Concept explainers

Videos

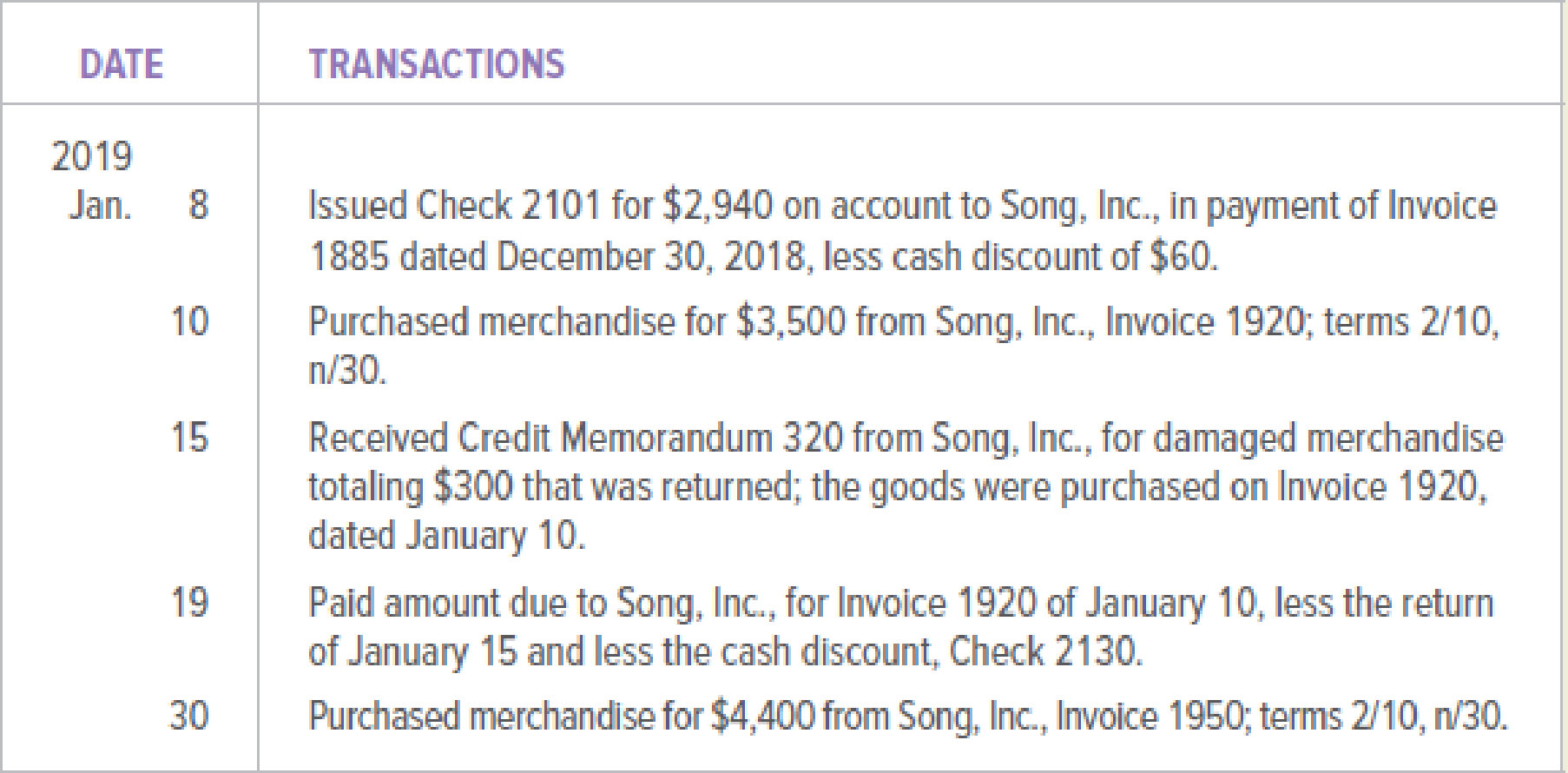

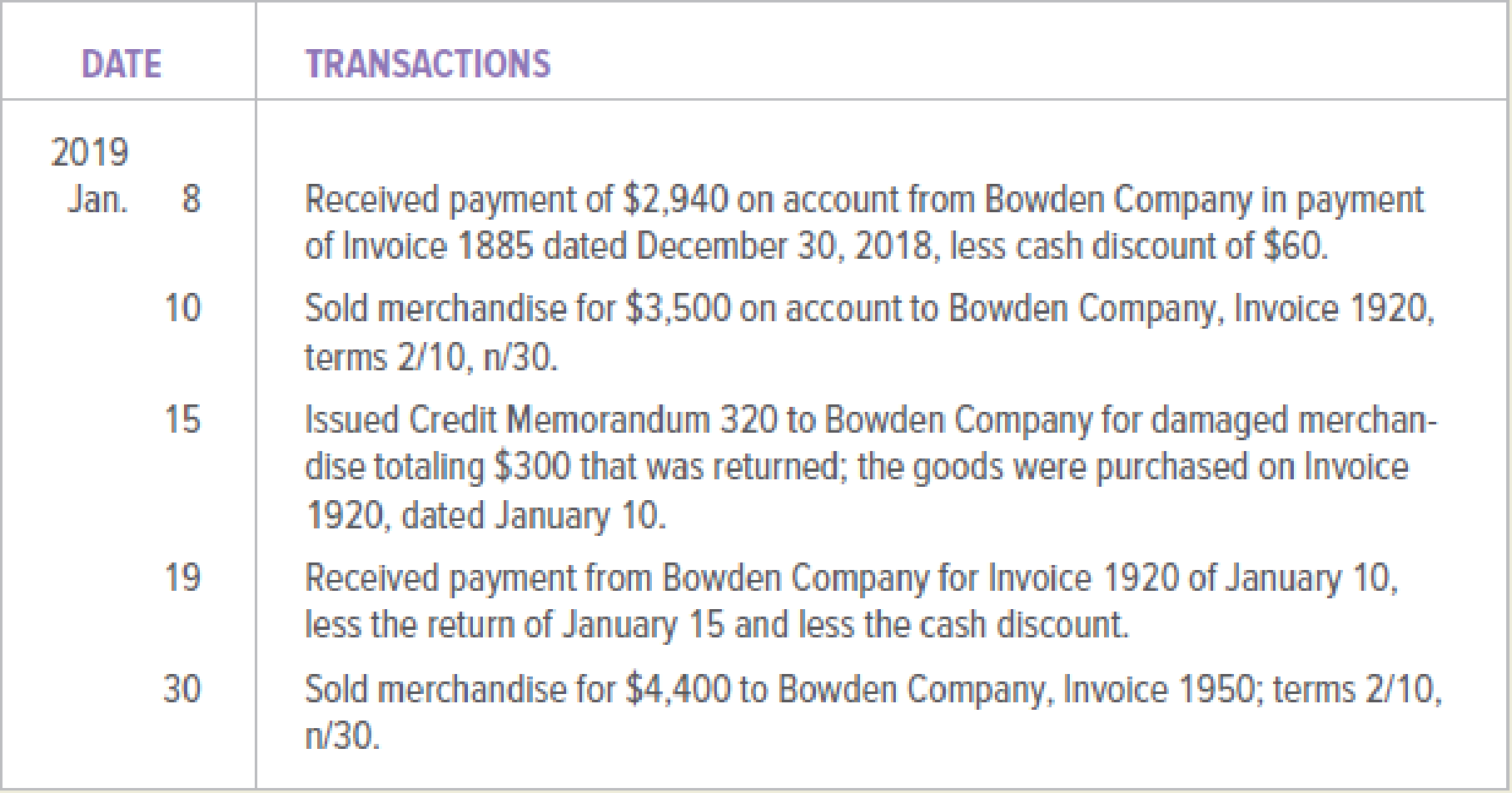

Bowden Company (buyer) and Song, Inc. (seller), engaged in the following transactions during January 2019:

Bowden Company

Song, Inc.

INSTRUCTIONS

- 1. Open the accounts payable ledger account and accounts receivable ledger account indicated below for both Bowden Company and Song, Inc. Enter the balances as of January 1, 2019.

- 2. Journalize the transactions above in a general journal for both Bowden Company and Song, Inc. Begin the journals for both companies with page 21.

- 3.

Post the transactions to the appropriate accounts in the general ledger and the accounts payable subsidiary ledger for Bowden Company. - 4. Post the transactions to the appropriate accounts in the general ledger and the accounts receivable subsidiary ledger for Song, Inc.

GENERAL LEDGER ACCOUNTS—BOWDEN COMPANY

201 Accounts Payable, $3,000 Cr.

ACCOUNTS PAYABLE LEDGER ACCOUNT—BOWDEN COMPANY

Song, Inc., $3,000

GENERAL LEDGER ACCOUNTS—SONG, INC.

111 Accounts Receivable, $3,000 Dr.

ACCOUNTS RECEIVABLE LEDGER ACCOUNT—SONG, INC.

Bowden Company, $3,000

Analyze: What is the balance of the accounts payable for Song, Inc., in the Bowden Company accounts payable subsidiary ledger? What is the balance of the accounts receivable for Bowden Company in the Song, Inc., accounts receivable subsidiary ledger?

1.

Create the accounts payable ledger account and accounts receivable ledger account of company B and company SI indicating the balances on given date.

Explanation of Solution

Ledgers:

Ledgers are T accounts to which journal entries are posted. Ledgers are used to ascertain transactions of a particular account and its closing balance for the period. The day-to-day transactions of the business are recorded in their respective ledgers.

The accounts payable ledger account of company B is as follows:

| Accounts Payable | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | 3,000 | ||

Table (1)

The accounts receivable ledger account of company SI is as follows:

| Accounts Receivable | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | 3,000 | ||

Table (2)

2.

Record the entries into the general journal of the company B and the company SI.

Explanation of Solution

The recording of entries in the general journal for company B is as follows:

Recording the payment made:

| GENERAL JOURNAL | Page 21 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 8, 2019 | Accounts payable/Company SI | 3,000 | ||

| Purchases discounts | 60 | |||

| Cash | 2,940 | |||

| (to record the payment made and receiving purchases discount) | ||||

Table (3)

- • The accounts payable account is liability and the account balance is decreasing. Therefore, accounts payable account is debited.

- • The purchases discount account is a contra expense account. The account has the normal credit balance and it is increasing. Therefore, it is credited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the purchases on credit:

| GENERAL JOURNAL | Page 21 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 10, 2019 | Purchases | 3,500 | ||

| Accounts payable/Company SI | 3,500 | |||

| (to record the inventory purchased on account with terms2/10, n/30) | ||||

Table (4)

- • The purchases account is an expense account. The purchases account has normal debit balance and the balance is increasing. Therefore, it is debited.

- • Accounts payable is liability and the account balance is increasing. Therefore, it is credited.

Recording the purchases returned and credit memorandum received:

| GENERAL JOURNAL | Page 21 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 15, 2019 | Accounts payable/Company SI | 300 | ||

| Purchases returns and allowances | 300 | |||

| (to record the inventory returned and credit memorandum received) | ||||

Table (5)

- • The accounts payable account is a liability account. The accounts payable account has the normal credit balance and it is decreasing. Therefore, it is debited.

- • The purchase returns and allowances account is contra expenses account. The account has the normal credit balance and it is increasing. Therefore, it is credited.

Recording the payment made:

| GENERAL JOURNAL | Page 21 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 19, 2019 | Accounts payable/Company SI | 3,200 | ||

| Purchases discounts | 64 | |||

| Cash | 3,136 | |||

| (to record the payment made and receiving purchases discount) | ||||

Table (6)

- • The accounts payable account is liability and the account balance is decreasing. Therefore, accounts payable account is debited.

- • The purchases discount account is a contra expense account. The account has the normal credit balance and it is increasing. Therefore, it is credited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the purchases on credit:

| GENERAL JOURNAL | Page 21 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 30, 2019 | Purchases | 4,400 | ||

| Accounts payable/Company SI | 4,400 | |||

| (to record the inventory purchased on account with terms2/10, n/30) | ||||

Table (7)

- • The purchases account is an expense account. The purchases account has normal debit balance and the balance is increasing. Therefore, it is debited.

- • Accounts payable is liability and the account balance is increasing. Therefore, it is credited.

The recording of entries in the general journal for company SI is as follows:

Recording the payment received from the buyer:

| GENERAL JOURNAL | Page 21 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 8, 2019 | Sales Discount | 60 | ||

| Cash | 2,940 | |||

| Accounts Receivable/Company B | 3,000 | |||

| (to record the payment received and discount provided) | ||||

Table (8)

- • The sales discount account is identified as contra revenue account and it has normal debit balance which is increasing. Therefore, it is debited.

- • The cash account is asset account and the account balance is increasing. Therefore, cash account is debited. The amount in cash account would be calculated by subtracting the merchandise returned by the buyer and the sales discount provided.

- • The accounts receivable account is asset account and the account balance is decreasing. Therefore, it is credited.

Recording of the merchandise sold:

| GENERAL JOURNAL | Page 21 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 10, 2019 | Accounts Receivable/ Company B | 3,500 | ||

| Sales | 3,500 | |||

| (to record the merchandise sold on credit on terms of 2/10, n/30) | ||||

Table (9)

- • The accounts receivables account is an asset account and the account balance is increasing. Hence, accounts receivable is debited.

- • The sales account is identified as the revenue account and the revenue is generated. Hence, sales account is credited.

Recording the returned merchandise sold and the credit memorandum:

| GENERAL JOURNAL | Page 21 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 15, 2019 | Sales returns and allowances | 300 | ||

| Accounts Receivable/ Company B | 300 | |||

| (to record the merchandise returned and issued credit memorandum) | ||||

Table (10)

- • The sales returns and allowances account is identified as contra revenue account with normal debit balance and it is increasing. Therefore, it is debited.

- • The account receivable account is an asset account and the account balance is decreasing. Therefore, the accounts receivable account is credited.

Recording the payment received from the buyer:

| GENERAL JOURNAL | Page 21 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 19, 2019 | Sales Discount | 64 | ||

| Cash | 3,136 | |||

| Accounts Receivable/Company B | 3,200 | |||

| (to record the timely payment received from the account receivable) | ||||

Table (11)

- • The sales discount account is identified as contra revenue account and it has normal debit balance which is increasing. Therefore, it is debited.

- • The cash account is debited. This is because the cash account is asset account and the account balance is increasing. The amount in cash account would be calculated by subtracting the merchandise returned by the buyer and the sales discount provided.

- • The accounts receivable account is asset account and the account balance is decreasing. Therefore, it is credited.

Recording of the merchandise sold and sales tax payable:

| GENERAL JOURNAL | Page 21 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 30, 2019 | Accounts Receivable/ Company B | 4,400 | ||

| Sales | 4,400 | |||

| (to record the merchandise sold on credit on terms of 2/10, n/30) | ||||

Table (12)

- • The accounts receivables account is an asset account and the account balance is increasing. Therefore, accounts receivables account is debited.

- • The sales account is identified as the revenue account and the revenue is generated. Hence, sales account is credited.

Working Note:

Calculation of purchases discount:

The purchases discounts are received by the buyer for fulfilling the terms of timely payment to seller for purchases. The terms related to paying on timely basis with the company SI was agreed as 2/10, n/30. The terms 2/10, n/30 means the buyer is entitled to receive two percent of purchase discount on the purchases amount. The buyer will be entitled to the discount only if the payment is paid within ten days after provided invoice.

The amount calculated as purchase discount would be $64.

Calculation for sales discount:

The sales discount is provided to the customer by the seller fulfilling the terms of making the timely payments as per 2/10, n/30 terms. The customer is entitled to receive the one percent of sales discount on the merchandise sold if the payment is made with ten days of invoice provided.

The amount calculated as per given information would be $64.

3.

Record the transactions to the appropriate accounts in the general ledger and the accounts payable subsidiary ledger for company B.

Explanation of Solution

The posting of general journal in the appropriate accounts in the general ledger and the accounts payable subsidiary ledger is as follows:

| Cash | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | - | ||

| January 8, 2019 | 2,940 | (2,940) | ||

| January 19, 2019 | 3,136 | (6,076) | ||

Table (13)

| Accounts Payable/Company SI | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | 3,000 | ||

| January 8, 2019 | 3,000 | - | ||

| January 10, 2019 | 3,500 | 3,500 | ||

| January 15, 2019 | 300 | 3,200 | ||

| January 19, 2019 | 3,200 | - | ||

| January 30, 2019 | 4,400 | 4,400 | ||

Table (14)

| Accounts Payable | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | 3,000 | ||

| January 8, 2019 | 3,000 | - | ||

| January 10, 2019 | 3,500 | 3,500 | ||

| January 15, 2019 | 300 | 3,200 | ||

| January 19, 2019 | 3,200 | - | ||

| January 30, 2019 | 4,400 | 4,400 | ||

Table (15)

| Purchases | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | - | ||

| January 10, 2019 | 3,500 | 3,500 | ||

| January 30, 2019 | 4,400 | 7,900 | ||

Table (16)

| Purchases Returns and Allowances | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | - | ||

| January 15, 2019 | 300 | 300 | ||

Table (17)

| Purchases Discounts | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | - | ||

| January 8, 2019 | 60 | 60 | ||

| January 19, 2019 | 64 | 124 | ||

Table (18)

4.

Record the transactions to the appropriate accounts in the general ledger and the accounts payable subsidiary ledger for company SI.

Explanation of Solution

| Cash | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | - | ||

| January 8, 2019 | 2,940 | 2,940 | ||

| January 19, 2019 | 3,136 | 6,076 | ||

Table (19)

| Accounts Receivable/Company B | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | 3,000 | ||

| January 8, 2019 | 3,000 | - | ||

| January 10, 2019 | 3,500 | 3,500 | ||

| January 15, 2019 | 300 | 3,200 | ||

| January 19, 2019 | 3,200 | - | ||

| January 30, 2019 | 4,400 | 4,400 | ||

Table (20)

| Accounts Receivable | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | 3,000 | ||

| January 8, 2019 | 3,000 | - | ||

| January 10, 2019 | 3,500 | 3,500 | ||

| January 15, 2019 | 300 | 3,200 | ||

| January 19, 2019 | 3,200 | - | ||

| January 30, 2019 | 4,400 | 4,400 | ||

Table (21)

| Sales | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | - | ||

| January 10, 2019 | 3,500 | 3,500 | ||

| January 30, 2019 | 4,400 | 7,900 | ||

Table (22)

| Sales Returns and Allowances | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | - | ||

| January 15, 2019 | 300 | 300 | ||

Table (23)

| Sales Discounts | ||||

| Date | Particular |

Debit ($) |

Credit ($) |

Balance ($) |

| January 1, 2019 | Balance | - | ||

| January 8, 2019 | 60 | 60 | ||

| January 19, 2019 | 64 | 124 | ||

Table (24)

The balance of accounts payable account for company SI in company B’s subsidiary ledger is $4,400 credit balance. The balance of accounts receivable account for company B in company SL’s subsidiary ledger is $4,400 debit balance.

Want to see more full solutions like this?

Chapter 8 Solutions

COLLEGE ACCOUNTING (LL)W/ACCESS>CUSTOM<

- The following selected accounts and their current balances appear in the ledger of Clairemont Co. for the fiscal year ended May 31, 2019: Instructions 1. Prepare a multiple-step income statement. 2. Prepare a statement of owners equity. 3. Prepare a balance sheet, assuming that the current portion of the note payable is 50,000. 4. Briefly explain how multiple-step and single-step income statements differ.arrow_forwardRefer to RE6-8. On April 23, 2020, McKinncy Co. receives a check, from Mangold Corporation for 8,500. Prepare the journal entry for McKinncy to record the collection of the account previously written off.arrow_forwardAnalyzing Accounts Receivable Upham Companys June 30, 2019, balance sheet included the following information: Required: 1. Prepare the journal entries necessary for Upham to record the preceding transactions. 2. Prepare an analysis and schedule that shows the amounts of the accounts receivable, allowance for doubtful accounts, notes receivable, and notes receivable dishonored accounts that will be disclosed on Uphams June 30, 2020, balance sheet.arrow_forward

- Comprehensive Selected transactions of Shadrach Computer Corporation during November and December of 2019 are as follows: Required: Prepare journal entries to record the preceding transactions of Shadrach Computer Corporation for 2019. Include year-end accruals. Round all calculations to the nearest dollar.arrow_forwardOn September 18, 2019, Afton Company purchased $2,475 of supplies on account. In Afton Company’s chart of accounts, the supplies account is No. 15, and the accounts payable account is No. 21.a. Journalize the September 18, 2019, transaction on page 87 of Afton Company’s twocolumn journal. Include an explanation of the entry.b. Prepare a four-column account for Supplies. Enter a debit balance of $840 as of September 1, 2019. Place a check mark (¸) in the Posting Reference column.c. Prepare a four-column account for Accounts Payable. Enter a credit balance of $10,900 as of September 1, 2019. Place a check mark (¸) in the Posting Reference column.d. Post the September 18, 2019, transaction to the accounts.e. Do the rules of debit and credit apply to all companies?arrow_forwardRosalie Couses the gross method to record sales made on credit. On June 10, 2019, it made sales of £100,000 with terms 2/10, n/30 to Finley Farms, Inc. On June 19, 2019, Rosalie received payment for 1/2 the amount due from Finley Farms. Rosalie’s fiscal year end is on June 30, 2019. What amount will be reported in the statement of financial position for the accounts receivable due from Finley Farms, Inc.?arrow_forward

- Use the information in the attachment to prepare journal entries without explanations for the following transactions involving notes payable for Gomez Company, whose fiscal year ends June 30.arrow_forwardBelow are the transactions related to notes receivable activity for Barton Corporation. Record each transaction in the journal provided. Enter the date of the last transaction. 2020 13-Nov Accepted a $40,000, 90-day, 6% note from a customer in exchange for their past due accounts receivable balance 31-Dec Made an entry to accrue the accrued interest earned on the Nov 13 note 2021 11-Feb Received payment for the principal and interest on the note dated November 13 22-Apr Accepted a $20,000, 45-day, 5% note from a customer in exchange for consulting fees provided ??? Received payment for the principal and interest on the note dated April 22…arrow_forwardHuhu Company and Hihi Company engaged in the following transactions during the month of July 2021. On July 16, Huhu Company sold merchandise to Hihi Company for P6,000, terms 2/10, n/30. Shipping costs were P600. Hihi Company received the goods and Huhu Company’s invoice on July 17. On July 24, Hihi Company sent the payment to Huhu, which Huhu received on July 25. Additional Info: Both Huhu and Hihi use the periodic inventory system. The arrangement regarding the shipping costs are as follows: Shipping terms FOB destination, Freight Collect. Hihi paid the shipping costs on July 17 and deducted the P600 from the amount owed to Huhu Company. A copy of freight bill to Huhu Company was provided with the July 24 cash remittance. Hihi remitted P5,280 on July 24. How much is the accounts payable of Hihi before remittances?arrow_forward

- On January 1, 2020, the records of ABC Company showed a debit balance of P650,000 in its Accounts Receivable account. The following summary transactions that occurred during 2020 were also shown under the said account: Debits:Charge sales, P6,300,000Shareholders’ subscriptions, P200,000Deposit on contract, P120,000Claims against common carrier for shipping damages, P100,000IOUs from employees, P10,000Cash advances to affiliates, P150,000Advances to a supplier, P30,000Credits:Collections from customers, P5,300,000Write-off, P35,000Merchandise returns, P45,000Allowances to customers for shipping damages, P25,000Collections on carrier claims, P40,000Collections on subscriptions, P50,000Required:a. Determine the correct amount of accounts receivable.b. Compute the amount to be presented as “trade and other receivables” under current assets.arrow_forwardFrom the following particulars of Al Zahra LLC for the year 2019, a. Accounts receivable on 1st Jan 2019 RO 20000. b. During the year RO 18000 was collected from the Opening Accounts receivables and the remaining was treated as uncollectable. c. Sales during the year was RO 175000 d. Amount collected from current years sales was RO 150000 e. From the year 2019 Al Zahra LLC started to use Allowance Method for writing off the un collectables. f. Allowance to be created @ 10% on closing receivables Prepare a) Account of receivables and b) Allowance for Doubtful debts from the above informationarrow_forwardFrom the following particulars of Al Zahra LLC for the year 2019, a. Accounts receivable on 1st Jan 2019 RO 20000. b. During the year RO 18000 was collected from the Opening Accounts receivables and the remaining was treated as uncollectable. c. Sales during the year was RO 175000 d. Amount collected from current years sales was RO 150000 e. From the year 2019 Al Zahra LLC started to use Allowance Method for writing off the un collectables. f. Allowance to be created @ 10% on closing receivablesarrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

- Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage LearningPrinciples of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage LearningPrinciples of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College