor-hours and half would be allocated based on engineering design time. This time is expected to be distributed as follows during the upcoming year: Parcel Engineering design time (in hours) 4,500 Compute…arrow_forward

- The controller of Hendershot Corporation estimates the amount of materials handling overhead cost that should be allocated to the company's two products using the data that are given below: Wall Specialty Mirrors Windows Total expected units produced Total expected material moves Expected direct labor-hours per unit 11,900 1,710 1,190 1,610 8 The total materials handling cost for the year is expected to be $17,148.7O. If the materials handling cost is allocated on the basis of material moves, the total materials handling cost allocated to the specialty windows is closest to: (Round your intermediate calculations to 4 decimal places.)arrow_forwardCherokee Inc. is a merchandiser that provided the following information: Amount 20,000 $ Number of units sold Selling price per Variable selling expense per Variable administrative expense per unit Total fixed selling expense Total fixed administrative expense unit 30 unit $ 4 $ 2 $ 40,000 $ 30,000 $ Beginning merchandise inventory Ending merchandise inventory Merchandise purchases 24,000 $ 44,000 $ 180,000 Required: 1. Prepare a traditional income statement. 2. Prepare a contribution format income statement.arrow_forwardDraus Products Company uses activity-based costing to compute product costs for external reports. The company has three activity cost pools and applies overhead using predetermined overhead rates for each activity cost pool. Estimated costs and activities for the current year are presented below for the three activity cost pools. estimated overhead expected activity activity#1 $60,048 4800 activity#2 $58,656 2400 activity#3 $130,324 4400 Actual costs and activities for the current year were as follows. actual overhead cost actual activity acrivity#1 $59,798 4830 activity#2 $58,476 2370 activity#3 $130,234 4450 The total amount of overhead applied during the year was closest to: 1. $248,508 2. $248,988 3. $250,155 4. $251,334arrow_forward

- CanCo Company manufactures a single product. The company keeps careful records of manufacturing activities, from which the following Information has been extracted: Number of units produced Cost of goods manufactured Work-in-process inventory, beginning Work-in-process inventory, ending Direct materials cost per unit Direct labour cost per unit Manufacturing overhead cost, total Manufacturing overhead cost Y= Level of Activity March The company's manufacturing overhead cost consists of both variable and fixed cost elements. To have data available for planning, management wants to determine how much of the overhead cost is variable with units produced and how much of it is fixed per month. $ 5,200 $260,800 31,000 53,000 Required: 1. For both March and June, determine the amount of manufacturing overhead cost added to production. (Hint: A useful way to proceed might be to construct a schedule of cost of goods manufactured.) Cost of goods manufactured Answer is complete but not entirely…arrow_forwardA Corporation manufactures two products: Product K and Product L. The company uses a plantwide overhead rate based on direct labor-hours. It is considering implementing an activity-based costing (ABC) system that allocates its manufacturing overhead to four cost pools. The following additional information is available for the company as a whole and for Products K and L. Activity Cost Pool Activity Measure Machining Machine setups Total Cost Total Activity S 247,00013,000MHS 150setups 2products Direct labor-hours $ 260,00010,000DLHS Machine-hours Number of setups S 60,000 Number of products S 56,000 Product design Order size Activity Measure Machine-hours Number of setups Number of products Direct labor-hours Product K Product L 10,000 110 3,000 40 6,000 4,000 Required: 1. Compute the plantwide (POHR) overhead rate. 2. Using the plantwide overhead rate, how much manufacturing overhead cost would be allocated to Product K? How much is allocated to Product L? 3. Using the ABC system,…arrow_forwardPasternik Company produces and sells two products, Alpha and Zeta. The following information is available relating to its setup activities: Alpha Units produced Batch size (units) Total direct labor hours Cost per setup A) 이이이이티 B) With a volume-based costing system that applies overhead based on direct labor hours, the setup cost portion of overhead for each unit is (rounded to the nearest cent): C) D) 270 10 E) 1,100 $2,180 Alpha Zeta $3.43 $13.96 $4.43 $14.96 $9.19 22,130 540 43,120 $2,260 Zeta $3.43 $6.68 $4.43 $7.68 $5.55arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning