a.

To identify:

Discount:

Discount refers to a situation where price issued for the bond is below the par value of the bond.

Premium:

Premium refers to a situation where price issued for the bond is above the par value of the bond.

Par value of bonds:

Par value of bond also mentioned as the face value of the bond is the original price printed on the bond certificate. A bond is considered to be issued at par when yield to maturity of a bond is equal to coupon rate of the bond.

a.

Explanation of Solution

Yield to maturity is 9%.

Bond A has 7% annual coupon rate.

Bond B has 9% annual coupon rate.

Bond C has 11% annual coupon rate.

Bond A has an annual coupon rate of 7% which is less than the required return of 9%, it means that the bond is being traded at below the par value or at discount.

Bond B has an annual coupon rate of 9% which is equal to the required return of 9%, it means that the bond is being traded at par value.

Bond C has an annual coupon rate of 11% which is more than the required return of 9%, it means that the bond is being traded at above the par value or at a premium.

b.

To compute: Price of bonds.

Bonds:

Bonds are a financial instrument, generally issued to raise debt generally for activities which require a significant amount of funds, with an undertaking to repay the amount with appropriate interest.

b.

Explanation of Solution

Bond A

Given,

The coupon rate is 7% or 0.07.

Par value is $1,000

Yield to maturity is 9%

Number of periods is 12

PVIF is 0.35553

PVIFA is 7.1607

The formula to compute the price of bonds:

Where,

i is the interest rate

n is number of time period

PVIFA is Present Value Interest Factor of

PVIF is Present Value Interest Factor

Substitute $1,000 for the par value of the bond, 0.35553 for PVIF (i,n), $70 for interest to be paid each year and 7.1607 for PVIFA (i,n)

Bond B

Given,

The coupon rate is 9% or 0.09.

Par value is $1,000

Yield to maturity is 9%

Number of periods is 12

PVIF is 0.35553

PVIFA is 7.1607

Since bond B is issued at par, the price of the bond will be its value $1,000.

Bond C

Given,

The coupon rate is 11% or 0.11.

Par value is $1,000

Yield to maturity is 9%

Number of periods is 12

PVIF is 0.35553

PVIFA is 7.1607

The formula to compute the price of bonds:

Where,

i is the interest rate

n is number of time period

PVIFA is Present Value Interest Factor of Annuity

PVIF is Present Value Interest Factor

Substitute $1,000 for the par value of the bond, 0.35553 for PVIF (i,n), $110 for interest to be paid each year and 7.1607 for PVIFA (i,n)

Working Note:

Bond A

Calculation of interest to be paid each year:

Bond B

Calculation of interest to be paid each year:

Bond C

Calculation of interest to be paid each year:

Hence, the price of the bond A, B and C are computed to be $856.78, $1,000 and $1,143.21.

c.

To compute: Current yield.

Current Yield:

Current yield is the anticipated

The formula for current yield:

c.

Explanation of Solution

Bond A

Given,

Annual coupon payment as computed is $70.

Current price as computed is $856.78.

The formula to calculate the current yield of Bond A:

Substitute $70 for annual coupon payment and $856.78 for the current price,

Bond B

Given,

Annual coupon payment as computed is $90.

Current price as computed is $1,000.

The formula to calculate the current yield of Bond B:

Substitute $90 for annual coupon payment and $1,000 for the current price,

Bond C

Given,

Annual coupon payment as computed is $110.

Current price as computed is $1,143.21.

The formula to calculate the current yield of Bond C:

Substitute $110 for annual coupon payment and $1,143.21 for the current price,

Hence, the current yield of Bond A, B and C are computed to be $8.17%, 9.00%, and 9.62%.

d.

To compute: Price of each bond 1 year from now. Expected

Bonds:

Bonds are a financial instrument, generally issued to raise debt generally for activities which require a significant amount of funds, with an undertaking to repay the amount with appropriate interest.

d.

Explanation of Solution

Price of each bond one year from now:

Bond A

Given,

The coupon rate is 7% or 0.07.

Par value is $1,000

Yield to maturity is 9%

Number of periods is 11

PVIF is 0.3875

PVIFA is 6.8052

The formula to compute the price of bonds:

Where,

i is the interest rate

n is number of time period

PVIFA is Present Value Interest Factor of

PVIF is Present Value Interest Factor

Substitute $1,000 for the par value of the bond, 0.3875 for PVIF (i,n), $70 for interest to be paid each year and 6.8052 for PVIFA (i,n)

Bond B

Given,

The coupon rate is 9% or 0.09.

Par value is $1,000

Yield to maturity is 9%

A number of periods is 11.

PVIF is 0.3875

PVIFA is 6.8052

Since bond B is issued at par, the price of the bond will be its value $1,000.

Bond C

Given,

The coupon rate is 11% or 0.11.

Par value is $1,000

Yield to maturity is 9%

Number of periods is 11.

PVIF is 0.3875

PVIFA is 6.8052

The formula to compute the price of bonds:

Where,

i is the interest rate

n is number of time period

PVIFA is Present Value Interest Factor of Annuity

PVIF is Present Value Interest Factor

Substitute $1,000 for the par value of the bond, 0.3875 for PVIF (i,n), $110 for interest to be paid each year and 6.8052 for PVIFA (i,n)

Expected total return for each bond:

Expected total return for each bond is equal to YTM which is 9%.

Expected capital gains yield for each bond:

Bond A

Given,

Expected total return for bond A, B and C is 9%.

The current yield of bond A as computed is 8.17%.

The formula to calculate capital gain yield for Bond A:

Substitute 9% for total return and 8.17% for current yield,

Bond B

Given,

Expected total return for bond A, B and C is 9%.

The current yield of bond A as computed is 9%.

The formula to calculate capital gain yield for Bond B:

Substitute 9% for total return and 9% for current yield,

Bond C

Given,

Expected total return for bond A, B and C is 9%.

The current yield of bond C as computed is 9.62%.

The formula to calculate capital gain yield for Bond A:

Substitute 9% for total return and 9.62% for current yield,

Working Note:

Bond A

Calculation of interest to be paid each year:

Bond B

Calculation of interest to be paid each year:

Bond C

Calculation of interest to be paid each year:

Hence, the price of the bond A, B and C are computed to be $863.86, $1,000 and $1,136.07 respectively. The capital gain yield of Bond A, B and C are computed to be 0.83%, 0% and -0.62% respectively. Expected total return for each bond is computed to be 9%.

e.1.

To compute: Bond’s normal yield to maturity.

e.1.

Explanation of Solution

Bond D

Given,

The semi-annual coupon rate is 8% or 0.08.

Par value is $1,000

Number of periods is 18

Bond price is $1,150.

The formula to compute bond’s nominal yield to maturity:

Where,

C is coupon value

FV is face value

P is the price of the bond

n is number of periods

Substituting $80 for C, $1,000 for FV, $1,150 for P and 18 months for n,

Working note:

Calculation of semiannual rate:

Interest is

Hence, yield to maturity is computed to be 5.88%

2.

To compute: Yield to call

2.

Explanation of Solution

Given,

Semi-annual coupon rate is 8% or 0.08.

Par value is $1,000

Number of periods is 10

The call price is $1,040

The formula to compute bond’s nominal yield to maturity:

Where,

C is coupon value

FV is face value

P is the price of the bond

n is number of periods

Substituting $80 for C, $1,150 for FV, $1,040 for P and 10 months for n,

Hence, yield to maturity is computed to be 5.29.

3.

To identify: Decision to choose between yield to maturity or yield to call.

3.

Answer to Problem 19SP

Mr. C will earn Yield to call in the given case.

Explanation of Solution

Since the bonds are trading at a premium, it indicates that interest rates have fallen.

In case interest rates remain to be constant at present level, Mr. C should anticipate the bond to be called.

As a result, he will earn Yield to call.

Hence, Mr. C will earn Yield to call in the given case.

f.

To identify: Difference between price risk and reinvestment risk. Bonds which have highest reinvestment risk.

f.

Explanation of Solution

Price risk

Price risk is the possibility of the fall in the price of bonds due to rising in the interest rates.

Price risk is higher on bonds having longer maturity period as it gives sufficient time to bondholder to replace the bond.

Reinvestment risk

Reinvestment risk is the possibility of fall in the interest rates which will subsequently result in fall in income from the bond portfolio.

Reinvestment risk is higher on short-term bonds as less high old coupon bonds will be replaced with a new low-coupon bond.

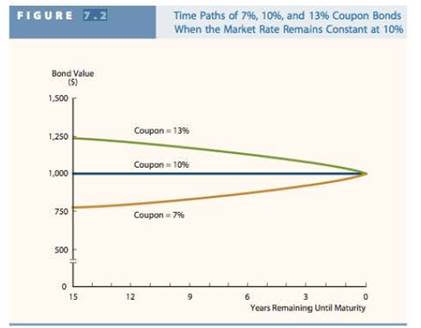

Bonds have been ranked in order from the most interest rate risk to the least interest rate risk:

18 year bond with a 9% annual coupon

A 10-year bond with a zero coupon

A 10-year bond with a 9% annual coupon

A 5-year bond with a zero coupon

A 5-year bond with a 9% annual coupon

Hence, bonds have been ranked above from the most interest rate risk to the least interest rate risk.

g.1.

To compute: Expected interest rate for each bond in each year.

g.1.

Explanation of Solution

Expected interest yield or current yield for each bond in each year:

| N | Bond A | Bond B | Bond C |

| 12 | 8.17% | 9.00% | 9.62% |

| 11 | 8.10% | 9.00% | 9.68% |

| 10 | 8.03% | 9.00% | 9.75% |

| 9 | 7.95% | 9.00% | 9.82% |

| 8 | 7.87% | 9.00% | 9.90% |

| 7 | 7.78% | 9.00% | 9.99% |

| 6 | 7.69% | 9.00% | 10.09% |

| 5 | 7.59% | 9.00% | 10.21% |

| 4 | 7.48% | 9.00% | 10.33% |

| 3 | 7.37% | 9.00% | 10.47% |

| 2 | 7.26% | 9.00% | 10.63% |

| 1 | 7.13% | 9.00% | 10.80% |

Hence, above table shows the expected interest yield or current yield for each bond in each year.

2.

To compute: Expected capital gains yield for each bond in each year.

2.

Explanation of Solution

Expected capital gains yield for each bond in each year:

| N | Bond A | Bond B | Bond C |

| 12 | 0.83% | 0.00% | -0.62% |

| 11 | 0.90% | 0.00% | -0.68% |

| 10 | 0.97% | 0.00% | -0.75% |

| 9 | 1.05% | 0.00% | -0.82% |

| 8 | 1.13% | 0.00% | -0.90% |

| 7 | 1.22% | 0.00% | -0.99% |

| 6 | 1.31% | 0.00% | -1.09% |

| 5 | 1.41% | 0.00% | -1.21% |

| 4 | 1.52% | 0.00% | -1.33% |

| 3 | 1.63% | 0.00% | -1.47% |

| 2 | 1.74% | 0.00% | -1.63% |

| 1 | 1.87% | 0.00% | -1.80% |

Hence, above table shows the expected capital gains yield for each bond in each year.

3.

To compute: Total return for each bond in each year.

3.

Explanation of Solution

Given,

Expected total return for bond A, B and C is 9%.

Total return for each bond in each year:

| N | Bond A | Bond B | Bond C |

| 12 | 9.00% | 9.00% | 9.00% |

| 11 | 9.00% | 9.00% | 9.00% |

| 10 | 9.00% | 9.00% | 9.00% |

| 9 | 9.00% | 9.00% | 9.00% |

| 8 | 9.00% | 9.00% | 9.00% |

| 7 | 9.00% | 9.00% | 9.00% |

| 6 | 9.00% | 9.00% | 9.00% |

| 5 | 9.00% | 9.00% | 9.00% |

| 4 | 9.00% | 9.00% | 9.00% |

| 3 | 9.00% | 9.00% | 9.00% |

| 2 | 9.00% | 9.00% | 9.00% |

| 1 | 9.00% | 9.00% | 9.00% |

Hence, above table shows the total return for each bond in each year.

Want to see more full solutions like this?

Chapter 7 Solutions

Fundamentals Of Financial Management, Concise Edition (mindtap Course List)

- Clifford Clark is a recent retiree who is interested in investing some of his savings in corporate bonds. His financial planner has suggested the following bonds: Bond A has a 9% annual coupon, matures in 12 years, and has a $1,000 face value. Bond B has a 10% annual coupon, matures in 12 years, and has a $1,000 face value. Bond C has an 8% annual coupon, matures in 12 years, and has a $1,000 face value. Each bond has a yield to maturity of 9%.arrow_forwardEconomics Corus Berhad is interested to invest in bonds. Currently, the financial manager is evaluating both Bond A and Bond B. Bond A pays 8 percent coupon semi-annually and matures in 12 years. Bond B pays 7 percent coupon annually having a maturity period of 13 years. Determine the value of each bond if the current market yield for both bonds is 8 percent.arrow_forwardJason Greg is a recent retiree who is interested in investing some of his savings in corporate bonds. Listed below are the bonds he is considering adding to his portfolio. Bond A has a 7.5% semiannual coupon, matures in 12 years, and has a $1,000 face value. Bond B has a 10% semiannual coupon, matures in 12 years, and has a $1,000 face value. Bond C has an 11.5% semiannual coupon, matures in 12 years, and has a $1,000 face value. Each bond has a YTM of 10%. Before calculating the prices of the bonds, indicate whether each bond is trading at a premium, discount, or par. Calculate the price of each of these bonds. Calculate the current yield for each bond. If the yield to maturity for each bond remains at 9%, what will be the price of each bond 2 years from now? Greg is considering another bond, Bond D. It has an 8% semiannual coupon and a $1,000 face value. Bond D is scheduled to mature in 9 years and has a price of $1,150. It is also callable in 5 years at a call…arrow_forward

- What is the expected current yield for each bond in each year? Round your answers to two decimal places. Clifford Clark is a recent retiree who is interested in investing some of his savings in corporate bonds. His financial planner has suggested the following bonds: Bond A has a 9% annual coupon, matures in 12 years, and has a $1,000 face value. Bond B has a 10% annual coupon, matures in 12 years, and has a $1,000 face value. Bond C has an 8% annual coupon, matures in 12 years, and has a $1,000 face value. Each bond has a yield to maturity of 9%.arrow_forward(Bond valuation) You own a bond that pays $120 in annual interest, with a $1,000 par value. It matures in 20 years. Your required rate of return is 11 percent a. Calculate the value of the bond. b. How does the value change if your required rate of return (1) increases to 15 percent or (2) decreases to 7 percent? c. Explain the implications of your answers in part b as they relate to interest rate risk, premium bonds, and discount bonds. d. Assume that the bond matures in 4 years instead of 20 years. Recompute your answers in part b. e. Explain the implications of your answers in part d as they relate to interest rate risk, premlum bonds, and discount bonds.arrow_forward(Bond valuation) You own a bond that pays $120 in annual interest, with a $1,000 par value. It matures in 20 years. Your required rate of return is 10 percent. a. Calculate the value of the bond. b. How does the value change if your required rate of return (1) increases to 15 percent or (2) decreases to 6 percent? c. Explain the implications of your answers in part b as they relate to interest rate risk, premium bonds, and discount bonds. d. Assume that the bond matures in 3 years instead of 20 years. Recompute your answers in part b. e. Explain the implications of your answers in part d as they relate to interest rate risk, premium bonds, and discount bonds. a. If your required rate of return is 10 percent, what is the value of the bond? $ (Round to the nearest cent.)arrow_forward

- 3. You own several bonds and as an astute investor, you keep track of your interest payments (also known as coupon payments or cash flows). Annually, you receive a fixed total of interest payments of $2,000 per year from these bonds for the next 5 years and your required rate of return is 7.5%. What is the current value of your bond investment? Show your work and explain your answer.arrow_forwardWorking as an investment analyst for a fund that invests in fixed-income assets, you are tasked with evaluating the efficacy of a potential investment. You are given a bond that has a 5% coupon rate and matures in 5 years. Assume comparable debt yields 7% and that the bond is sold in increments of $1,000. What is the value of one increment of the bond?arrow_forwardAn investor wishes to invest $200,000 in bonds that mature in 4 years Question 3. and earn a yield to maturity of at least 3% per year. Currently she can buy 4 year treasury bonds at $102 per bond that have a yield to maturity of 2%. She decides to also buy some 4 year corporate bonds at $90 per bond that have a yield to maturity of 4%. Find the four year growth factor for each type of investment and derive the equations that must hold if her portfolio has the desired yield to maturity, How many corporate bonds, and how many 4 year treasuries, should she buy to ensure this? Give an answer in integers. Then determine how much of each type of bond she buys and what the total cost actually is. What will be the actual value of this portfolio after 4 years and what is the actual annual yield?arrow_forward

- Consider buying a $1,000-denomination corporate bond at the market price of $996.25. The interest will be paid semiannually at an interest rate per payment period of 4.8125%. Twenty interest payments over 10 years are required. We show the resulting cash flow to the investor as shown. Find the return on this bond investment (or yield to maturity).arrow_forwardHello! Im stuck at this homework. Clifford Clark is a recent retiree who is interested in investing some ofhis savings in corporate bonds. His financial planner has suggested the following bonds:● Bond A has a 6% annual coupon, matures in 15years, and has a $1,000 face value.● Bond B has a 8% annual coupon, matures in 15years, and has a $1,000 face value.● Bond C has an 10% annual coupon, matures in 15years, and has a $1,000 face value.Each bond has a yield to maturity of 8%.e. Mr. Clark is considering another bond, Bond D. It has an 7% semiannual coupon and a $1,000 face value. Interest is paid at the enf of each 6months. Bond is schedule to mature in 9 years and has a price of $1,200. It is also callable in 5 years at a call price of $1,050.1. What is the bond’s nominal yield to maturity?2. What is the bond’s nominal yield to call?3. If Mr. Clark were to purchase this bond, would he be more likely to receive the yield to maturity or yield to call? Explain your answer.arrow_forwardHello! Im stuck at this homework. Clifford Clark is a recent retiree who is interested in investing some ofhis savings in corporate bonds. His financial planner has suggested the following bonds:● Bond A has a 6% annual coupon, matures in 15years, and has a $1,000 face value.● Bond B has a 8% annual coupon, matures in 15years, and has a $1,000 face value.● Bond C has an 10% annual coupon, matures in 15years, and has a $1,000 face value.Each bond has a yield to maturity of 8%.C)how would the price be shown in the wall street journal? d) calculate the current yield for each of the three bonds d. If the yield to maturity for each bond remains at 8%, what will be the price of eachbond 1 year from now?arrow_forward

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education