Concept explainers

Videos

T accounts,

The unadjusted

| Epicenter Laundry Unadjusted Trial Balance June 30, 2016 |

||

| Debit Balances | Credit Balances | |

| Cash............................................................. | 11,000 | |

| Laundry Supplies................................................. | 21,500 | |

| Prepaid Insurance................................................. | 9,600 | |

| Laundry Equipment............................................... | 232,600 | |

| 125,400 | ||

| Accounts Payable................................................. | 11,800 | |

| Common Stock................................................... | 40,000 | |

| 65,600 | ||

| Dividends....................................................... | 10,000 | |

| Laundry Revenue................................................. | 232,200 | |

| Wages Expense................................................... | 125,200 | |

| Rent Expense..................................................... | 40,000 | |

| Utilities Expense.................................................. | 19,700 | |

| Miscellaneous Expense............................................ | 5,400 | |

| 475,000 | 475,000 | |

The data needed to determine year-end adjustments are as follows:

- a. Laundry supplies on hand at June 30 are $3,600.

- b. Insurance premiums expired during the year are $5,700.

- c. Depreciation of laundry equipment during the year is $6,500.

- d. Wages accrued but not paid at June 30 are $1,100.

Instructions

- 1. For each account listed in the unadjusted trial balance, enter the balance in a T account. Identify the balance as “June 30 Bal." In addition, add T accounts for Wages Payable, Depreciation Expense, Laundry Supplies Expense, Insurance Expense, and Income Summary.

- 2. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. Add the accounts listed in part (1) as needed.

- 3. Journalize and post the adjusting entries. Identify the adjustments by "Adj." and the new balances as “Adj. BAL.”

- 4. Prepare an adjusted trial balance.

- 5. Prepare an income statement, a retained earnings statement, and a balance sheet.

- 6. Journalize and

post the closing entries. Identify the closing entries by “Clos." - 7. Prepare a post-closing trial balance.

1, 3, and 6:

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr) and,

- The credit side (Cr).

Adjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Adjusting entries:

An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

Spreadsheet:

A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Retained Earnings Statement:

It is one of the financial statements, which shows the amount of the net income retained by a company at a particular point of time for reinvestment and pay its debts and obligations. It shows the amount of retained earnings that is not paid as dividends to the shareholders.

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

Closing entries:

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

To prepare: The T-accounts.

Explanation of Solution

Record the transactions directly in their respective T-accounts, and determine their balances.

| Cash | |||||||||||

| June 30 | Balance | 11,000 | |||||||||

| Laundry Supplies | |||||||||||

| June 30 | Balance | 21,500 | June 30 | Adjusted | 17,900 | ||||||

| June 30 | Adjusted balance | 3,600 | |||||||||

| Prepaid Insurance | |||||||||||

| June 30 | Balance | 9,600 | June 30 | Adjusted | 5,700 | ||||||

| Adjusted balance | 3,900 | ||||||||||

| Laundry Equipment | |||||||||||

| June 30 | Balance | 232,600 | |||||||||

| Accumulated Depreciation | |||||||||||

| June 30 | Balance | 125,400 | |||||||||

| June 30 | Adjusted | 6,500 | |||||||||

| June 30 | Adjusted balance | 131,900 | |||||||||

| Accounts Payable | |||||||||||

| June 30 | Balance | 11,800 | |||||||||

| Wages Payable | |||||||||||

| June 30 | Adjusted | 1,100 | |||||||||

| Retained Earnings | |||||||||||

| June 30 | Closing | 10,000 | June 30 | Balance | 65,600 | ||||||

| June 30 | Closing | 10,700 | |||||||||

| June 30 | Balance | 66,300 | |||||||||

| Dividends | |||||||||||

| June 30 | Balance | 10,000 | June 30 | Closing | 10,000 | ||||||

| Laundry Revenue | |||||||||||

| June 30 | Closing | 232,200 | June 30 | Balance | 232,200 | ||||||

| Wages Expense | |||||||||||

| June 30 | Balance | 125,200 | June 30 | Closing | 126,300 | ||||||

| June 30 | Adjusted | 1,100 | |||||||||

| June 30 | Adjusted balance | 126,300 | |||||||||

| Rent Expense | |||||||||||

| June 30 | Balance | 40,000 | June 30 | Closing | 40,000 | ||||||

| Utilities Expense | |||||||||||

| June 30 | Balance | 19,700 | June 30 | Closing | 19,700 | ||||||

| Depreciation Expense | |||||||||||

| June 30 | Adjusted | 6,500 | June 30 | Closing | 6,500 | ||||||

| Laundry Supplies Expense | |||||||||||

| June 30 | Adjusted | 17,900 | June 30 | Closing | 17,900 | ||||||

| Insurance Expense | |||||||||||

| June 30 | Adjusted | 5,700 | June 30 | Closing | 5,700 | ||||||

| Miscellaneous Expense | |||||||||||

| June 30 | Balance | 5,400 | June 30 | Closing | 5,400 | ||||||

| Common Stock | |||||

| June 30 | Closing | 40,000 | |||

| Income Summary | |||||

| June 30 | Closing | 221,500 | June 30 | Closing | 232,200 |

| Closing | 10,700 | ||||

Table (1)

2.

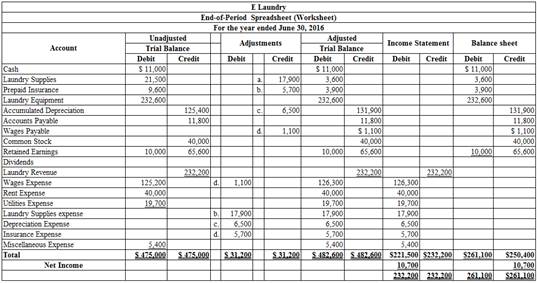

To enter: The unadjusted trial balances on an end-of-period spreadsheet, and complete the spreadsheet.

Explanation of Solution

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (2)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

3.

To Journalize and post: The adjusting entries.

Explanation of Solution

The adjusting entries are journalized as follows:

| Date | Description | Debit ($) | Credit ($) | |

| 2016 | Wages expense | 1,100 | ||

| June | 30 | Wages payable | 1,100 | |

| (To record the wages accrued) | ||||

Table (3)

- Wages expense is an expense account, and it is increased. Hence, debit the wages expense account by $1,100.

- Wages payable is a liability account, and it is increased. Hence, credit the wages payable account by $1,100.

| Date | Description | Debit ($) | Credit ($) | |

| 2016 | Depreciation expense | 6,500 | ||

| June | 30 | Accumulated depreciation | 6,500 | |

| (To record the equipment depreciation) | ||||

Table (4)

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $6,500.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $6,500.

| Date | Description | Debit ($) | Credit ($) | |

| 2016 | Laundry supplies expense | 17,900 | ||

| June | 30 | Laundry supplies

|

17,900 | |

| (To record the supplies expense) | ||||

Table (5)

- Laundry supplies expense is an expense account, and it is increased. Hence, debit the laundry supplies expense account by $17,900.

- Laundry supplies are the asset account, and it is increased. Hence, credit the laundry supplies account by $17,900.

| Date | Description | Debit ($) | Credit ($) | |

| 2016 | Insurance expense | 5,700 | ||

| August | 31 | Prepaid insurance | 5,700 | |

| (To record the insurance expense) | ||||

Table (6)

- Insurance expense is an expense account, and it is increased. Hence, debit the insurance expense account by $5,700.

- Prepaid insurance is an asset account, and it is decreased. Hence, credit the prepaid insurance account by $5,700.

4.

To prepare: An adjusted trial balance for Laundry E, as of June 30, 2016.

Explanation of Solution

Prepare an adjusted trial balance for Laundry E, as of June 30, 2016.

| Laundry E | ||

| Adjusted Trial Balance | ||

| June 30, 2016 | ||

| Accounts | Debit Balances | Credit Balances |

| Cash | 11,000 | |

| Laundry Supplies | 3,600 | |

| Prepaid Insurance | 3,900 | |

| Laundry Equipment | 232,600 | |

| Accumulated depreciation | 131,900 | |

| Accounts payable | 11,800 | |

| Wages Payable | 1,100 | |

| Common Stock | 40,000 | |

| Retained earnings | 65,600 | |

| Dividends | 10,000 | |

| Laundry revenue | 232,200 | |

| Wages expense | 126,300 | |

| Rent expense | 40,000 | |

| Utilities Expense | 19,700 | |

| Depreciation Expense | 17,900 | |

| Laundry supplies expense | 6,500 | |

| Insurance Expense | 5,700 | |

| Miscellaneous Expense | 5,400 | |

| 482,600 | 482,600 | |

Table (7)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $482,600.

5.

Explanation of Solution

The net income of Laundry E for the month of June is $10,700.

| E Laundry | ||

| Income Statement | ||

| For the year ended June 30, 2016 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenue: | ||

| Laundry revenue | $248,000 | |

| Expenses: | ||

| Wages Expense | $126,300 | |

| Rent Expense | 40,000 | |

| Utilities Expense | 19,700 | |

| Depreciation Expense | 17,900 | |

| Laundry supplies Expense | 6,500 | |

| Insurance Expense | 5,700 | |

| Miscellaneous Expense | 5,400 | |

| Total Expenses | 221,500 | |

| Net Income | $10,700 | |

Table (8)

Hence, the net income of Laundry E for the year ended June 30, 2016 is $10,700.

6.

To Journalize: The closing entries for E Laundry.

Explanation of Solution

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. | Debit ($) |

Credit ($) |

| June 30, 2016 | Laundry Revenue | 232,200 | ||

| Income Summary | 232,200 | |||

| (To record the closure of revenues account ) | ||||

| June 30 | Income Summary | 221,500 | ||

| Wages Expense | 126,300 | |||

| Rent Expense | 40,000 | |||

| Utilities Expense | 19,700 | |||

| Depreciation Expense | 6,500 | |||

| Laundry supplies Expense | 17,900 | |||

| Insurance Expense | 5,700 | |||

| Miscellaneous Expense | 5,400 | |||

| (To close the revenues and expenses account. Then the balance amount are transferred to income summary account) | ||||

| June 30 | Income Summary | 10,700 | ||

| Retained earnings | 10,700 | |||

| (To record the closure of net income from income summary to retained earnings) | ||||

| Retained earnings | 10,000 | |||

| Dividends | 10,000 | |||

| (To record the closure of dividend to retained earnings) | ||||

Table (11)

Laundry revenue account has a normal credit balance of $232,200 in total, now to close this account, the laundry revenue account must be debited with $232,200 and, income summary account must be credited with $232,200.

- In this closing entry, the laundry revenue account balance is being transferred to the income summary account, to bring the revenues account balance to zero.

- Thereby, the income summary account balance gets increased by $232,200 and, the revenue account balance gets decreased by $232,200.

All expenses accounts have a normal debit balance, the total of expenses are $221,500 have to be closed by transferring these account balances to the income summary account. All expenses account must be credited, and the income summary account must be debited with $ 221,500.

- In this closing entry, all the expenses account balances are transferred to the income summary account, to bring the expenses account balances to zero.

- Thereby, both the income summary account, and the expenses account balances get decreased by $221,500.

Determined amount balance of income summary is $10,700, which has to be closed by debiting the income summary account with $10,700, and crediting the retained earnings account with $10,700.

- In this closing entry, the income summary account balance is being transferred to the retained earnings account, to bring the income summary account balance to zero.

- Thereby, the income summary account gets decreased, and the retained earnings account balance gets increased by $10,700.

Dividends account has a normal debit balance of $10,000, now to close this account, retained earnings account must be debited with $10,000 and, dividend account must be credited with $10,000.

- In this closing entry, the dividend account balance is being transferred to the retained earnings account, to bring the dividend account balance to zero.

- Thereby, the retained earnings account balance gets increased by $10,000 and, the dividend account balance gets decreased by $10,000.

7.

To prepare: The post–closing trial balance of E Laundry for the month ended June 30, 2016.

Explanation of Solution

Prepare a post–closing trial balance of E Laundry for the month ended June 30, 2016 as follows:

Laundry E Post-closing Trial Balance June 30, 2016 |

||

| Particulars | Debit $ | Credit $ |

| Cash | 11,000 | |

| Laundry Supplies | 3,600 | |

| Prepaid insurance | 3,900 | |

| Laundry Equipment | 232,600 | |

| Accumulated depreciation | 131,900 | |

| Accounts payable | 11,800 | |

| Wages payable | 1,100 | |

| Common stock | 40,000 | |

| Retained earnings | 66,300 | |

| Total | $251,100 | $251,100 |

Table (12)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $251,100.

Want to see more full solutions like this?

Chapter 4 Solutions

Bundle: Financial & Managerial Accounting, 13th + CengageNOWv2, 2 terms (12 months) Printed Access Card

- UNCOLLECTIBLE ACCOUNTSALLOWANCE METHOD Lewis Warehouse used the allowance method to record the following transactions, adjusting entries, and closing entries during the year ended December 31, 20--: Selected accounts and beginning balances on January 1, 20--, are as follows: REQUIRED 1. Open the three selected general ledger accounts. 2. Enter the transactions and the adjusting and closing entries in a general journal (page 6). After each entry, post to the appropriate selected accounts. 3. Determine the net realizable value as of December 31, 20--.arrow_forwardUse the following items taken from the financial statements of the Postal Service for the year ending December 31, 2018 to answer questions: Accounts payable ..............................................................$10,000 Accounts receivable ............................................................11,000 Accumulated depreciation – equipment ..........................28,000 Advertising expense ............................................................21,000 Cash ......................................................................................14,000 Owner’s capital (1/1/18) ...................................................105,000 Owner’s drawings ...............................................................14,000 Depreciation expense ........................................................12,000 Insurance expense ...............................................................3,000 Note payable, due 6/30/19…arrow_forwardComplex Company prepares monthly financial statements. Below are listed some selected accounts and their balances in the September 30 trial balance before any adjustments have been made for the month of September. Instruction: Using the information given, prepare the adjusting entries that should be made by Complex Company on September 30. Complex COMPANY Trial Balance (Selected Accounts) September 30, 2010 Debit Credit Office Supplies....................................................................................$ 2,700 Prepaid Insurance..............................................................................$4,200 Office Equipment............................................................................. $16,200 Accumulated Depreciation—Office…arrow_forward

- QUESTION 2 Study the following transactions that occurred during August 2022 for Renwick & Co. Aug 2 - Renwick & Co. sold 40 office desks costing $2,000 each, at a unit price of $4,500 to Shams Ltd. Terms: 2/10, n/30. Aug 7- Shams Ltd. Returned for full credit 6 of the desks acquired on August 2 because they were of the incorrect size and style. Aug 8 - Renwick & Co. returned the office desks to its inventory. Aug 9 - Renwick & Co. received payment by cheque from Shams Ltd. for 30 office desks. Aug 27 - Renwick & Co. received payment in cash from Shams Ltd. in full settlement for the remaining office desks acquired on August 2. Renwick & Co. uses the net method to record sales and cash discounts and the perpetual inventory system. You may copy and paste from this list: Accounts receivable Discount Interest income Bad debt expense Bank Cash Cost of Goods Sold COGS REQUIRED: Interest receivable Inventory Notes receivable Par Premium Sales discounts Sales discounts forfeited Sales returns…arrow_forwardJournalize the purchase of the putters on account on the 8th. Date Accounts and Explanation Nov. 8 Debit Creditarrow_forwardThe post-closing trial balance of Beamer Manufacturing Co. onApril 30 is reproduced as follows:Beamer Manufacturing Co.Post-Closing Trial BalanceApril 30, 2011 Cash . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 25,000Accounts Receivable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65,000Finished Goods .................................. 120,000Work in Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35,000Materials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18,000Building . . . ...................................... 480,000Accumulated Depreciation—Building ............. $ 72,000Factory Equipment . . ............................ 220,000Accumulated Depreciation—Factory Equipment . . . 66,000Office Equipment ................................ 60,000Accumulated Depreciation—Office Equipment . . . . 36,000Accounts Payable . . .............................. 95,000Capital Stock…arrow_forward

- Requirement No. General Journal No. Date July 01 Date June 30 General Ledger Each journal entry is posted automatically to the general ledger. Think of the general ledger as sorting all of your journal entries by account title. Click on any of the individual amounts to return to the underlying journal entry. Cash Debit Common stock Debit Trial Balance Credit Credit 000 Schedule of Receivables General Ledger Account Balance 27,000 Balance 1 of 1 Income Statement MacBook Air F6 Merchandise Inventory Debit Impact on Income Next F7 Credit DII FO Balance 13,000arrow_forwardThe adjusted Trail Balance of Saudi Gold Co Contained the following accounts at November 30, the end of the company’s fiscal year : Saudi Gold Co. Adjusted Trial Balance November 30, 2019 Dr. Cr. Cash............................................................... Sr 28,700 Accounts Receivable..................................... 33,700 Inventory........................................................ 45,000 Supplies......................................................... 1,500 Equipment...................................................... 133,000 Accumulated Depreciation—Equipment..... Sr 39,000 Notes Payable................................................ 51,000 Accounts Payable......................................... 48,500 Share Capital—Ordinary............................... 90,000 Retained…arrow_forward1. Prepare a November 30 balance sheet in proper form for Green Bay Delivery Service from the following alphabetical list of the accounts at November 30: Accounts receivable.......................$10,000Accounts payable................................18,000Building..............................................28,000Cash..................................................8,000Notes payable.....................................45,000Office equipment...................................12,000R. Perkins, Capital................................?Trucks...............................................55,000arrow_forward

- On January 1, 2024, Rick's Pawn Shop leased a truck from Corey Motors for a six-year period with an option to extend the lease for three years. • Rick's had no significant economic incentive as of the beginning of the lease to exercise the three-year extension option. Annual lease payments are $12,000 due on December 31 of each year, calculated by the lessor using a 7% discount rate. . The expected useful life of the asset is nine years, and its fair value is $90,000. . Assume that at the beginning of the third year, January 1, 2026, Rick's had made significant improvements to the truck whose cost could be recovered only if it exercises the extension option, creating an expectation that extension of the lease was "reasonably certain." The relevant interest rate at that time was 8%. Note: Use tables, Excel, or a financial calculator. (FV of $1. PV of $1. FVA of $1. PVA of $1. EVAD of $1 and PVAD of $1) Required: 1. Prepare the journal entry, if any, on January 1 and on December 31 of…arrow_forwardA summary of Klugman Company's December 31, 2021. accounts receivable aging schedule is presented below along with the: estimáted percent uncollectible for each age group: Age Group 0-69 days 61-98 days 01 123 days Dver 128 days Amount $55,000 19,500 2,500 1, 000 0.5 1.0 10.0 50.0 The allowance fer uncollectible accounts had a balance of $1,350 on January 1, 20211. During the year, bad debts of $700 were. written of: Required: Prepare all joumal entries for 2021 with respect to bad debts and the aflowance for uncollectible accounts. (f no entry is required fain a transaction/event, select "No journat entry requirEG" in the first account fielld.) w transaCtion ist Journal entry worksheet Record the entry to write-off specific accounts.arrow_forwardWhich one of the following journal entry is Correct on 1st January 2020? a. Debit Purchase OMR 11,400 Credit Accounts payable OMR 11,400 b. Debit Accounts receivable OMR 11,400 Credit Sales OMR 11,400 c. Debit Purchase OMR 12,000 Credit Accounts payable OMR 12,000 d. Debit Accounts payable OMR 12,000 Credit Purchase returns and allowances OMR 12,000arrow_forward

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,