Intermediate Financial Management

14th Edition

ISBN: 9780357516782

Author: Brigham, Eugene F., Daves, Phillip R.

Publisher: Cengage Learning

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 5, Problem 3MC

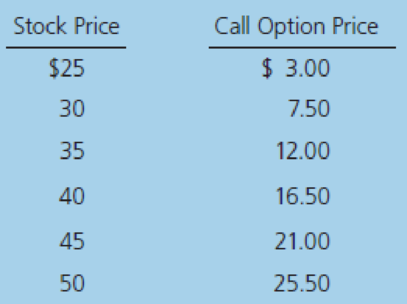

Consider Triple Play’s call option with a $25 strike price. The following table contains historical values for this option at different stock prices:

- (1) Create a table that shows (a) stock price, (b) strike price, (c) exercise value, (d) option price, and (e) the time value, which is the option’s price less its exercise value.

- (2) What happens to the time value as the stock price rises? Why?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

In the Black-Scholes option pricing model, the value of a call is inversely related to: a. the risk-free interest stock b. the volatility of the stock c. its time to expiration date d. its stock price e. its strike price

What impact does each of the followingparameters have on the value of a call option?(1) Current stock price

Both call and put options are affected by the following five factors: the exercise price, the underlying stock price, the time to expiration, the stock’s standard deviation, and the risk-free rate. However, the direction of the effects on call and put options could be different.

Use the following table to identify whether each statement describes put options or call options.

Statement

Put Option

Call Option

1. When the exercise price increases, option prices increase.

2. An option is more valuable the longer the maturity.

3. The effect of the time to maturity on the option prices is indeterminate.

4. As the risk-free rate increases, the value of the option increases.

Chapter 5 Solutions

Intermediate Financial Management

Ch. 5 - Define each of the following terms:

Option; call...Ch. 5 - Prob. 2QCh. 5 - Prob. 3QCh. 5 - Prob. 1PCh. 5 - The exercise price on one of Flanagan Companys...Ch. 5 - Black-Scholes Model

Assume that you have been...Ch. 5 - Put–Call Parity

The current price of a stock is...Ch. 5 - Prob. 5PCh. 5 - Binomial Model The current price of a stock is 20....Ch. 5 - Prob. 7P

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Which of the following describes delta? O The ratio of the option price to the stock price None of these O The ratio of a change in the option price to the corresponding change in the stock price The ratio of a change in the stock price to the corresponding change in the option price O The ratio of the stock price to the option price ◄ Previous Next ▸arrow_forwardIf the stock price increases, the price of a put option on that stock ________ and that of a call option _________. decreases, increases decreases, decreases increases, decreases increases, increasesarrow_forwardSuppose that call options on a stock with strike prices $100 and $106 cost $8 and $5, respectively. How can the options be (the profits from option positions and the total profit).arrow_forward

- Explain in detail with an example how the change of the variables (like Stock Price, Exercise Price, Risk-Free Rate, Volatility or Standard Deviation, and Time to Expiration) of Black-Scholes-Merton Formula affect the price of the option.arrow_forwardDescribe the effect of a change in each of the following factors on the value of a calloption:1. Stock price2. Exercise price3. Option life4. Risk-free ratearrow_forwardSuppose that put options on a stock with strike prices $18 and $20 cost $2 and $3.50, respectively. How can the options be used to create a bull spread? Construct atable that shows the profit and payoff for the spread.arrow_forward

- Describe the effect of a change in each of the following factorson the value of a call option: (1) stock price, (2) exercise price,(3) option life, (4) risk-free rate, and (5) stock return standarddeviation (i.e., risk of stock).arrow_forwardBoth call and put options are affected by the following five factors: the exercise price, the underlying stock price, the time to expiration, the stock’s standard deviation, and the risk-free rate. However, the direction of the effects on call and put options could be different. Use the following table to identify whether each statement describes put options or call options. Statement Put Option Call Option 1. An option is more valuable the longer the maturity. 2. A longer maturity in-the-money option on a risky stock is more valuable than the same shorter maturity option. 3. When the exercise price increases, option prices increase. 4. As the risk-free rate increases, the value of the option increases.arrow_forwardWe showed in the text that the value of a call option increases with the volatility of the stock. Is this also true of put option values? Use the put-call parity theorem as well as a numerical example to prove your answer.arrow_forward

- Label the following for this diagram: a. Name of options payoff b. Identify whether positive or negative premium c. Identify break-even point d. What is the profit or loss when stock price is $60 at maturity e. Suppose you have this options position, should you exercise your right (if any) assuming that the stock price is $60 at maturity? Option Payoffs and Profits Long put $40 $20 $0 Option Payoff Option Profit ---- Exercise Price -$20 -$40 $0 $20 $40 $60 $80 Stock Price At Maturity Payoff and Profitarrow_forwardWhat are the steps in valuing a call option when the binomial tree describing an underlying stock price has more than one sequential up/down jumps?arrow_forwardWhich of the following statements true? A call option price is increasing in stock return volatility A put option price is decreasing in stock return volatility I. II. A) I. and II. are true B) I. is true and II. is false C) II. is true and I. is false D) I. and II. are false |arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...

Finance

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Cengage Learning

Accounting for Derivatives Comprehensive Guide; Author: WallStreetMojo;https://www.youtube.com/watch?v=9D-0LoM4dy4;License: Standard YouTube License, CC-BY

Option Trading Basics-Simplest Explanation; Author: Sky View Trading;https://www.youtube.com/watch?v=joJ8mbwuYW8;License: Standard YouTube License, CC-BY