Intermediate Financial Management (MindTap Course List)

13th Edition

ISBN: 9781337395083

Author: Eugene F. Brigham, Phillip R. Daves

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 5, Problem 3MC

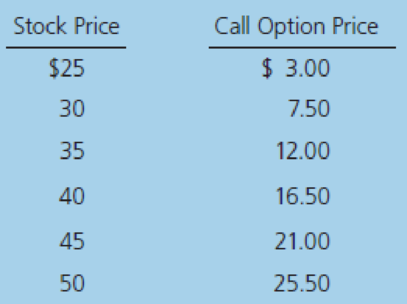

Consider Triple Play’s call option with a $25 strike price. The following table contains historical values for this option at different stock prices:

- (1) Create a table that shows (a) stock price, (b) strike price, (c) exercise value, (d) option price, and (e) the time value, which is the option’s price less its exercise value.

- (2) What happens to the time value as the stock price rises? Why?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

In the derivation of the option pricing formula, we required that a delta-hedged position earn the risk-free rate of return. A different approach to pricing an option is to impose the condition that the actual expected return on the option must equal the equilibrium expected return.

Suppose the risk premium on the stock is 0.03, the price of the underlying stock is 111, the call option price is 4.63, and the delta of the call option is 0.4.

Determine the risk premium on the option.

General Finance

Assume an investor buys a share of stock for $18 at t = 0 and at the end of the next year (t = 1) , he buys 12 shares with a unit price of $9 per share. At the end of Year 2 (t = 2) , the investor sells all shares for $40 per share. At the end of each year in the holding period, the stock paid a $5.00 per share dividend. What is the annual time-weighted rate of return?

Chapter 5 Solutions

Intermediate Financial Management (MindTap Course List)

Ch. 5 - Define each of the following terms:

Option; call...Ch. 5 - Prob. 2QCh. 5 - Prob. 3QCh. 5 - Prob. 1PCh. 5 - The exercise price on one of Flanagan Companys...Ch. 5 - Black-Scholes Model

Assume that you have been...Ch. 5 - Put–Call Parity

The current price of a stock is...Ch. 5 - Prob. 5PCh. 5 - Binomial Model The current price of a stock is 20....Ch. 5 - Prob. 7P

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Please don't use Ai solutionarrow_forwardA flowchart that depicts the relationships among the input, processing, and output of an AIS is A. a system flowchart. B. a program flowchart. C. an internal control flowchart. D. a document flowchart.arrow_forwardA flowchart that depicts the relationships among the input, processing, and output of an AIS is A. a system flowchart. B. a program flowchart. C. an internal control flowchart. D. a document flowchart.arrow_forward

- Please write proposal which needs On the basis of which you will be writing APR. Write review of at least one article on the study area (Not title) of your interest, which can be finance related study area. Go through the 1. Study area selection (Topic Selection) 2. Review of Literature and development of research of framework 3. Topic Selection 4. Further review of literature and refinement of research fraework 5. Problem definition and research question…arrow_forwardLet it denote the effective annual return achieved on an equity fund achieved between time (t-1) and time t. Annual log-returns on the fund, denoted by In(1+i̟²), are assumed to form a series of independent and identically distributed Normal random variables with parameters µ = 7% and σ = 10%. An investor has a liability of £20,000 payable at time 10. Calculate the amount of money that should be invested now so that the probability that the investor will be unable to meet the liability as it falls due is only 5%. Express your answer to the NEAREST INTEGER and do NOT include a "£" sign. Note: From standard Normal tables, we have (-1.645) = 0.05.arrow_forwardFor this question, use this data: myFunc = function (x, y = 2) {z = 7 Z+x^2+y } What is the output of myFunc(2)? O 13. O An error, y is undefined. O Nothing, we have to assign it as a vari O 9.arrow_forward

- a medical test has some probability of being positive if the patient has the disease (hasPos) and another probability of testing positive if the person does not have the disease (notHasPos). a random member of the entire population has a real problem of having the disease (actual incidence). Based on the attached information what does the result of the function?arrow_forwardmyFunc = function (x, y = 2) {z = 7 } z+x^2+y Assuming that this was the first thing entered in a new R session, if the next command entered is z+1, what is the output? O 8. ● An error, z does not exist. O 10. O 7.arrow_forwardDon't used Ai solutionarrow_forward

- Literature Review Based Essay on Contemporary Issues of Business Ethics and Corporate Social Responsibility Essay Format Cover Page with your Name Table of Content • Introduction ⚫ Objectives ⚫ Discussion with Literature Support • Conclusion References (10+) Words Limit-3000-3500 wordsarrow_forwardPlease don't use hand ratingarrow_forward"Dividend paying stocks cannot be growth stocks" Do you agree or disagree? Discuss choosing two stocks to help justify your view.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

Intermediate Financial Management (MindTap Course...

Finance

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:9781337514835

Author:MOYER

Publisher:CENGAGE LEARNING - CONSIGNMENT

Accounting for Derivatives Comprehensive Guide; Author: WallStreetMojo;https://www.youtube.com/watch?v=9D-0LoM4dy4;License: Standard YouTube License, CC-BY

Option Trading Basics-Simplest Explanation; Author: Sky View Trading;https://www.youtube.com/watch?v=joJ8mbwuYW8;License: Standard YouTube License, CC-BY