Concept explainers

Videos

Kelly Pitney began her consulting business, Kelly Consulting, on April 1, 2019. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter. During May, Kelly Consulting entered into the following transactions:

| May 3. | Received cash from clients as an advance payment for services to be provided and recorded it as unearned fees, $4,500. |

| 5. | Received cash from clients on account, $2,450. |

| 9. | Paid cash for a newspaper advertisement, $225. |

| 13. | Paid Office Station Co. for part of the debt incurred on April 5, $640. |

| 15. | Provided services on account for the period May 1–15, $9,180. |

| 16. | Paid part-time receptionist for two weeks' salary including the amount owed on April 30, $750. |

| 17. | Received cash from cash clients for fees earned during the period May 1–16, $8,360. |

| Record the following transactions on Page 6 of the journal: | |

| 20. | Purchased supplies on account, $735. |

| 21. | Provided services on account for the period May 16–20, $4,820. |

| 25. | Received cash from cash clients for fees earned for the period May 17–23, $7,900. |

| 27. | Received cash from clients on account, $9,520. |

| 28. | Paid part-time receptionist for two weeks' salary, $750. |

| 30. | Paid telephone bill for May, $260. |

| 31. | Paid electricity bill for May, $810. |

| 31. | Received cash from cash clients for fees earned for the period May 26–31, $3,300. |

| 31. | Provided services on account for the remainder of May, $2,650. |

| 31. | Kelly withdrew $10,500 for personal use. |

Instructions

1. The chart of accounts for Kelly Consulting is shown in Exhibit 9, and the post-closing

2. Post the journal to a ledger of four-column accounts.

3 Prepare an unadjusted trial balance.

4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6).

a. Insurance expired during May is $275.

b. Supplies on hand on May 3 1 are $715.

c. Depreciation of office equipment for May is $330.

d. Accrued receptionist salary on May 31 is $325.

e. Rent expired during May is $1,600.

f. Unearned fees on May 31 are $3,210.

5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet.

6. Journalize and post the

7. Prepare an adjusted trial balance.

8. Prepare an income statement, a statement of owner's equity, and a balance sheet.

9. Prepare and post the closing entries. Record the closing entries on Page 8 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry.

10. Prepare a post-closing trial balance.

1.

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

Ø The title of accounts.

Ø The debit side (Dr) and,

Ø The credit side (Cr).

Adjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Adjusting entries:

An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

Spreadsheet: A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Statement of owners’ equity:

This statement reports the beginning owner’s equity and all the changes, which led to ending owners’ equity. Additional capital, net income from income statement is added to and drawing is deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

Closing entries:

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

To journalize: The transactions of May in a two column journal beginning on page 5.

Explanation of Solution

Journalize the transactions of May in a two column journal beginning on page 5.

| Journal Page 5 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2019 | 3 | Cash | 11 | 4,500 | |

| May | Unearned fees | 23 | 4,500 | ||

| (To record the cash received for the service yet to be provide) | |||||

| 5 | Cash | 11 | 2,450 | ||

| Accounts receivable | 12 | 2,450 | |||

| (To record the cash received from clients) | |||||

| 9 | Miscellaneousexpense | 59 | 225 | ||

| Cash | 11 | 225 | |||

| (To record the payment made for Miscellaneous expense) | |||||

| 13 | Accounts payable | 21 | 640 | ||

| Cash | 11 | 640 | |||

| (To record the payment made to creditors on account) | |||||

| 15 | Accounts receivable | 12 | 9,180 | ||

| Fees earned | 41 | 9,180 | |||

| (To record the revenue earned and billed) | |||||

| 14 | Salary Expense | 51 | 630 | ||

| Salaries payable | 22 | 120 | |||

| Cash | 11 | 750 | |||

| (To record the payment made for salary) | |||||

| Cash | 11 | 8,360 | |||

| 17 | Fees earned | 41 | 8,360 | ||

| (To record the receipt of cash) | |||||

Table (1)

| Journal Page 6 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 2019 | 18 | Supplies | 14 | 735 | |

| May | Accounts payable | 21 | 735 | ||

| (To record the payment made for automobile expense) | |||||

| 21 | Accounts receivable | 12 | 4,820 | ||

| Fees earned | 41 | 4,820 | |||

| (To record the payment of advertising expense) | |||||

| 25 | Cash | 11 | 7,900 | ||

| Fees earned | 41 | 7,900 | |||

| (To record the cash received from client for fees earned) | |||||

| 27 | Cash | 11 | 9,520 | ||

| Accounts receivable | 12 | 9,520 | |||

| (To record the cash received from clients) | |||||

| 28 | Salary expense | 51 | 750 | ||

| Cash | 11 | 750 | |||

| (To record the payment of salary) | |||||

| 30 | Miscellaneous Expense | 59 | 260 | ||

| Cash | 11 | 260 | |||

| (To record the payment of telephone charges) | |||||

| 31 | Miscellaneous Expense | 59 | 810 | ||

| Cash | 11 | 810 | |||

| (To record the payment of electricity charges) | |||||

| 31 | Cash | 11 | 3,300 | ||

| Fees earned | 41 | 3,300 | |||

| (To record the cash received from client for fees earned) | |||||

| 31 | Accounts receivable | 12 | 2,650 | ||

| Fees earned | 41 | 2,650 | |||

| (To record the revenue earned and billed) | |||||

| 31 | K’s Drawing | 32 | 10,500 | ||

| Cash | 11 | 10,500 | |||

| (To record the drawing made for personal use) | |||||

Table (2)

(2)

To record: The balance of each accounts in the appropriate balance column of a four-column account and post them to the ledger.

Explanation of Solution

| Account: Cash Account no.11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 1 | Balance | ✓ | 22,100 | |||

| 3 | 5 | 4,500 | 26,600 | ||||

| 5 | 5 | 2,450 | 29,050 | ||||

| 9 | 5 | 225 | 28,825 | ||||

| 13 | 5 | 640 | 28,185 | ||||

| 16 | 5 | 750 | 27,435 | ||||

| 17 | 5 | 8,360 | 35,795 | ||||

| 25 | 6 | 7,900 | 43,695 | ||||

| 27 | 6 | 9,520 | 53,215 | ||||

| 28 | 6 | 750 | 52,465 | ||||

| 30 | 6 | 260 | 52,205 | ||||

| 31 | 6 | 810 | 51,395 | ||||

| 31 | 6 | 3,300 | 54,695 | ||||

| 31 | 6 | 10,500 | 44,195 | ||||

Table (3)

| Account: Accounts ReceivableAccount no.12 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 1 | Balance | ✓ | 3,400 | |||

| 5 | 5 | 2,450 | 950 | ||||

| 15 | 5 | 9,180 | 10,130 | ||||

| 21 | 6 | 4,820 | 14,950 | ||||

| 27 | 6 | 9,520 | 5,430 | ||||

| 31 | 6 | 2,650 | 8,080 | ||||

Table (4)

| Account: SuppliesAccount no.14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 1 | Balance | ✓ | 1,350 | |||

| 20 | 6 | 735 | 2,085 | ||||

| 30 | Adjusting | 7 | 1,350 | 715 | |||

Table (5)

| Account: Prepaid RentAccount no.15 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 1 | Balance | ✓ | 3,200 | |||

| 31 | Adjusting | 7 | 1,600 | 1,600 | |||

Table (6)

| Account: Prepaid InsuranceAccount no.16 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 1 | Balance | ✓ | 1,500 | |||

| 31 | Adjusting | 7 | 275 | 1,225 | |||

Table (7)

| Account: Office equipmentAccount no.18 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 1 | Balance | ✓ | 14,500 | |||

Table (8)

| Account: Accumulated Depreciation-Office equipmentAccount no.19 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 1 | Balance | ✓ | 330 | |||

| 31 | Adjusting | 7 | 330 | 660 | |||

Table (9)

| Account: Accounts Payable Account no.21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 1 | Balance | ✓ | 800 | |||

| 13 | 5 | 640 | 160 | ||||

| 20 | 6 | 735 | 895 | ||||

Table (10)

| Account: Salaries Payable Account no.22 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 1 | Balance | ✓ | 120 | |||

| 16 | 5 | 120 | |||||

| 31 | Adjusting | 7 | 325 | 325 | |||

Table (11)

| Account: Unearned Fees Account no.23 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 1 | Balance | ✓ | 2,500 | |||

| 3 | 5 | 4,500 | 7,000 | ||||

| 31 | Adjusting | 7 | 3,790 | 3,210 | |||

Table (12)

| Account: K’s Capital Account no.31 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 1 | Balance | ✓ | 42,300 | |||

| 31 | Closing | 8 | 33,425 | 75,725 | |||

| 31 | Closing | 8 | 10,500 | 65,225 | |||

Table (13)

| Account: K’s DrawingAccount no.32 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 31 | 6 | 10,500 | 10,500 | |||

| 31 | Closing | 8 | 10,500 | ||||

Table (14)

| Account: Fees earned Account no.41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 15 | 5 | 9,180 | 9,180 | |||

| 17 | 5 | 8,360 | 17,540 | ||||

| 21 | 6 | 4,820 | 22,360 | ||||

| 25 | 6 | 7,900 | 30,260 | ||||

| 31 | 6 | 3,300 | 33,560 | ||||

| 31 | 6 | 2,650 | 36,210 | ||||

| 31 | Adjusting | 7 | 3,790 | 40,000 | |||

| 31 | Closing | 8 | 40,000 | ||||

Table (15)

| Account: Salary expense Account no.51 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 16 | 5 | 630 | 630 | |||

| 28 | 6 | 750 | 1,380 | ||||

| 31 | Adjusting | 7 | 325 | 1,705 | |||

| 31 | Closing | 8 | 1,705 | ||||

Table (16)

| Account: Rent expense Account no.52 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 31 | Adjusting | 7 | 1,600 | 1,600 | ||

| 31 | Closing | 8 | 1,600 | ||||

Table (17)

| Account: Supplies expense Account no.53 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 31 | Adjusting | 7 | 1,370 | 1,370 | ||

| 31 | Closing | 8 | 1,370 | ||||

Table (18)

| Account: Depreciation expense Account no.54 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 31 | Adjusting | 7 | 330 | 330 | ||

| 31 | Closing | 8 | 330 | ||||

Table (19)

| Account: Insurance expense Account no.54 | |||||||

| Date | Item | PostRef |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 31 | Adjusting | 7 | 275 | 275 | ||

| 31 | Closing | 8 | 275 | ||||

Table (20)

| Account: Miscellaneous expense Account no.59 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2019 | |||||||

| May | 9 | 5 | 225 | 225 | |||

| 30 | 6 | 260 | 485 | ||||

| 31 | 6 | 810 | 1,295 | ||||

| 31 | Closing | 8 | 1,295 | ||||

Table (21)

(3)

To prepare: The unadjusted trial balance of Consulting Kat May, 31.

Explanation of Solution

Prepare an unadjusted trial balance of Consulting K for the month ended May, 31 as follows:

|

K Consulting Unadjusted Trial Balance May 31, 2019 | |||

| Particulars |

Account No. | Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 2,085 | |

| Prepaid rent | 15 | 3,200 | |

| Prepaid insurance | 16 | 1,500 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated depreciation-Office equipment | 19 | 330 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 0 | |

| Unearned fees | 23 | 7,000 | |

| K’s Capital | 31 | 42,300 | |

| K’s Drawing | 32 | 10,500 | |

| Fees earned | 41 | 36,210 | |

| Salary expense | 51 | 1,380 | |

| Rent expense | 52 | 0 | |

| Supplies expense | 53 | 0 | |

| Depreciation expense | 54 | 0 | |

| Insurance expense | 55 | 0 | |

| Miscellaneous expense | 59 | 1,295 | |

| Total | 86,735 | 86,735 | |

Table (22)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $86,735.

(4)

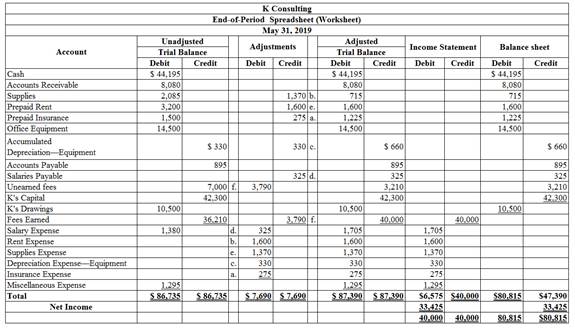

To enter: The unadjusted trial balance on an end-of-period spreadsheet.

Explanation of Solution

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (23)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

(5)

To Journalize: Theadjusting entries of Consulting K for May 31.

Explanation of Solution

The adjusting entries of ConsultingK for May 31, 2019 are as follows:

| Date | Accounts title and explanation | Post Ref. |

Debit ($) |

Credit ($) | |

| 2019 | Insurance expense | 55 | 275 | ||

| May | 31 | Prepaid insurance | 16 | 275 | |

| (To record the insurance expense for May ) | |||||

| 31 | Supplies expense(1) | 53 | 1,370 | ||

| Supplies | 14 | 1,370 | |||

| (To record the supplies expense) | |||||

| 31 | Depreciation expense | 54 | 330 | ||

| Accumulated Depreciation | 19 | 330 | |||

| (To record the depreciation and the accumulated depreciation) | |||||

| 31 | Salaries expense | 51 | 325 | ||

| Salaries payable | 22 | 325 | |||

| (To record the accrued salaries payable) | |||||

| 31 | Rent expense | 52 | 1,600 | ||

| Prepaid rent | 15 | 1,600 | |||

| (To record the rent expense for May ) | |||||

| 31 | Unearned fees(2) | 23 | 3,790 | ||

| Fees earned | 41 | 3,790 | |||

| (To record the receipt of unearned fees) | |||||

Table (24)

Working notes:

(1)

(2)

(6)

To prepare: An adjusted trial balance of Consulting K for May 31, 2019.

Explanation of Solution

An adjusted trial balanceof Consulting K for May 31, 2019 is prepared as follows:

|

K Consulting Adjusted Trial Balance May 31, 2019 | |||

| Particulars |

Account No. | Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 715 | |

| Prepaid insurance | 16 | 1,600 | |

| Prepaid rent | 15 | 1,225 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated Depreciation-Office equipment | 19 | 660 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 325 | |

| Unearned fees | 23 | 3,210 | |

| J’s Capital | 31 | 42,300 | |

| J’s Drawing | 32 | 10,500 | |

| Fees earned | 41 | 40,000 | |

| Salary expense | 51 | 1,705 | |

| Rent expense | 52 | 1,600 | |

| Supplies Expense | 53 | 1,370 | |

| Depreciation expense | 54 | 330 | |

| Insurance expense | 55 | 275 | |

| Miscellaneous expense | 59 | 1,295 | |

| Total | 87,390 | 87,390 | |

Table (25)

Conclusion:

The debit column and credit column of the adjusted trial balance are agreed, both having balance of $87,390.

(7)

To Prepare: An income statement for the year ended May 31, 2019.

Explanation of Solution

An income statement for the year ended May 31, 2019 is as follows:

| K Consulting | ||

| Income Statement | ||

| For the year ended May 31, 2019 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Fees Earned | 40,000 | |

| Expenses: | ||

| Salaries Expense | 1,705 | |

| Rent Expense | 1,600 | |

| Supplies Expense | 1,370 | |

| Depreciation Expense- Building | 330 | |

| Insurance Expense | 275 | |

| Miscellaneous Expense | 1,295 | |

| Total Expenses | 6,575 | |

| Net Income | $33,425 | |

Table (26)

Hence, the net income of G Consulting for the year ended May 31, 2019 is $33,425.

(8)

To Journalize: The closing entries for KConsulting.

Explanation of Solution

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| May 31, 2019 | Fees Earned | 41 | 40,000 | |

| Salary Expense | 51 | 1,705 | ||

| Rent Expense | 52 | 1,600 | ||

| Supplies Expense | 53 | 1,370 | ||

| Depreciation Expense | 54 | 330 | ||

| Insurance Expense | 55 | 275 | ||

| Miscellaneous Expense | 59 | 1,295 | ||

| K, Capital | 31 | 33,425 | ||

| (To close the revenues and expenses account. Then the balance amount are transferred to owners’ capital account) | ||||

| May 31 | K’s Capital | 31 | 10,500 | |

| K’ Drawing | 32 | 10,500 | ||

| (To Close the capital and drawings account) | ||||

Table (29)

Explanation:

- A Service fee earned is revenue account. Since the amount of revenue is closed and transferred to K’s capital account. Here, K Consulting earned an income of $40,000. Therefore, it is debited.

- Salaries Expense, Rent Expense, Insurance Expense, Utilities Expense, Supplies Expense, Depreciation Expense, Advertising Expense, JU Capital,and Miscellaneous Expense are expense accounts. Since the amount of expenses are closed to Income Summary account. Therefore, it is credited.

- Owner’s capital is a component of owner’s equity. Thus, owners ‘equity is debited since the capital is decreased on owners’ drawings.

- Owner’s drawings are a component of owner’s equity. It is credited because the balance of owners’ drawing account is transferred to owners ‘capital account.

(9)

To Journalize: The closing entries for KConsulting.

Explanation of Solution

Prepare apost–closing trial balance of KConsulting for the month ended May 31, 2019 as follows:

|

Consulting K Post-closing Trial Balance May, 31, 2019 | |||

| Particulars | Account Number | Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 715 | |

| Prepaid rent | 15 | 1,600 | |

| Prepaid insurance | 16 | 1,225 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated depreciation –Office Equipment | 19 | 660 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 325 | |

| Unearned rent | 23 | 3,210 | |

| K’s Capital | 31 | 65,225 | |

| Total | 70,315 | 70,315 | |

Table (5)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $70,315.

Want to see more full solutions like this?

Chapter 4 Solutions

Bundle: Accounting, 27th + Cengagenowv2, 2 Terms Printed Access Card

- Blue Company, an architectural firm, has a bookkeeper who maintains a cash receipts and disbursements journal. At the end of the year (2019), the company hires you to convert the cash receipts and disbursements into accrual basis revenues and expenses. The total cash receipts are summarized as follows. The accounts receivable from customers at the end of the year are 120,000. You note that the accounts receivable at the beginning of the year were 190,000. The cash sales included 30,000 of prepayments for services to be provided over the period January 1, 2019, through December 31, 2021. a. Compute the companys accrual basis gross income for 2019. b. Would you recommend that Blue use the cash method or the accrual method? Why? c. The company does not maintain an allowance for uncollectible accounts. Would you recommend that such an allowance be established for tax purposes? Explain.arrow_forwardSammi started her business on 1 January 2021 called Trendy. You are required to prepare the GENERAL JOURNAL for the following transactions of Trendy for the first month of operations. Jan 01Sammi invested RM50, 000 cash into the business.Jan 02Trendy purchased used motor vehicle for RM20,000.Jan 08Trendy paid rent for RM4, 000.Jan 08Trendy completed work for a client and immediately received RM15, 000.Jan 12Sammi signed a RM50,000 small business loans with CIMB Bank under Trendy’s name.Jan 15Ideal Homes renovated and installed fixtures and fittings at a cost of RM3, 000. Trendy will pay the bill at a later date.Jan 15Trendy paid RM1, 000 cash for advertisement in a local magazine.Jan 28Trendy completed work for another client on credit and invoiced the client RM5, 000. The client is allowed to settle the bill within 30 days.Jan 30Trendy paid Ideal Homes that installed the fixtures and fittings earlier.Jan 30Trendy paid RM150 for usage of electricity for the month.arrow_forwardSammi started her business on 1 January 2021 called Trendy. You are required to prepare the GENERAL JOURNAL for the following transactions of Trendy for the first month of operations. Narratives are not required for each journal entry. Jan 01Sammi invested RM50, 000 cash into the business.Jan 02Trendy purchased used motor vehicle for RM20,000.Jan 08Trendy paid rent for RM4, 000.Jan 08Trendy completed work for a client and immediately received RM15, 000.Jan 12Sammi signed a RM50,000 small business loans with CIMB Bank under Trendy’s name.Jan 15Ideal Homes renovated and installed fixtures and fittings at a cost of RM3, 000. Trendy will pay the bill at a later date.Jan 15Trendy paid RM1, 000 cash for advertisement in a local magazine.Jan 28Trendy completed work for another client on credit and invoiced the client RM5, 000. The client is allowed to settle the bill within 30 days.Jan 30Trendy paid Ideal Homes that installed the fixtures and fittings earlier.Jan 30Trendy paid RM150 for usage…arrow_forward

- The following transactions occurred during the month of July 2021. July 1 Paid employee salaries, $2,700 for June. Sharon pays her employees’ accrued salaries on the first day of each calendar month. July 1 Paid office rent for the month of July, $2,300. July 8 Received $7,200 cash from a client on account. July 9 Purchased office supplies on credit, $2,000 14 Paid $3,500 of the accounts payable. July 15 Invoiced customers for accounting services performed, $12,300. July 25 Sharon withdrew capital of $2,250 July 31 Paid $4,200 for a one-year insurance policy. a) Prepare the cash at bank ledger account as at 31 July 2021.arrow_forwardThe first project for the semester will involve the following items to turn in: 1) Journal entries for financial transactions I will provide you. 2) An adjusted trial balance. 3) An Income statement. 1) On December 1 of 2019 Harold Hammer deposited $ 15,100 in a bank account in the name of Huaning Corporation in exchange for shares of common stock in the corporation. 2) On December 1 of 2019 Huaning Corporation purchased supplies on account for $ 226 . 3) On December 4 of 2019 Huaning Corporation received cash of $ 384 for product sold to the customer. 4) On December 5 of 2019 Huaning Corporation paid the vendor for the December 1st purchase of supplies. 5) On December 6 of 2019 Huaning Corporation purchases supplies on account for $ 469 .6) On December 8 of 2019 Huaning Corporation sells product for $ 445 on account to a customer.7) On December 9 of 2019 Huaning Corporation sells product for $ 462 on account to a customer. 8) On December 10 of 2019 Huaning Corporation paid, in…arrow_forwardThe transactions below needs to be journalized. Two accrual transactions and two deferral transactions. Please be sure to include corresponding dates and transaction amount information. I need help with this please and thank you. Please include an explanation of what was done. Accrual Transactions - May 1st, 2021 Paid rent on my office space and paid the landscaping company (revenue: $15,000 expenses: $2,000) Bonuses paid out for my employees (revenue: $15,000 expenses: $800) Deferral Transactions - January 1st 2021 Paid $600 for a year of insurance Equipment Depreciates by $150 every montharrow_forward

- . Assume that a lawyer bills her clients $15,000 on June 30, for services rendered during June. The lawyer collects $8,500 of the billings during July and the remainder in August. Under the accrual basis of accounting, when would the lawyer record the revenue? A. June, $15,000; July, $0; and August, $0 B. June, $0; July $6,500; and August, $8,500 C. June, $8,500; July $6,500; and August, $0 D. June, $0; July, $8,500; and August, $6,500arrow_forwardSammi started her business on 1 January 2021 called Trendy. You are required to prepare the GENERAL JOURNAL for the following transactions of Trendy for the first month of operations. Narratives are not required for each journal entry. Jan 01 Sammi invested RM50, 000 cash into the business.Jan 02 Trendy purchased used motor vehicle for RM20,000.Jan 08 Trendy paid rent for RM4, 000.Jan 08 Trendy completed work for a client and immediately received RM15, 000.Jan 12 Sammi signed a RM50,000 small business loans with CIMB Bank under Trendy’s name.Jan 15 Ideal Homes renovated and installed fixtures and fittings at a cost of RM3, 000. Trendy will pay the bill at a later date.Jan 15 Trendy paid RM1, 000 cash for advertisement in a local magazine.Jan 28 Trendy completed work for another client on credit and invoiced the client RM5, 000. The client is allowed to settle the bill within 30 days.Jan 30 Trendy paid Ideal Homes that installed the fixtures and fittings earlier.Jan 30 Trendy paid…arrow_forwardPrepare journal entries to record the following transactions for the month of November: A. on first day of the month, issued common stock for cash, $20,000 B. on third day of month, purchased equipment for cash, $10,500 C. on tenth day of month, received cash for accounting services, $14,250 D. on fifteenth day of month, paid miscellaneous expenses, $3,200 E. on last day of month, paid employee salaries, $8,600arrow_forward

- On October 1, 2019, Jay Pryor established an interior decorating business, Pioneer Designs. During the month, Jay completed the following transactions related to the business: Oct. 1. Jay transferred cash from a personal bank account to an account to be used for the business, 18,000. 4.Paid rent for period of October 4 to end of month, 3,000. 10.Purchased a used truck for 23,750, paying 3,750 cash and giving a note payable for the remainder. 13.Purchased equipment on account, 10,500. 14.Purchased supplies for cash, 2,100. 15.Paid annual premiums on property and casualty insurance, 3,600. 15.Received cash for job completed, 8,950. Enter the following transactions on Page 2 of the two-column journal: 21.Paid creditor a portion of the amount owed for equipment purchased on October 13, 2,000. 24.Recorded jobs completed on account and sent invoices to customers, 14,150. 26.Received an invoice for truck expenses, to be paid in November, 700. 27.Paid utilities expense, 2,240. 27.Paid miscellaneous expenses, 1,100. Oct. 29. Received cash from customers on account, 7,600. 30.Paid wages of employees, 4,800. 31.Withdrew cash for personal use, 3,500. Instructions 1. Journalize each transaction in a two-column journal beginning on Page 1, referring to the following chart of accounts in selecting the accounts to be debited and credited. (Do not insert the account numbers in the journal at this time.) Journal entry explanations may be omitted. 2. Post the journal to a ledger of four-column accounts, inserting appropriate posting references as each item is posted. Extend the balances to the appropriate balance columns after each transaction is posted. 3. Prepare an unadjusted trial balance for Pioneer Designs as of October 31, 2019. 4. Determine the excess of revenues over expenses for October. 5. Can you think of any reason why the amount determined in (4) might not be the net income for October?arrow_forwardInner Resources Company started its business on April 1, 2019. The following transactions occurred during the month of April. Prepare the journal entries in the journal on Page 1. A. The owners invested $8,500 from their personal account to the business account. B. Paid rent $650 with check #101. C. Initiated a petty cash fund $550 check #102. D. Received $750 cash for services rendered. E. Purchased office supplies for $180 with check #103. F. Purchased computer equipment $8,500, paid $1,600 with check #104 and will pay the remainder in 30 days. G. Received $1,200 cash for services rendered. H. Paid wages $560, check #105. I. Petty cash reimbursement office supplies $200, Maintenance Expense $140, Miscellaneous Expense $65. Cash on Hand $93. Check #106. J. Increased Petty Cash by $100, check #107.arrow_forwardWhat Do You Think? You work as an accounting clerk. You have received the following information supplied by a client, S. Winston, from the clients bank statement, the clients tax returns, and a variety of other July documents. The client wants you to prepare an income statement, a statement of owners equity, and a balance sheet for the month of July for Winston Company.arrow_forward

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT

Individual Income TaxesAccountingISBN:9780357109731Author:HoffmanPublisher:CENGAGE LEARNING - CONSIGNMENT