Videos

The following transactions occurred during the 2020 fiscal year for the City of Evergreen. For budgetary purposes, the city reports encumbrances in the Expenditures section of its budgetary comparison schedule for the General Fund but excludes expenditures chargeable to a prior year’s appropriation.

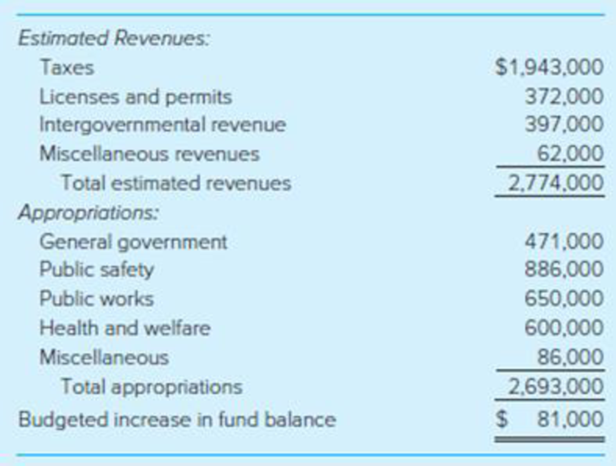

- 1. The budget prepared for the fiscal year 2020 was as follows:

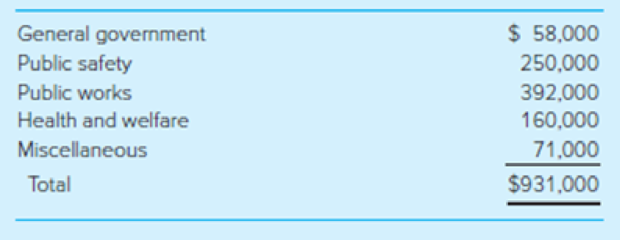

- 2. Encumbrances issued against the appropriations during the year were as follows:

- 3. The current year’s tax levy of $2,005,000 was recorded; uncollectibles were estimated as $65,000.

- 4. Tax collections of the current year’s levy totaled $1,459,000. The City also collected $132,000 in taxes from the prior year’s levy in the first 60 days after year end. (These delinquent collections had been anticipated prior to year-end.)

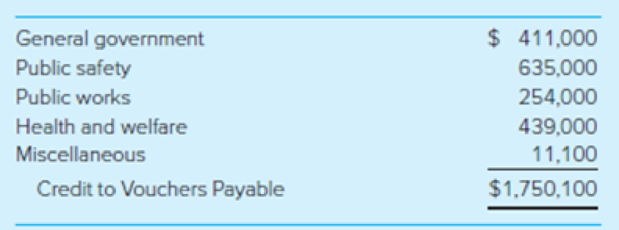

- 5. Personnel costs during the year were charged to the following appropriations in the amounts indicated. Encumbrances were not recorded for personnel costs. Because no liabilities currently exist for withholdings, you may ignore any FICA or federal or state income tax withholdings. (Expenditures charged to Miscellaneous should be treated as General Government expenses in the governmental activities general journal at the government-wide level.)

- 6. Invoices for all items ordered during the prior year were received and approved for payment in the amount of $14,470. Encumbrances had been recorded in the prior year for these items in the amount of $14,000. The amount chargeable to each year’s appropriations should be charged to the Public Safety appropriation.

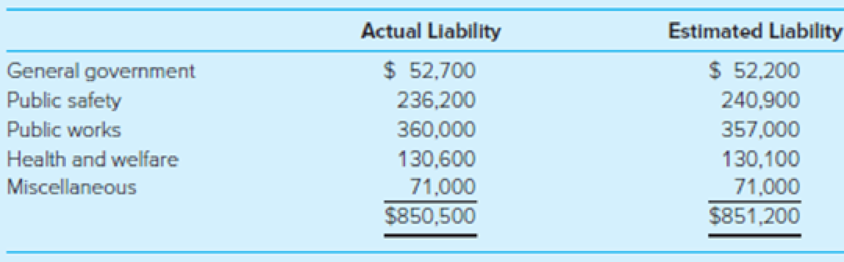

- 7. Invoices were received and approved for payment for items ordered in documents recorded as encumbrances in Transaction (2) of this problem. The following appropriations were affected.

- 8. Revenue other than taxes collected during the year consisted of licenses and permits, $373,000; intergovernmental revenue, $400,000; and $66,000 of miscellaneous revenues. For purposes of accounting for these revenues at the government-wide level, the intergovernmental revenues were operating grants and contributions for the Public Safety function. Miscellaneous revenues are not identifiable with any function and, therefore, are recorded as General Revenues at the government-wide level.

- 9. Payments on Vouchers Payable totaled $2,505,000.

Additional information follows: The General Fund Fund Balance—Unassigned account had a credit balance of $96,900 as of December 31, 2019; no entries have been made in the Fund Balance—Unassigned account during 2020.

Required

- a. Record the preceding transactions in general journal form for fiscal year 2020 in both the General Fund and governmental activities general journals.

- b. Prepare a budgetary comparison schedule for the General Fund of the City of Evergreen for the fiscal year ending December 31, 2020, as shown in Illustration 4-6. Do not prepare a government-wide statement of activities because other governmental funds would affect that statement.

a.

Journalize the given transactions for the fiscal year 2020 in General Fund and governmental activities general journals.

Explanation of Solution

General Fund: The chief operating fund of state and local government used to record the departmental operating activities and government support services is referred to as General Fund, or General Operating Fund, or General Revenue Fund. The activities recorded in General Funds are police, fire, public works, recreation, education, culture, social services, city office, finance, personnel, and data processing.

Journalize the given transactions for the fiscal year 2020 in General Fund and governmental activities general journals.

1.

Entry to record the budget:

| General Ledger | Subsidiary Ledger | |||||

| Debits | Credits | Debits | Credits | |||

| General Fund: | ||||||

| Estimated Revenues | $2,774,000 | |||||

| Budgetary Fund Balance | $81,000 | |||||

| Appropriations | 2,693,000 | |||||

| Estimated Revenues Ledger: | ||||||

| Taxes | $1,943,000 | |||||

| Licenses and Permits | 372,000 | |||||

| Internalgovernmental Revenue | 397,000 | |||||

| Miscellaneous Revenues | 62,000 | |||||

| Appropriations Ledger: | ||||||

| General Government | $471,000 | |||||

| Public Safety | 886,000 | |||||

| Public Works | 650,000 | |||||

| Health and Welfare | 600,000 | |||||

| Miscellaneous | 86,000 | |||||

Table (1)

2.

Entry to record the encumbrances against appropriations:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund: | |||||

| Encumbrances–2020 | $931,000 | ||||

| Encumbrances Outstanding–2020 | $931,000 | ||||

| Encumbrances Ledger: | |||||

| General Government | $58,000 | ||||

| Public Safety | 250,000 | ||||

| Public Works | 392,000 | ||||

| Health and Welfare | 160,000 | ||||

| Miscellaneous | 71,000 | ||||

Table (2)

3.

Entries to record property tax levy:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund: | |||||

| Taxes Receivable–Current | $2,005,000 | ||||

| Allowance for Uncollectible Current Taxes | $65,000 | ||||

| Revenues | 1,940,000 | ||||

| Revenues Ledger: | |||||

| Property Taxes | $1,940,000 | ||||

| Governmental Activities: | |||||

| Taxes Receivable–Current | $2,005,000 | ||||

| Allowance for Uncollectible Current Taxes | $65,000 | ||||

| General Revenues–Property Taxes | 1,940,000 | ||||

Table (3)

4.

Entry to record collection of delinquent taxes:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund and Governmental Activities: | |||||

| Cash | $1,591,000 | ||||

| Taxes Receivable–Delinquent | $132,000 | ||||

| Taxes Receivable–Current | 1,459,000 | ||||

Table (4)

5.

Entry to charge costs to appropriations:

| General Ledger | Subsidiary Ledger | |||||

| Debits | Credits | Debits | Credits | |||

| General Fund: | ||||||

| Expenditures | $1,750,100 | |||||

| Vouchers Payable | $1,750,100 | |||||

| Expenditures Ledger: | ||||||

| General Government | $411,000 | |||||

| Public Safety | 635,000 | |||||

| Public Works | 254,000 | |||||

| Health and Welfare | 439,000 | |||||

| Miscellaneous | 11,100 | |||||

| Governmental Activities: | ||||||

| Expenses–General Government | $422,100 | |||||

| Expenses–Public Safety | 635,000 | |||||

| Expenses–Public Works | 254,000 | |||||

| Expenses–Health and Welfare | 439,000 | |||||

| Vouchers Payable | $1,750,100 | |||||

Table (5)

6.

Entry for the receipt of invoice for the goods ordered in prior year and payment approval:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund: | |||||

| Encumbrances Outstanding–2019 | $14,000 | ||||

| Encumbrances–2019 | $14,000 | ||||

| Encumbrances Ledger–2019: | |||||

| Public Safety | $14,000 | ||||

| Expenditures–2019 | 14,000 | ||||

| Expenditures–2019 | 470 | ||||

| Vouchers Payable | 14,470 | ||||

| Expenditures Ledger–2020: | |||||

| Public Safety | $470 | ||||

| Expenditures Ledger–2019: | |||||

| Public Safety | 14,000 | ||||

| Governmental Activities: | |||||

| Expenses–Public Safety | 14,470 | ||||

| Vouchers Payable | 14,470 | ||||

Table (6)

7.

Entry for the receipt of invoice for the goods ordered in 2020:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund: | |||||

| Encumbrances Outstanding–2020 | $851,200 | ||||

| Encumbrances–2020 | $851,200 | ||||

| Encumbrances Ledger–2020: | |||||

| General Government | $52,200 | ||||

| Public Safety | 240,900 | ||||

| Public Works | 367,000 | ||||

| Health and Welfare | 130,100 | ||||

| Miscellaneous | 71,000 | ||||

| Expenditures–2020 | 850,500 | ||||

| Vouchers Payable | 850,500 | ||||

| Expenditures Ledger–2020: | |||||

| General Government | $52,700 | ||||

| Public Safety | 236,200 | ||||

| Public Works | 360,000 | ||||

| Health and Welfare | 130,600 | ||||

| Miscellaneous | 71,000 | ||||

| Governmental Activities: | |||||

| Expenses–General Government | 123,700 | ||||

| Expenses–Public Safety | 236,200 | ||||

| Expenses–Public Works | 360,000 | ||||

| Expenses–Health and Welfare | 130,600 | ||||

| Vouchers Payable | 850,500 | ||||

Table (7)

8.

Entry to record revenues collected:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund: | |||||

| Cash | $839,000 | ||||

| Revenues | $839,000 | ||||

| Revenues Ledger: | |||||

| Licenses and Permits | $373,000 | ||||

| Intergovernmental Revenue | 400,000 | ||||

| Miscellaneous Revenues | 66,000 | ||||

| Governmental Activities: | |||||

| Cash | |||||

| Program Revenues–General Government–Charges for Services | $373,000 | ||||

| Program Revenues–Public Safety–Operating Grants and Contributions | 400,000 | ||||

| General Revenues–Miscellaneous | 66,000 | ||||

Table (8)

9.

Entry to record the payment of vouchers:

| General Ledger | Subsidiary Ledger | ||||

| Debits | Credits | Debits | Credits | ||

| General Fund and Governmental Activities: | |||||

| Vouchers Payable | $2,505,000 | ||||

| Cash | $2,505,000 | ||||

Table (9)

b.

Prepare the budgetary comparison schedule for the General Fund of the City E for the year ending December 31, 2020.

Explanation of Solution

Budgetary comparison schedule: The schedule that shows the actual revenues, expenditures, outstanding encumbrances in comparison with the budgeted revenues, and appropriations as on a particular date, is referred to as budgetary comparison schedule.

Prepare the budgetary comparison schedule for the General Fund of the City E for the year ending December 31, 2020.

| City E | |||

| General Fund | |||

| Budgetary Comparison Schedule | |||

| For the Year Ended December 31, 2020 | |||

| Budgeted Amounts (Original and Final) | Actual Amounts | Variance with Final Budget Over (Under) | |

| Revenues: | |||

| Taxes | $1,943,000 | $1,940,000 | $(3,000) |

| Licenses and permits | 372,000 | 373,000 | 1,000 |

| Intergovernmental revenue | 397,000 | 400,000 | 3,000 |

| Miscellaneous revenues | 62,000 | 66,000 | 4,000 |

| Total Revenues | 2,774,000 | 2,779,000 | 5,000 |

| Expenditures and Encumbrances: | |||

| General government | $471,000 | 469,500 | (1,500) |

| Public safety | 886,000 | 880,770 | (5,230) |

| Public works | 650,000 | 649,000 | (1,000) |

| Health and welfare | 600,000 | 599,500 | (500) |

| Miscellaneous | 86,000 | 82,100 | (3,900) |

| Total Expenditures | 2,693,000 | 2,680,870 | (12,130) |

| Excess of Revenues over Expenditures | 81,000 | 98,130 | 17,130 |

| Increase in Encumbrances Outstanding | 0 | 65,800 | 65,800 |

| Increase in Fund Balances for Year | 81,000 | 163,930 | 82,930 |

| Fund Balances, January 1, 2020 | 96,900 | 96,900 | 0 |

| Fund Balances, December 31, 2020 | $177,900 | $260,830 | $82,930 |

Table (10)

Want to see more full solutions like this?

Chapter 4 Solutions

Accounting For Governmental & Nonprofit Entities

- Laws can be classified into several categories: criminal law versus civil law, substantive law versus procedural law, public versus private law, and law versus equity. Discuss one of these categories and the distinctions between the two types of laws.arrow_forwardDo fast answer of this accounting questionsarrow_forwardFinancial Accounting Question please answerarrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education