Concept explainers

Videos

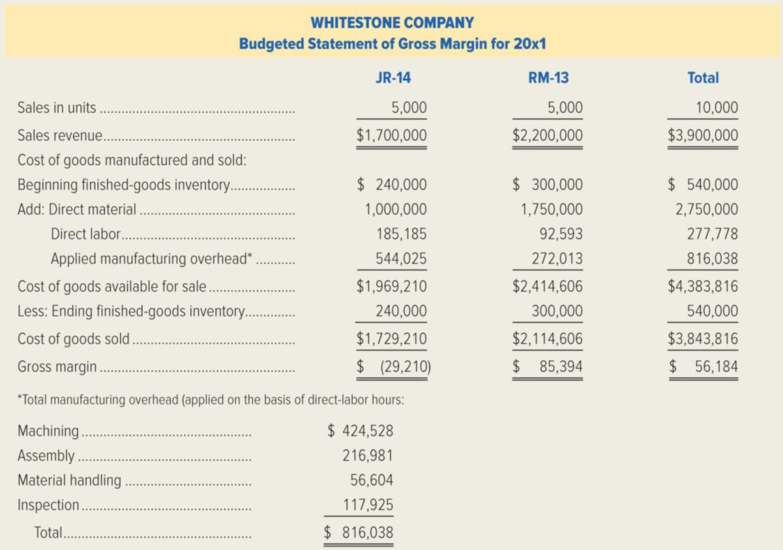

Whitestone Company produces two subassemblies, JR-14 and RM-13, used in manufacturing trucks. The company is currently using an absorption costing system that applies overhead based on direct labor hours. The budget for the current year ending December 31, 20x1, is as follows:

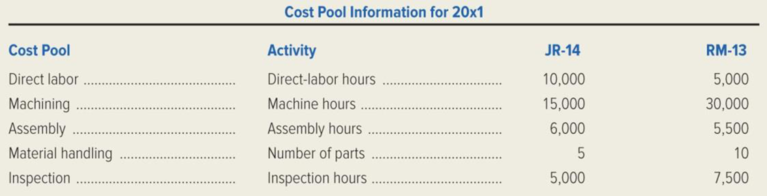

Mark Ward, Whitestone’s president, has been reading about a product-costing method called activity-based costing. Ward is convinced that activity-based costing will cast a new light on future profits. As a result, Brian Walters, Whitestone’s director of cost management, has accumulated cost pool information for this year shown on the following chart. This information is based on a product mix of 5,000 units of JR-14 and 5,000 units of RM-13.

In addition, the following information is projected for the next calendar year, 20x2.

On January 1, 20x2, Whitestone is planning to increase the prices of JR-14 to $355 and RM-13 to $455. Material costs are not expected to increase in 20x2, but direct labor will increase by 8 percent, and all

Whitestone uses a just-in-time inventory system and has materials delivered to the production facility directly from the vendors. The raw-material inventory at both the beginning and the end of the month is immaterial and can be ignored for the purposes of a

Required:

- 1. Explain how activity-based costing differs from traditional product-costing methods.

- 2. Using activity-based costing, calculate the total cost for the following activity cost pools: machining, assembly, material handling, and inspection. (Round to the nearest dollar.) Then, calculate the pool rate per unit of the appropriate cost driver for each of the four activities. (Hint: Refer to Exhibit 5–6, regarding calculation of the pool rate.)

- 3. Prepare a table showing for each product line the estimated 20x2 cost for each of the following cost elements: direct material, direct labor, machining, assembly, material handling, and inspection. (Round to the nearest dollar.)

- 4. Prepare a budgeted statement showing the gross margin for Whitestone Company for 20x2, using activity-based costing. The statement should show each product and a total for the company. Be sure to include detailed calculations for the cost of goods manufactured and sold. (Round each amount in the statement to the nearest dollar.)

Want to see the full answer?

Check out a sample textbook solution

Chapter 5 Solutions

MANAGERIAL ACCOUNTING-CUSTOM EBOOK>I<

- Evans, Inc., has a unit-based costing system. Evanss Miami plant produces 10 different electronic products. The demand for each product is about the same. Although they differ in complexity, each product uses about the same labor time and materials. The plant has used direct labor hours for years to assign overhead to products. To help design engineers understand the assumed cost relationships, the Cost Accounting Department developed the following cost equation. (The equation describes the relationship between total manufacturing costs and direct labor hours; the equation is supported by a coefficient of determination of 60 percent.) Y=5,000,000+30X,whereX=directlaborhours The variable rate of 30 is broken down as follows: Because of competitive pressures, product engineering was given the charge to redesign products to reduce the total cost of manufacturing. Using the above cost relationships, product engineering adopted the strategy of redesigning to reduce direct labor content. As each design was completed, an engineering change order was cut, triggering a series of events such as design approval, vendor selection, bill of materials update, redrawing of schematic, test runs, changes in setup procedures, development of new inspection procedures, and so on. After one year of design changes, the normal volume of direct labor was reduced from 250,000 hours to 200,000 hours, with the same number of products being produced. Although each product differs in its labor content, the redesign efforts reduced the labor content for all products. On average, the labor content per unit of product dropped from 1.25 hours per unit to one hour per unit. Fixed overhead, however, increased from 5,000,000 to 6,600,000 per year. Suppose that a consultant was hired to explain the increase in fixed overhead costs. The consultants study revealed that the 30 per hour rate captured the unit-level variable costs; however, the cost behavior of other activities was quite different. For example, setting up equipment is a step-fixed cost, where each step is 2,000 setup hours, costing 90,000. The study also revealed that the cost of receiving goods is a function of the number of different components. This activity has a variable cost of 2,000 per component type and a fixed cost that follows a step-cost pattern. The step is defined by 20 components with a cost of 50,000 per step. Assume also that the consultant indicated that the design adopted by the engineers increased the demand for setups from 20,000 setup hours to 40,000 setup hours and the number of different components from 100 to 250. The demand for other non-unit-level activities remained unchanged. The consultant also recommended that management take a look at a rejected design for its products. This rejected design increased direct labor content from 250,000 hours to 260,000 hours, decreased the demand for setups from 20,000 hours to 10,000 hours, and decreased the demand for purchasing from 100 component types to 75 component types, while the demand for all other activities remained unchanged. Required: 1. Using normal volume, compute the manufacturing cost per labor hour before the year of design changes. What is the cost per unit of an average product? 2. Using normal volume after the one year of design changes, compute the manufacturing cost per hour. What is the cost per unit of an average product? 3. Before considering the consultants study, what do you think is the most likely explanation for the failure of the design changes to reduce manufacturing costs? Now use the information from the consultants study to explain the increase in the average cost per unit of product. What changes would you suggest to improve Evanss efforts to reduce costs? 4. Explain why the consultant recommended a second look at a rejected design. Provide computational support. What does this tell you about the strategic importance of cost management?arrow_forwardYoung Company is beginning operations and is considering three alternatives to allocate manufacturing overhead to individual units produced. Young can use a plantwide rate, departmental rates, or activity-based costing. Young will produce many types of products in its single plant, and not all products will be processed through all departments. In which one of the following independent situations would reported net income for the first year be the same regardless of which overhead allocation method had been selected? a. All production costs approach those costs that were budgeted. b. The sales mix does not vary from the mix that was budgeted. c. All manufacturing overhead is a fixed cost. d. All ending inventory balances are zero.arrow_forwardBig Mikes, a large hardware store, has gathered data on its overhead activities and associated costs for the past 10 months. Nizam Sanjay, a member of the controllers department, believes that overhead activities and costs should be classified into groups that have the same driver. He has decided that unloading incoming goods, counting goods, and inspecting goods can be grouped together as a more general receiving activity, since these three activities are all driven by the number of receiving orders. The 10 months of data shown below have been gathered for the receiving activity. Required: 1. Prepare a scattergraph, plotting the receiving costs against the number of purchase orders. Use the vertical axis for costs and the horizontal axis for orders. 2. Select two points that make the best fit, and compute a cost formula for receiving costs. 3. Using the high-low method, prepare a cost formula for the receiving activity. 4. Using the method of least squares, prepare a cost formula for the receiving activity. What is the coefficient of determination?arrow_forward

- Bumblebee Mobiles manufactures a line of cell phones. The management has identified the following overhead costs and related cost drivers for the coming year. The following were incurred in manufacturing two of their cell phones, Bubble and Burst, during the first quarter. REQUIREMENT Review the worksheet called ABC that follows these requirements. You have been asked to determine the cost of each product using an activity-based cost system. Note that the problem information is already entered into the Data Section of the ABC worksheet.arrow_forwardThe management of Hartman Company is trying to determine the amount of each of two products to produce over the coming planning period. The following information concerns labor availability, labor utilization, and product profitability: a. Develop a linear programming model of the Hartman Company problem. Solve the model to determine the optimal production quantities of products 1 and 2. b. In computing the profit contribution per unit, management does not deduct labor costs because they are considered fixed for the upcoming planning period. However, suppose that overtime can be scheduled in some of the departments. Which departments would you recommend scheduling for overtime? How much would you be willing to pay per hour of overtime in each department? c. Suppose that 10, 6, and 8 hours of overtime may be scheduled in departments A, B, and C, respectively. The cost per hour of overtime is 18 in department A, 22.50 in department B, and 12 in department C. Formulate a linear programming model that can be used to determine the optimal production quantities if overtime is made available. What are the optimal production quantities, and what is the revised total contribution to profit? How much overtime do you recommend using in each department? What is the increase in the total contribution to profit if overtime is used?arrow_forwardThe cost accountant of L. Rosales, Inc. is considering to use the ABC system in determining the cost of its products. At present, the company uses the traditional costing systems wherein factory overhead costs are allocated based on direct labor hours. This cost accountant believes that the present system may be providing misleading cost information, hence, the plan to change to ABC system. For the coming period, the company is planning to use 5,000 direct labor hours, and its total budgeted factory overhead amounts to P 90,000, broken down as follows: Activity Cost Driver Budgeted Activity Budgeted Cost Sets up cost Number of set ups 40 P 20,000 Production monitoring Number of batches 20 40,000 Quality control Number of inspections 1,000 30,000 Total overhead…arrow_forward

- Uses activity-based costing in their manufacturing process. The company produces two products, ABC and XYZ. SCS has provided their costing department the following information from this year's budget relating to the production of these two products: Units to be produced Machine-hours expected Direct labor-hours expected Materials handling (number of moves) Machine setups (number of setups) The following costs are expected to be incurred throughout the year and are related to the cost drivers being measured: Expected Total Costs Direct Labor Wages Materials handling Labor-related overhead Machine setups $110,000 $8,800 $92,400 $15,400 Select one: O O O O O ABC XYZ 8,000 12,000 440 220 440 660 132 154 44 33 What is the expected overhead allocated per unit of product ABC? NOTE: Round all per-unit amounts to the nearest cent. a. $1.61 b. $5.64 c. $11.33 d. $6.23 e. None of the amounts listed.arrow_forwardEcco Ltd is engaged in the manufacture of components for the computer hardware industry. The factory consists of three production departments, A, B and C and a number of service departments. The costing system uses a single production overhead absorption rate expressed as a percentage of direct labour cost. A newly qualified accountant has just joined the company and has expressed a view that departmental overhead absorption rates would result in more accurate job costs. With this in mind, she has produced the following budgeted information for the next year. The budgeted production overheads in each department are after the allocation of service department costs. (a) State with reasons, whether you agree with the view that ‘departmental overhead absorption rates would result in more accurate job costs’ and outline why a company would calculate predetermined annual overhead absorption rates as opposed to rates calculated from actual weekly or monthly activity and expenditure. (b) (i)…arrow_forwardMajan Plastic Industries produces two categories of products: Plastic Products and Rubber Products. They are deciding whether to use Traditional costing or activity based costing. Based on next year's budget, two cost pools have been developed with the following information: Plastic Products Rubber Products OH Direct Labour 10000 5000 Machine Hours 6500 3500 500000 machine setup 2000 3000 100000 Required: a) Compute the plant-wide overhead rate if overhead is applied based on direct labor hours. b) Compute the overhead rates using activity based costing. c) Determine the difference in the amount of overhead allocated to each product between the two methods.arrow_forward

- Mission Company is preparing its annual profit plan. As part of its analysis of the profitability of individual products, the controller estimates the amount of overhead that should be allocated to the individual product lines from the information provided below. (CMA adapted) Multiple Choice Units produced Material moves per product line Direct labor-hours per product line Budgeted material handling costs: $279,500 Under an activity-based costing (ABC) system, the materials handling costs allocated to one unit of Specialty Windows would be: $6,450.00. $2,170.68. $12,900.00. Wall Mirrors 220 5 1,100 $10,320.00. Specialty Windows 20 60 1,200arrow_forwardThe controller of Ferrence Company estimates the amount of materials handling overhead cost that should be allocated to the company's two products using the data that are given below: The total materials handling cost for the year is expected to be $16,486.40. If the materials handling cost is allocated on the basis of material moves, how much of the total materials handling cost should be allocated to the specialty windows? (Round off your answer to the nearest whole dollar.) Question 12 options: $3,266 $9,274 $8,243 $6,595arrow_forwardThe Bangor Manufacturing Company makes mechanical toy robots that are typically produced in batches of 250 units. Prior to the current year, the company’s accountants used a standard cost system with a simplified method of assigning manufacturing support (i.e., overhead) costs to products: All such costs were allocated to outputs based on the standard machine hours allowed for output produced. You have recently joined the accounting team and are developing a proposal that the company adopt an ABC system for both product-costing and control purposes. To illustrate the benefit of such a system in terms of the latter, you decide to put together an analysis of batch-related overhead costs. You chose these costs because a previous investigation indicated that there is both a variable component to these costs (materials plus power) plus a fixed component (depreciation and salaries). Last year’s budget indicated that the variable overhead cost per setup hour was $20.00 and that the fixed…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning