Videos

Replacement Decisions Suppose we are thinking about replacing an old computer with a new one. The old one cost us $450,000; the new one will cost $580,000. The new machine will be depreciated straight-line to zero over its five-year life. It will probably be worth about $130,000 after five years. The old computer is being depreciated at a rate of $90,000 per year. It will be completely written off in three years. If we don’t replace it now, we will have to replace it in two years. We can sell it now for $230,000; in two years it will probably be worth $60,000. The new machine will save us $85,000 per year in operating costs. The tax rate is 38 percent and the discount rate is 14 percent.

- a. Suppose we recognize that if we don’t replace the computer now, we will be replacing it in two years. Should we replace now or should we wait? (Hint: What we effectively have here is a decision either to “invest” in the old computer-by not selling it-or to invest in the new one. Notice that the two investments have unequal lives.)

- b. Suppose we consider only whether we should replace the old computer now without worrying about what’s going to happen in two years. What are the relevant cash flows? Should we replace it or not? (Hint: Consider the net change in the firm’s aftertax cash flows if we do the replacement.)

a)

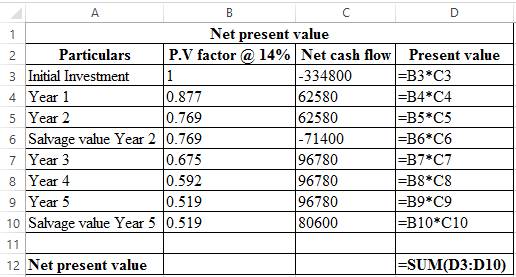

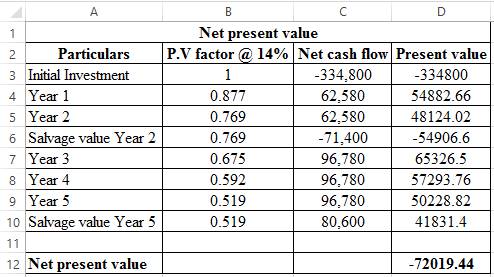

To determine: Net present value of the old and new computer.

Equivalent Annual Cost:

Equivalent annual cost is that cost which shows the operating and maintaining cost of the assets of whole life.

Net Present Value(NPV):

The net present value is differential amount between the net cash inflow from future investments and net cash outflow in the form of cost that the company has to pay at present as initial cost of the investment.

Explanation of Solution

Given,

Salvage value of the old computer is $230,000.

Salvage value of the computer after two years is $60,000.

Cost of new computer is $580,000.

Estimated life of the computer is 5 years.

Salvage value of the new computer is $130,000.

Operating cost is $85,000.

Discount rate is 14%.

Calculated values,

Book value of the old computer is $270,000.

Annual depreciation on the old computer is $90,000.

Formula to calculate the equivalent annual cost of the old computer,

Substitute-$133,966 for the net present value and 1.647 for the PVIFA.

Formula to calculate the equivalent annual cost of the new computer,

Substitute, -$205,923 for the net present value and 3.433 for the PVFA,

Working notes:

Calculate the operating cash flow of old computer,

Calculate the operating cash flow of new computer,

Calculate the present salvage value of new computer,

Calculate the present salvage value of the old computer,

Calculate the initial cost of the old computer,

Calculate the net present value of the old computer,

Calculate the net present value of the new computer,

Hence, equivalent annual cost of old and new computer is -$81,339 and -$59,983.

b)

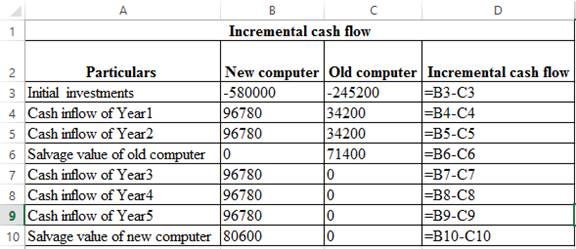

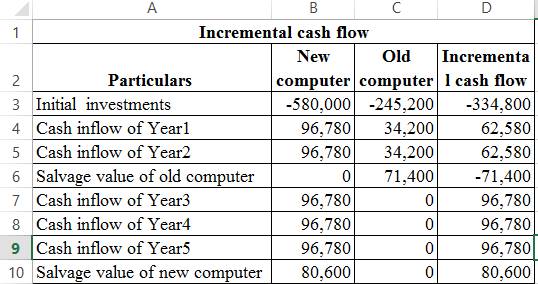

To determine: Incremental net present value.

Net Present Value(NPV):

The net present value is differential amount between the net cash inflow from future investments and net cash outflow in the form of cost that the company has to pay at present as initial cost of the investment.

Explanation of Solution

Formula to calculate the incremental net present value,

Working notes:

Calculate the incremental cash flows,

Hence, net present value is -$72,019.

Want to see more full solutions like this?

Chapter 6 Solutions

EBK CORPORATE FINANCE

- Suppose we are thinking about replacing an old computer with a new one. The old one cost us $1,660,000; the new one will cost, $2,001,000. The new machine will be depreciated straight-line to zero over its five-year life. It will probably be worth about $435,000 after five years. The old computer is being depreciated at a rate of $352,000 per year. It will be completely written off in three years. If we don't replace it now, we will have to replace it in two years. We can sell it now for $549,000; in two years, it will probably be worth $159,000. The new machine will save us $373,000 per year in operating costs. The tax rate is 25 percent, and the discount rate is 12 percent. a-1. Calculate the EAC for the the old computer and the new computer. (A negative answer should be indicated by a minus sign. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) a-2. What is the NPV of the decision to replace the computer now? (A negative answer should…arrow_forwardSuppose we are thinking about replacing an old computer with a new one. The old one cost us $1,620,000; the new one will cost, $1,949,000. The new machine will be depreciated straight-line to zero over its five-year life. It will probably be worth about $405,000 after five years. The old computer is being depreciated at a rate of $336,000 per year. It will be completely written off in three years. If we don't replace it now, we will have to replace it in two years. We can sell it now for $531,000; in two years, it will probably be worth $153,000. The new machine will save us $363,000 per year in operating costs. The tax rate is 23 percent, and the discount rate is 10 percent. a-1. Calculate the EAC for the the old computer and the new computer. (A negative answer should be indicated by a minus sign. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) a-2. What is the NPV of the decision to replace the computer now? (A negative answer should…arrow_forwardSuppose we are thinking about replacing an old computer with a new one. The old one cost us $1,680,000; the new one will cost, $2,027,000. The new machine will be depreciated straight-line to zero over its five-year life. It will probably be worth about $450,000 after five years. The old computer is being depreciated at a rate of $360,000 per year. It will be completely written off in three years. If we don't replace it now, we will have to replace it in two years. We can sell it now for $558,000; in two years, it will probably be worth $162,000. The new machine will save us $378,000 per year in operating costs. The tax rate is 21 percent, and the discount rate is 12 percent. a-1. Calculate the EAC for the the old computer and the new computer. (A negative answer should be indicated by a minus sign. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) a-2. What is the NPV of the decision to replace the computer now? (A negative answer should…arrow_forward

- Suppose we are thinking about replacing an old computer with a new one. The old one cost us $1,960,000; the new one will cost, $2,531,000. The new machine will be depreciated straight-line to zero over its five-year life. It will probably be worth about $660,000 after five years. The old computer is being depreciated at a rate of $472,000 per year. It will be completely written off in three years. If we don't replace it now, we will have to replace it in two years. We can sell it now for $684,000; in two years, it will probably be worth $204,000. The new machine will save us $413,000 per year in operating costs. The tax rate is 25 percent, and the discount rate is 8 percent. a-1. Calculate the EAC for the the old computer and the new computer. (A negative answer should be indicated by a minus sign. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) a - What is the NPV of the decision to replace the computer now? (A negative answer should be…arrow_forwardTyrell Corp. is considering replacing a machine. The old one is currently being depreciated at $70,000 per year (straight-line), and is scheduled to end in five years with no remaining book value. If you don’t replace it, you will be lucky to get it removed for the amount you could salvage it for, so you don’t expect any profit in five years. If you replace the old machine now, you believe you can salvage it for $375,000 and buy a new machine for $850,000, plus $25,000 shipping fee and another $25,000 for installation. The new machine will not change the revenue or NOWC, but it will reduce the operating costs of the company by $145,000 per year. The new machine will be depreciated using the three-year MACRS schedule (the table is provided on the Moodle for your convenience). The useful life of this machine is five years, and it is expected that the machine can be sold at $20,000 at the end of the five years. Assume a tax rate of 25% and the cost of capital for the company is 8%.…arrow_forwardDenny Corporation is considering replacing a technologically obsolete machine with a new state-of-the-art numerically controlled machine. The new machine would cost $340,000 and would have a ten-year useful life. Unfortunately, the new machine would have no salvage value. The new machine would cost $50,000 per year to operate and maintain, but would save $95,000 per year in labor and other costs. The old machine can be sold now for scrap for $30,000. The simple rate of return on the new machine is closest to (Ignore income taxes.): (Round your answer to 1 decimal place.)arrow_forward

- Tyrell Corp. is considering replacing a machine. The old one is currently being depreciated at $70,000 per year (straight-line), and is scheduled to end in five years with no remaining book value. If you don't replace it, you will be lucky to get it removed for the amount you could salvage it for, so you don't expect any profit in five years. If you replace the old machine now, you believe you can salvage it for $375,000 and buy a new machine for $850,000, plus $25,000 shipping fee and another $25,000 for installation. The new machine will not change the revenue or NOWC, but it will reduce the operating costs of the company by $145,000 per year. The new machine will be depreciated using the three-year MACRS schedule (the table is provided on the Moodle for your convenience). The useful life of this machine is five years, and it is expected that the machine can be sold at $20,000 at the end of the five years. Assume a tax rate of 25% and the cost of capital for the company is 8%.…arrow_forwardDenny Corporation is considering replacing a technologically obsolete machine with a new state-of-the-art numerically controlled machine. The new machine would cost $180,000 and would have a twelve-year useful life. Unfortunately, the new machine would have no salvage value. The new machine would cost $26, 000 per year to operate and maintain, but would save $58,000 per year in labor and other costs. The old machine can be sold now for scrap for $18,000. The simple rate of return on the new machine is closest to (Ignore income taxes.):arrow_forwardA packaging factory is considering the replacement of some equipment. The new plan is to install equipment to produce a new can that uses less energy and less metal than the old one. Current equipment was installed 5 years ago for $100 million and can be sold for $35 million. Due to obsolescence the depreciation of this equipment results in an annual depreciation of $4 million for the next years. If you keep this equipment for one more year your operating and maintenance costs will be $65 million increasing by $3 million/year each year thereafter. The new equipment will cost $130 million, with an economic life of 8 years and a salvage value of $10 million. Its operating and maintenance costs will be $49 million. For a TMAR = 15% p.a. what new equipment should be installed? Make a recommendation about it. (Answer: The solution would be to use the current equipment for another two years and then exchange it for new equipment.arrow_forward

- The management of Ballard MicroBrew is considering the purchase of an automated bottling machine for $55,000. The machine would replace an old piece of equipment that costs $14,000 per year to operate. The new machine would cost $6,000 per year to operate. The old machine currently in use could be sold now for a salvage value of $20,000. The new machine would have a useful life of 10 years with no salvage value. Required: 1. What is the annual depreciation expense associated with the new bottling machine? 2. What is the annual incremental net operating income provided by the new bottling machine? 3. What is the amount of the initial investment associated with this project that should be used for calculating the simple rate of return? 4. What is the simple rate of return on the new bottling machine? (Round your answer to 1 decimal place i.e. 0.123 should be considered as 12.3%.)arrow_forwardDenny Corporation is considering replacing a technologically obsolete machine with a new state-of-the-art numerically controlled machine. The new machine would cost $290,000 and have a tenericals controll nortunately, the new machine would have no salvage value. The new machine would cost $48,000 per year to operate and maintain but would save $89,000 per year in labor and other costs. The old machine can be sold now for scrap for $29,000. The simple rate of return on the new machine is closest to (Ignore income taxes.):arrow_forwardDell is considering replacing one of its material handling systems. It has an annual O&M cost of $48,000, a remaining operational life of 8 years, and an estimated salvage value of $6,000 at that time. A new system can be purchased for $175,000. It will be worth $50,000 in 8 years, and it will have annual O&M costs of only $17,000 per year due to new technology. If the new system is purchased, the old system will be traded in for $55,000, even though the old system can be sold for only $45,000 on the open market. Leasing a new system will cost $31,000 per year, payable at the beginning of the year, plus operating costs of $15,000 per year payable at the end of the year. If the new system is leased, the existing material handling system will be sold for its market value of $45,000. Use a planning horizon of 8 years, an annual worth analysis, and MARR of 15% to decide which material handling system to recommend: (i) keep existing, (ii) trade in existing and purchase new, or (iii)…arrow_forward