2.

Prepare

2.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in

stockholders’ equity accounts. - Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Prepare journal entry for the given transactions in a general journal.

| General Journal Page 3 | ||||||

| Date | Accounts Title and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| 2020 | ||||||

| January | 2 | Supplies | 121 | 7,000 | ||

| Cash | 101 | 7,000 | ||||

| (To record purchases of supplies for cash) | ||||||

| 2 | Prepaid Insurance | 134 | 8,400 | |||

| Cash | 101 | 8,400 | ||||

| (To record purchases of insurance for one year) | ||||||

| 7 | Cash | 101 | 20,000 | |||

| 111 | 5,000 | |||||

| Fees Income | 401 | 25,000 | ||||

| (To record services performed for cash and account) | ||||||

| 12 | Cash | 101 | 4,000 | |||

| Accounts Receivable | 111 | 4,000 | ||||

| (To record receipts of cash on account) | ||||||

| 12 | Advertising Expense | 526 | 3,600 | |||

| Cash | 101 | 3,600 | ||||

| (To record payment of advertising on radio) | ||||||

| 13 | Cash | 101 | 4,500 | |||

| Accounts Receivable | 111 | 4,500 | ||||

| (To record receipts of cash on account) | ||||||

| 14 | Cash | 101 | 750 | |||

| Supplies | 121 | 750 | ||||

| (To record damage supplies return for cash) | ||||||

| 15 | Cash | 101 | 20,700 | |||

| Accounts Receivable | 111 | 2,300 | ||||

| Fees Income | 401 | 23,000 | ||||

| (To record services performed for cash and account) | ||||||

Table (1)

| General Journal Page 4 | ||||||

| Date | Account Title and Explanation | Post. Ref. | Debit ($) | Credit ($) | ||

| 2020 | ||||||

| January | 20 | Supplies | 121 | 5,000 | ||

| Accounts Payable | 202 | 5,000 | ||||

| (To record purchases of supplies on account) | ||||||

| 20 | Cash | 101 | 12,500 | |||

| Accounts Receivable | 111 | 3,500 | ||||

| Fees Income | 401 | 16,000 | ||||

| (To record services performed for cash and account) | ||||||

| 20 | Cash | 101 | 5,600 | |||

| Accounts Receivable | 111 | 5,600 | ||||

| (To record the collection on account) | ||||||

| 21 | Maintenance Expense | 529 | 7,065 | |||

| Cash | 101 | 7,065 | ||||

| (To record the payment for maintenance on equipment) | ||||||

| 22 | Advertising Expense | 526 | 3,600 | |||

| Cash | 101 | 3,600 | ||||

| (To record payment of cash for newspaper ads) | ||||||

| 23 | Telephone Expense | 532 | 1,025 | |||

| Cash | 101 | 1,025 | ||||

| (To Record the payment of telephone bill) | ||||||

| 26 | Cash | 101 | 1,600 | |||

| Accounts Receivable | 111 | 1,600 | ||||

| (To record the collection on account) | ||||||

| 27 | Accounts Payable | 202 | 3,000 | |||

| Cash | 101 | 3,000 | ||||

| (To record the payment to creditors) | ||||||

Table (2)

| General Journal Page 5 | ||||||

| Date | Accounts Title and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| 2020 | ||||||

| January | 28 | Utilities Expense | 514 | 2,675 | ||

| Cash | 101 | 2,675 | ||||

| (To record the payment of utility bill) | ||||||

| 29 | Cash | 101 | 19,000 | |||

| Accounts Receivable | 111 | 2,750 | ||||

| Fees Income | 401 | 21,750 | ||||

| (To record services performed for cash and account) | ||||||

| 31 | Salaries Expense | 511 | 32,800 | |||

| Cash | 101 | 32,800 | ||||

| (To record payment of monthly salaries) | ||||||

| 31 | TE, Drawing | 302 | 12,000 | |||

| Cash | 101 | 12,000 | ||||

| (To record withdrawal of cash for personal use) | ||||||

| 31 | Maintenance Expense | 529 | 4,150 | |||

| Cash | 101 | 4,150 | ||||

| (To record payment of monthly maintenance services) | ||||||

| 31 | Equipment | 141 | 15,000 | |||

| Cash | 101 | 10,000 | ||||

| Accounts Payable | 202 | 5,000 | ||||

| (To record the purchases of equipment for cash and on account) | ||||||

| 31 | Cash | 101 | 7,600 | |||

| Accounts Receivable | 111 | 1,620 | ||||

| Fees Income | 401 | 9,220 | ||||

| (To record services performed for cash and account) | ||||||

Table (3)

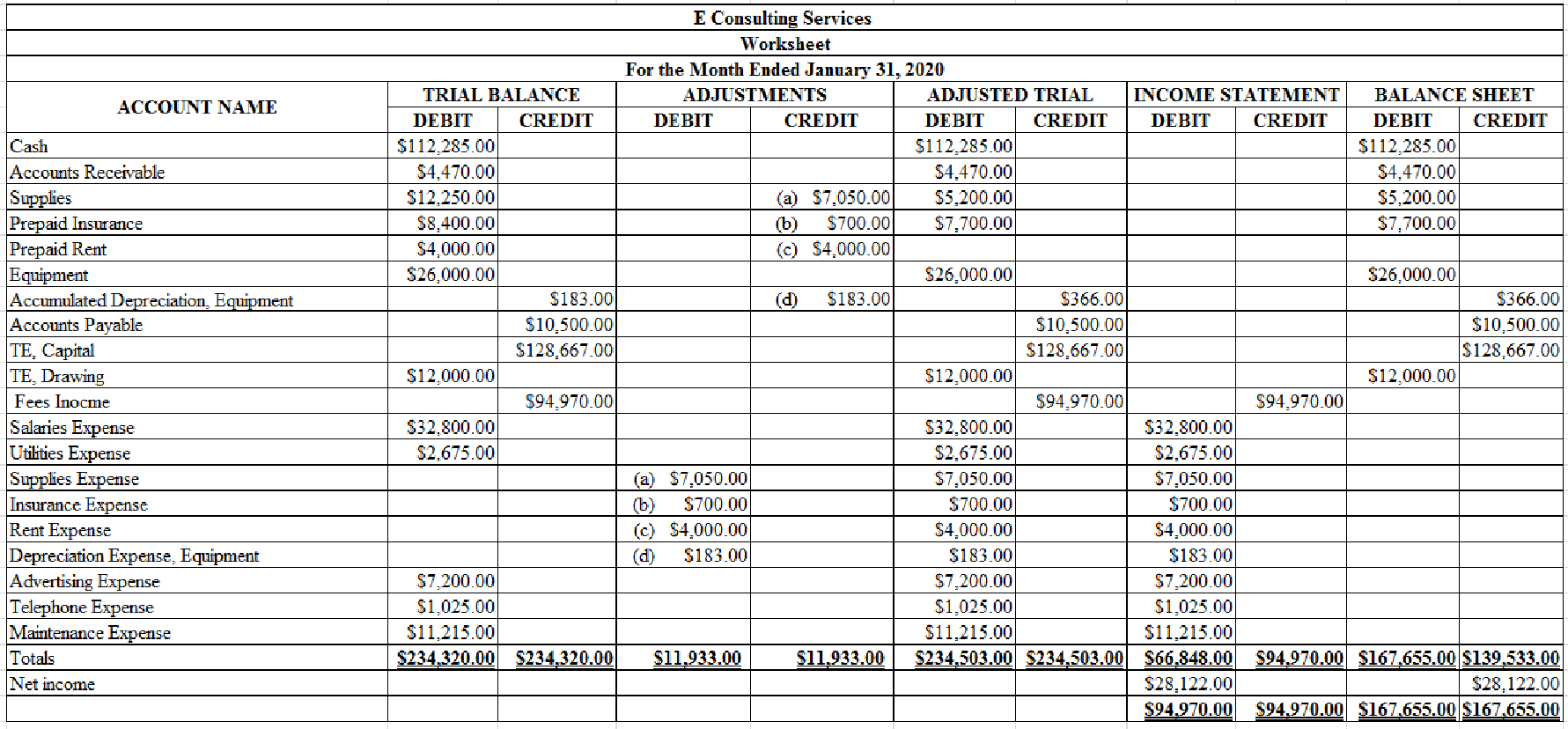

4, 5 and 6.

Prepare trail balance section, indicate the given adjustments, and complete the worksheet for E Consulting Services for the month ended January 31, 2020.

4, 5 and 6.

Explanation of Solution

Worksheet: Worksheet is an accounting tool that helps accountants to record adjustments and up-date balances required to prepare financial statements. Worksheet is a central place where

Prepare trail balance section, indicate the given adjustments, and complete the worksheet for E Consulting Services for the month ended January 31, 2020.

Table (4)

7.

Prepare income statement for E Consulting Services for the month ended January 31, 2020.

7.

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operation and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare income statement for E Consulting Services for the month ended January 31, 2020.

| E Consulting Services | ||

| Income Statement | ||

| For the Month Ended January 31, 2020 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Fees Income | 94,970 | |

| Expenses: | ||

| Salaries Expense | 32,800 | |

| Utilities Expense | 2,675 | |

| Supplies Expense | 7,050 | |

| Rent Expense | 4,000 | |

| Insurance Expense | 700 | |

| | 183 | |

| Advertising Expense | 7,200 | |

| Telephone Expense | 1,025 | |

| Maintenance Expense | 11,215 | |

| Total expenses | 66,848 | |

| Net income | $28,122 | |

Table (5)

8.

Prepare statement of owners’ equity for E Consulting Services for the month ended January 31, 2020.

8.

Explanation of Solution

Statement of owners’ equity: This statement reports the beginning owner’s equity and all the changes which led to ending owners’ equity. Additional capital, net income from income statement is added to, and drawings are deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Prepare a statement of owners’ equity for E Consulting Services for the month ended January 31, 2020.

| E Consulting Services | ||

| Statement of Owners’ Equity | ||

| For the Month Ended January 31, 2020 | ||

| Particulars | Amount ($) | Amount ($) |

| TE, Capital, January 1, 2020 | $128,667 | |

| Net income for January | 28,122 | |

| Less: Withdrawals for January | 12,000 | |

| Increase in capital | 16,122 | |

| HK, Capital, January 31, 2020 | $144,789 | |

Table (6)

9.

Prepare balance sheet for E Consulting Services as at January 31, 2020.

9.

Explanation of Solution

Balance sheet: This financial statement reports a company’s resources (assets) and claims of creditors (liabilities) and owners (owners’ equity) over those resources. The resources of the company are assets which include money contributed by owners and creditors. Hence, the main elements of the balance sheet are assets, liabilities, and owners’ equity.

Prepare the balance sheet for E Consulting Services as at January 31, 2020.

| E Consulting Services | ||

| Balance Sheet | ||

| January 31, 2019 | ||

| Assets | ||

| Cash | $112,285 | |

| Accounts Receivable | 4,470 | |

| Supplies | 5,200 | |

| Prepaid Insurance | 7,700 | |

| Equipment | $26,000 | |

| Less: | 336 | 25,634 |

| Total Assets | $155,289 | |

| Liabilities and owner’s equity | ||

| Liabilities | ||

| Accounts Payable | 10,500 | |

| Owners’ Equity | ||

| TE, Capital | 144,789 | |

| Total Liabilities and Owners’ Equity | $155,289 | |

Table (7)

10.

Prepare adjusting entry for the given adjustments.

10.

Explanation of Solution

Prepare adjusting entry for supplies.

| GENERAL JOURNAL | Page 6 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 31, 2019 | Supplies expense | 517 | 7,050 | |

| Supplies | 121 | 7,050 | ||

| (to record supplies used) | ||||

Table (8)

Description:

- Supplies Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Supplies are an asset account. Since amount of supplies is used, asset account decreased, and a decrease in asset is credited.

Prepare adjusting entry for insurance expense:

| GENERAL JOURNAL | Page 6 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 31, 2019 | Insurance expense | 535 | 700 | |

| Prepaid insurance | 134 | 700 | ||

| (to record part of prepaid insurance expired) | ||||

Table (9)

Description:

- Insurance Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Prepaid Insurance is an asset account. Since amount of insurance is expired, asset account decreased, and a decrease in asset is credited.

Prepare adjusting entry for rent expense:

| GENERAL JOURNAL | Page 6 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 31, 2019 | Rent expense | 520 | 4,000 | |

| Prepaid rent | 137 | 4,000 | ||

| (to record part of prepaid rent expired) | ||||

Table (10)

Description:

- Rent Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Prepaid Rent is an asset account. Since amount of rent is expired, asset account decreased, and a decrease in asset is credited.

Prepare adjusting entry for depreciation expense-equipment:

| GENERAL JOURNAL | Page 6 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| January 31, 2019 | Depreciation expense-Equipment | 523 | 183 | |

| Accumulated depreciation-Equipment | 142 | 183 | ||

| (to record depreciation expense) | ||||

Table (11)

Description:

- Depreciation Expense, Equipment is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Accumulated Depreciation, Equipment is a contra-asset account, and contra-asset accounts would have a normal credit balance, hence, the account is credited.

11.

Prepare closing entries in general ledger.

11.

Explanation of Solution

Closing entries: The journal entries prepared to close the temporary accounts to capital account are referred to as closing entries. The revenue, expense, and drawing accounts are referred to as temporary accounts because the information and figures in these accounts is held temporarily and consequently transferred to permanent account at the end of accounting year.

Steps in closing procedure:

- 1. Close the revenue accounts to Income Summary account.

- 2. Close the expense accounts to Income Summary account.

- 3. Close the Income Summary account and transfer the net income or net loss balance to the Capital account.

- 4. Close the Drawing account to Capital account.

Close the revenue accounts to Income Summary account.

| GENERAL JOURNAL | Page 6 | |||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| 2019 | Fees Income | 401 | 94,970 | |||

| January | 31 | Income Summary | 309 | 94,970 | ||

| (Record closing of revenue to Income Summary account) | ||||||

Table (12)

Description:

- Fees income is a revenue account. Revenue account has a normal credit balance. Since revenue is closed to Income Summary account, the account is debited.

- Income Summary is a clearing account which closes revenue, expense, drawings, and net of revenues and expenses to capital accounts. The account is credited to hold the transferred balance from revenue account.

Close the expense accounts to Income Summary account.

| GENERAL JOURNAL | Page 6 | |||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| 2019 | Income Summary | 309 | 19,980 | |||

| January | 31 | Salaries Expense | 511 | 32,800 | ||

| Utilities Expense | 514 | 2,675 | ||||

| Supplies Expense | 517 | 7,050 | ||||

| Rent Expense | 520 | 4,000 | ||||

| Depreciation Expense, Equipment | 523 | 183 | ||||

| Advertising Expense | 526 | 7,200 | ||||

| Maintenance Expense | 529 | 11,215 | ||||

| Telephone Expense | 532 | 1,025 | ||||

| Insurance Expense | 535 | 700 | ||||

| (Record closing of expenses to Income Summary account) | ||||||

Table (13)

Description:

- Income Summary is a clearing account which closes revenue, expense, drawings, and net of revenues and expenses to capital accounts. The account is debited to hold the transferred balance from expense accounts.

- Salaries expense, Utilities expense, Supplies expense, Rent expense, Depreciation expense, Advertising expense, Maintenance expense, Telephone expense, and Insurance expense are expense accounts. Expense account has a normal debit balance. Since expenses are closed to Income Summary account, the accounts are credited.

Close the net income to Income Summary account.

| GENERAL JOURNAL | Page 6 | |||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| 2019 | Income Summary | 309 | 28,122 | |||

| January | 31 | TE, Capital | 301 | 28,122 | ||

| (Record closing of net income to capital account) | ||||||

Table (14)

Description:

- Income Summary is a clearing account which closes revenue, expense, drawings, and net of revenues and expenses to capital accounts. Since net income is closed, the account is reversed; hence, the Income Summary account is debited.

- TE, Capital is a capital account. Since net income is transferred to the account, the value increased, and an increase in capital is credited.

Working Note 1:

Compute net income.

Close the Drawing account to Capital account.

| GENERAL JOURNAL | Page 6 | |||||

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| 2019 | TE, Capital | 12,000 | ||||

| January | 31 | TE, Drawing | 12,000 | |||

| (Record closing of drawing to capital account) | ||||||

Table (15)

Description:

- TE, Capital is a capital account. Since drawings are transferred to the account, the value decreased, and a decrease in capital is debited.

- TE, Drawing is a capital account. Since drawings are transferred, the account is credited to reverse the previously debited effect.

1, 3, 10, and 11.

Open the general ledger account, enter the balance for January 1, 2020, and post the journal entries, adjusting entries, and closing entries.

1, 3, 10, and 11.

Explanation of Solution

Open the general ledger account, enter the balance for January 1, 2020, and post the journal entries, adjusting entries, and closing entries.

| ACCOUNT: Cash ACCOUNT NO. 101 | |||||||

| DATE | Item | Post Ref. | Debit ($) | Credit ($) | BALANCE | ||

| Debit ($) | Credit ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 111,350 | |||

| 2 | J3 | 7,000 | 104,350 | ||||

| 2 | J3 | 8,400 | 95,950 | ||||

| 7 | J3 | 20,000 | 115,950 | ||||

| 12 | J3 | 4,000 | 119,950 | ||||

| 12 | J3 | 3,600 | 116,350 | ||||

| 13 | J3 | 4,500 | 120,850 | ||||

| 14 | J3 | 750 | 121,600 | ||||

| 15 | J4 | 20,700 | 142,300 | ||||

| 20 | J4 | 12,500 | 154,800 | ||||

| 20 | J4 | 5,600 | 160,400 | ||||

| 21 | J4 | 7,065 | 153,335 | ||||

| 22 | J4 | 3,600 | 149,735 | ||||

| 23 | J4 | 1,025 | 148,710 | ||||

| 26 | J4 | 1,600 | 150,310 | ||||

| 27 | J5 | 3,000 | 147,310 | ||||

| 28 | J5 | 2,675 | 144,635 | ||||

| 29 | J5 | 19,000 | 163,635 | ||||

| 31 | J5 | 32,800 | 130,835 | ||||

| 31 | J5 | 12,000 | 118,835 | ||||

| 31 | J5 | 4,150 | 114,685 | ||||

| 31 | J5 | 10,000 | 104,685 | ||||

| 31 | J5 | 7,600 | 112,285 | ||||

Table (16)

| ACCOUNT: Accounts Receivable ACCOUNT NO. 111 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

|

DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 5,000 | |||

| 7 | J3 | 5,000 | 10,000 | ||||

| 12 | J3 | 4,000 | 6,000 | ||||

| 13 | J3 | 4,500 | 1,500 | ||||

| 15 | J4 | 2,300 | 3,800 | ||||

| 20 | J4 | 3,500 | 7,300 | ||||

| 20 | J4 | 5,600 | 1,700 | ||||

| 26 | J4 | 1,600 | 100 | ||||

| 29 | J5 | 2,750 | 2,850 | ||||

| 31 | J5 | 1,620 | 4,470 | ||||

Table (17)

| ACCOUNT: Supplies ACCOUNT NO. 121 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 1,000 | |||

| 2 | J3 | 7,000 | 8,000 | ||||

| 14 | J3 | 750 | 7250 | ||||

| 20 | J4 | 5,000 | 12,250 | ||||

| 31 | Adjusting | J6 | 7,050 | 5,200 | |||

Table (18)

| ACCOUNT: Accounts Payable ACCOUNT NO. 202 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 3,500 | |||

| 20 | J4 | 5,000 | 8,500 | ||||

| 27 | J5 | 3,000 | 5,500 | ||||

| 31 | J5 | 5,000 | 10,500 | ||||

Table (19)

| ACCOUNT: TE, Capital ACCOUNT NO. 301 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 128,667 | |||

| 31 | Closing | J6 | 34,597 | 163,264 | |||

| 31 | Closing | J6 | 15,000 | 148,264 | |||

Table (20)

| ACCOUNT: TE, Drawing ACCOUNT NO. 302 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | J5 | 12,000 | 12,000 | |||

| 31 | Closing | J6 | 12,000 | ||||

Table (21)

| ACCOUNT: Prepaid Insurance ACCOUNT NO. 134 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 2 | J3 | 8,400 | 8,400 | |||

| 31 | Adjusting | J6 | 700 | 7,700 | |||

Table (22)

| ACCOUNT: Prepaid Rent ACCOUNT NO. 137 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 4,000 | |||

| 31 | Adjusting | J6 | 4,000 | ||||

Table (23)

| ACCOUNT: Equipment ACCOUNT NO. 141 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 11,000 | |||

| 31 | J5 | 15,000 | 26,000 | ||||

Table (24)

| ACCOUNT: Accumulated Depreciation-Equipment ACCOUNT NO. 142 | |||||||

| DATE | Item | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 1 | Balance | ✔ | 183 | |||

| 31 | Adjusting | J6 | 183 | 366 | |||

Table (25)

| ACCOUNT: Income Summary ACCOUNT NO. 309 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | Closing | J6 | 94,970 | 94,970 | ||

| 31 | Closing | J6 | 66,848 | 28,122 | |||

| 31 | Closing | J6 | 28,122 | ||||

Table (26)

| ACCOUNT: Fees Income ACCOUNT NO. 401 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 7 | J3 | 25,000 | 25,000 | |||

| 15 | J4 | 23,000 | 48,000 | ||||

| 20 | J4 | 16,000 | 64,000 | ||||

| 29 | J5 | 21,750 | 85,750 | ||||

| 31 | J5 | 9,220 | 94,970 | ||||

| 31 | Closing | J6 | 94,970 | ||||

Table (27)

| ACCOUNT: Salaries Expense ACCOUNT NO. 511 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | J5 | 32,800 | 32,800 | |||

| 31 | Closing | J6 | 32,800 | ||||

Table (28)

| ACCOUNT: Utilities Expense ACCOUNT NO. 514 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 28 | J5 | 2,675 | 2,675 | |||

| 31 | Closing | J6 | 2,675 | ||||

Table (29)

| ACCOUNT: Supplies Expense ACCOUNT NO. 517 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | Adjusting | J6 | 7,050 | 7,050 | ||

| 31 | Closing | J6 | 7,050 | ||||

Table (30)

| ACCOUNT: Rent Expense ACCOUNT NO. 520 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | Adjusting | J6 | 4,000 | 4,000 | ||

| 31 | Closing | J6 | 4,000 | ||||

Table (31)

| ACCOUNT: Depreciation Expense -Equipment ACCOUNT NO. 523 | |||||||

| DATE | ITEM | POST.REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | Adjusting | J6 | 183 | 183 | ||

| 31 | Closing | J6 | 183 | ||||

Table (32)

| ACCOUNT: Advertising Expense ACCOUNT NO. 526 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 12 | J3 | 3,600 | 3,600 | |||

| 22 | J4 | 3,600 | 7,200 | ||||

| 31 | Closing | J6 | 7200 | 0 | |||

Table (33)

| ACCOUNT: Maintenance Expense ACCOUNT NO. 529 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 21 | J4 | 7,065 | 7,065 | |||

| 31 | J5 | 4,150 | 11,215 | ||||

| 31 | Closing | J6 | 11,215 | 0 | |||

Table (34)

| ACCOUNT: Telephone Expense ACCOUNT NO. 532 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 23 | J4 | 1,025 | 1,025 | |||

| 31 | Closing | J6 | 1,025 | 0 | |||

Table (35)

| ACCOUNT: Insurance Expense ACCOUNT NO. 535 | |||||||

| DATE | ITEM | POST REF. | DEBIT ($) | CREDIT ($) | BALANCE | ||

| DEBIT ($) | CREDIT ($) | ||||||

| 2020 | |||||||

| January | 31 | Adjusting | J6 | 700 | 700 | ||

| 31 | Closing | J6 | 700 | 0 | |||

Table (36)

12.

Prepare a post-closing trial balance for E Consulting Services as at January 31, 2020.

12.

Explanation of Solution

Post-closing trial balance: Post-closing trial balance is a summary of all the assets, liabilities, and capital accounts and their balances, after the closing entries are prepared. So, post-closing trial balance reports the balances of permanent accounts only.

Prepare a post-closing trial balance for E Consulting Services as at January 31, 2020.

|

E Consulting Services Post- closing Trial Balance January 31, 2020 | ||

| Account Title |

Debit ($) |

Credit ($) |

| Cash | 112,285 | |

| Accounts Receivable | 4,470 | |

| Supplies | 5,200 | |

| Prepaid Insurance | 7,700 | |

| Equipment | 26,000 | |

| Accumulated Depreciation | 366 | |

| Accounts Payable | 10,500 | |

| TE, Capital | 144,789 | |

| Total | 155,655 | 155,655 |

Table (37)

Analyze the changes of total assets, liabilities, and the ending balance of owner’s capital of by comparing the January 31, 2020 balance sheet and December 31, 2019 balance sheet.

Explanation of Solution

The total assets are increased by $23,122

The total liabilities are increased by $7,000

The Owner’s capital is increased by $16,122

Analyze the changes arisen in cash and accounts receivable accounts.

Explanation of Solution

The cash account is increased by $935

The accounts receivable account is decreased by $530

Analyze the improvement in the firm’s financial position.

Explanation of Solution

The firm’s capital is increased by $16,122

Want to see more full solutions like this?

Chapter 6 Solutions

COLLEGE ACCOUNTING (LL)W/ACCESS>CUSTOM<

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning