Concept explainers

Videos

From Recording Transactions to Preparing Accrual and Deferral Adjustments and Reporting Results on the

RunHeavy Corporation (RHC) is a corporation that manages a local rock band. RHC was formed with an investment of $ 10,000 cash, paid in by the leader of the band on January 3 in exchange for common stock. On January 4, RHC purchased music equipment by paying $2,000 cash and signing an $8,000 promissory note payable in three years. On January 5, RHC booked the band for six concert events, at a price of $2,500 each. Of the six events, four were completed between January 10 and 20. On January 22, cash was collected for three of the four events. The other two bookings were for February concerts, but on January 24, RHC collected half of the $2,500 fee for one of them. On January 27, RHC paid $3,140 cash for the band’s travel-related costs. On January 28, RHC paid its band members a total of $2,400 cash for salaries and wages for the first three events. As of January 31, the band members hadn’t yet been paid wages for the fourth event completed in January, but they would be paid in February at the same rate as for the first three events. As of January 31, RHC has not yet recorded the $ 100 of monthly depreciation on the equipment. Also, RHC has not yet paid or recorded the $60 interest owed on the promissory note at January 31, RHC is subject to a 15% tax rate on the company’s income before lax.

Required:

- 1. Prepare

journal entries to record the transactions and adjustments needed on each of the dates indicated above. - 2.

Post the journal entries from requirement 1 to T-accounts, calculate ending balances, and prepare an adjustedtrial balance . - 3. Prepare a classified balance sheet and income statement as of and for the month ended January 31.

1.

To prepare: The journal entries for the given transactions and to prepare the adjusting entries that are needed on each of the dates.

Explanation of Solution

Journal:

Journal is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Adjusting entries:

Adjusting entries refers to the entries that are made at the end of an accounting period in accordance with revenue recognition principle, and expenses recognition principle. The purpose of adjusting entries is to adjust the revenue, and the expenses during the period in which they actually occurs.

Prepare the journal entries:

Journal entry for issuance of common stock:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January, 3 | Cash (A+) | 10,000 | |

| Common stock (SE+) | 10,000 | ||

| (To record the issuance of common stock to investors) |

Table (1)

- Cash is an asset. There is an increase in the asset. Hence, debit cash account with $10,000.

- Common stock is a component of stock holders’ equity. There is an increase in the common stock which increases the stock holders’ equity. Hence, credit common stock with $10,000.

Journal entry for purchase of equipment:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January, 4 | Equipment (A+) | 10,000 | |

| Notes payable (L+) | 8,000 | ||

| Cash (A–) | 2,000 | ||

| (To record the purchase of equipment partly for cash and partly by signing a note ) |

Table (2)

- Equipment is an asset. There is an increase in the asset. Hence, debit equipment with $10,000.

- Notes payable is a liability. There is an increase in the liability. Hence, credit notes payable with $8,000.

- Cash is an asset. There is a decrease in the asset. Hence, credit cash account with $2,000.

January ,5:

RHC booked the band for six concert events. As the booking represents only the mere exchange of promises, there is no need of recording the journal entry for that transaction. Hence, no entry is recorded.

Journal entry for providing services on account:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January, 10-20 |

Accounts receivable (A+) |

10,000 |

|

| Service revenue(R+) (SE+) | 10,000 | ||

| (To record the service made on account) |

Table (3)

- Accounts receivable is an asset. There is an increase in the asset. Hence, debit accounts receivable with $10,000.

- Service revenue is a revenue account which is a component of stock holders’ equity. There is an increase in the revenue account which increases the stockholders’ equity. Hence credit stockholders’ equity with $10,000.

Journal entry for receiving cash for the service provided:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January, 22 | Cash (A+) | 7,500 | |

| Accounts receivable (A-) | 7,500 | ||

| (To record the cash receipt for the service performed on account) |

Table (4)

- Cash is an asset. There is an increase in the asset. Hence, debit cash account with $7,500.

- Accounts receivable is an asset. There is a decrease in the asset. Hence, credit accounts receivable with $7,500.

Working note:

Journal entry for unearned revenue:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January, 24 | Cash (A+) | 1,250 | |

| Unearned revenue (L+) | 1,250 | ||

| (To record the cash receipt for the service performed on account) |

Table (5)

- Cash is an asset. There is an increase in the asset. Hence, debit cash account with $1,250.

- Unearned revenue is a liability. There is an increase in the liability. Hence, credit unearned revenue with $1,250.

Working note:

Journal entry for travel expenses:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January, 27 | Travel expense (E+) (SE-) | 3,140 | |

| Cash (A-) | 3,140 | ||

| (To record the payment made for travel expense) |

Table (6)

- Travel expense is an expense account which is a component of stock holders’ equity. There is an increase in the expense account which decreases the stockholders’ equity. Hence, debit travel expense with $3,140.

- Cash is an asset. There is a decrease in the asset. Hence, credit cash account with $3,140.

Journal entry for salaries and wages expense:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January, 28 | Salaries and wages expense (E+) (SE-) | 2,400 | |

| Cash (A-) | 2,400 | ||

| (To record the salaries and wages expense) |

Table (7)

- Salaries and wages expense is an expense account which is a component of stock holders’ equity. There is an increase in the expense account which decreases the stockholders’ equity. Hence, debit salaries and wages expense with $2,400.

- Cash is an asset. There is a decrease in the asset. Hence, credit cash account with $2,400.

Adjusting entry for salaries and wages payable:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January, 31 | Salaries and wages expense (E+) (SE-) | 800 | |

| Salaries and wages payable (L+) | 800 | ||

| (To record the adjusting entry salaries and wages expense) |

Table (8)

- Salaries and wages expense is an expense account which is a component of stock holders’ equity. There is an increase in the expense account which decreases the stockholders’ equity. Hence, debit salaries and wages expense with $800.

- Salaries and wages payable is a liability. There is an increase in the liability. Hence, credit, salaries and wages payable with $800.

Working note:

Adjusting entry for accumulated depreciation on equipment:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January, 31 | Depreciation expense (E+) (SE-) | 100 | |

| Accumulated depreciation-Equipment (xA+) (A-) | 100 | ||

| (To record the adjusting entry salaries and accumulated depreciation) |

Table (9)

- Depreciation expense is an expense account which is a component of stockholders’ equity. There is an increase in the expense account which decreases the stockholders’ equity. Hence, debit depreciation expense with $100.

- Accumulated depreciation is a contra-asset. There is an increase in the contra-asset which decreases the asset account. Hence, credit accumulated depreciation with $100.

Adjusting entry for interest expense:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January, 31 | Interest expense (E+) (SE-) | 60 | |

| Interest payable (L+) | 60 | ||

| (To record the adjusting entry for interest expense) |

Table (10)

- Interest expense is an expense account which is a component of stock holders’ equity. There is an increase in the expense account which decreases the stockholders’ equity. Hence, debit interest expense with $60.

- Interest payable is a liability. There is an increase in the liability. Hence, credit, interest payable with $60.

Adjusting entry for income tax expense:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| January, 31 | Income tax expense (E+) (SE-)(2) | 525 | |

| Income tax payable (L+) | 525 | ||

| (To record the adjusting entry for income tax expense) |

Table (11)

- Income tax expense is an expense account which is a component of stock holders’ equity. There is an increase in the expense account which decreases the stockholders’ equity. Hence, debit interest expense with $60.

- Income tax payable is a liability. There is an increase in the liability. Hence, credit, interest payable with $60.

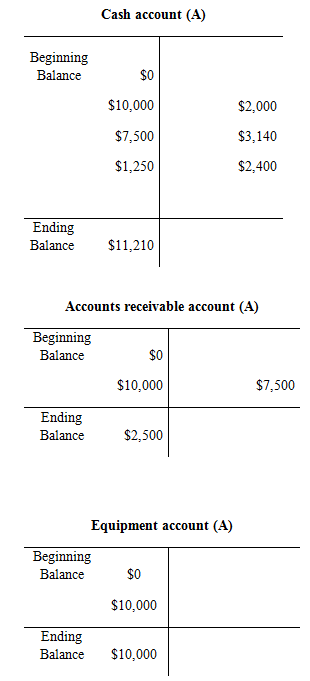

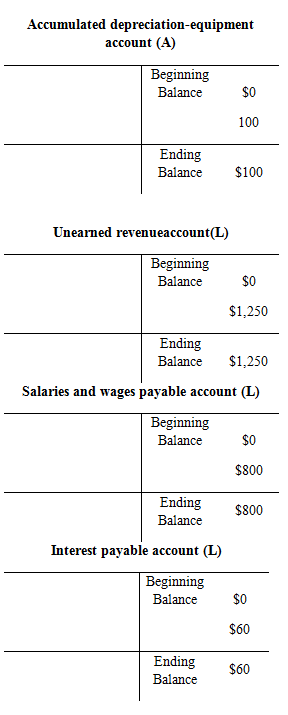

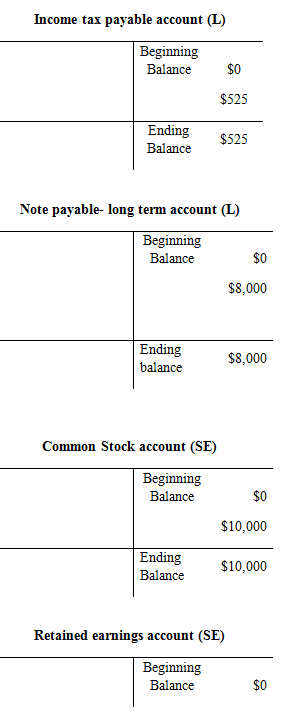

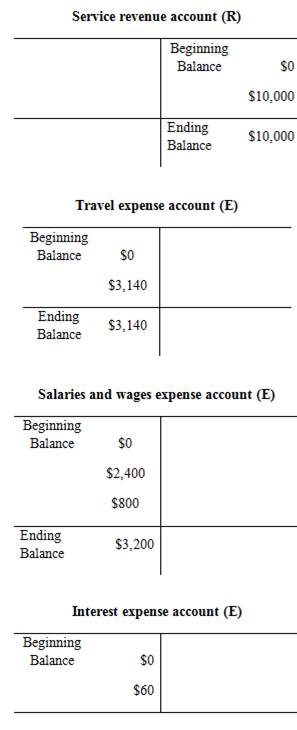

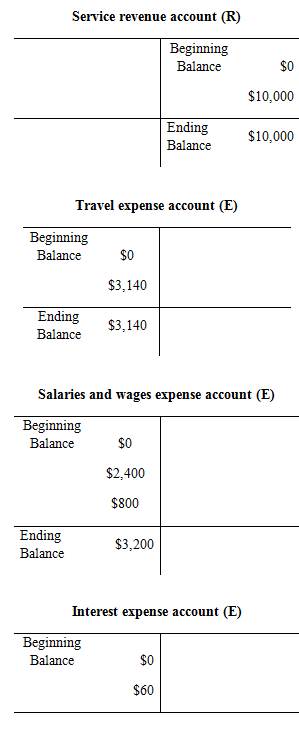

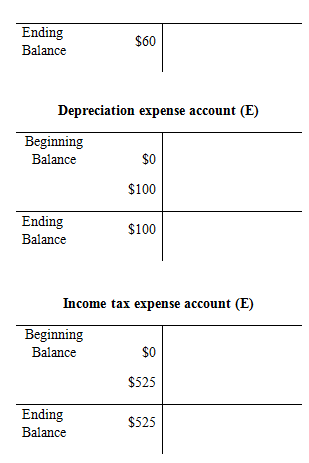

2.

To prepare: The T-Accounts for the journal entries to calculate the ending balance and prepare an adjusted trial balance.

Explanation of Solution

T-account:

T-account is the form of the ledger account, where the journal entries are posted to this account. It is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.

The components of the T-account are as follows:

- The title of the account

- The left or debit side

- The right or credit side

Prepare the T-account:

Trial balance:

Trial balance is the summary of accounts, and their debit and credit balances at a given time. It is usually prepared at end of the accounting period. Debit balances are listed in left column and credit balances are listed in right column. The totals of debit and credit column should be equal. Trial balance is useful in the preparation of the financial statements.

Prepare the adjusted trial balance:

| Corporation RH | ||

| Adjusted Trial Balance | ||

| As on 31st January | ||

| Particulars | Debits ($) | Credits ($) |

| Cash | 11,210 | |

| Accounts Receivable | 2,500 | |

| Equipment | 10,000 | |

| Accumulated Depreciation-equipment | 100 | |

| Unearned Revenue | 1,250 | |

| Salaries and Wages payable | 800 | |

| Interest Payable | 60 | |

| Income Tax Payable | 525 | |

| Note Payable (long–term) | 8,000 | |

| Common Stock | 10,000 | |

| Retained Earnings | 0 | |

| Service Revenue | 10,000 | |

| Travel Expense | 3,140 | |

| Salaries and Wages expense | 3,200 | |

| Interest Expense | 60 | |

| Depreciation Expense | 100 | |

| Income Tax Expense | 525 | |

| Total | 30,735 | 30,735 |

Table (12)

The debit column and credit column of the adjusted trial balance are agreed, both having balance of $30,735.

3.

To prepare: An income statement as on 31st January, and classified balance sheet.

Explanation of Solution

Income statement:

Income statement is a financial statement that shows the net income or net loss by deducting the expenses from the revenues.

Prepare the income statement as on 31st January.

| Corporation RH | ||

| Income Statement | ||

| For the Month Ended January 31 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Service Revenue | 10,000 | |

| Total Revenue | 10,000 | |

| Expenses: | ||

| Salaries and Wages expense | 3,200 | |

| Travel Expenses | 3,140 | |

| Depreciation Expense | 100 | |

| Interest Expense | 60 | |

| Income Tax Expense(2) | 525 | |

| Total Expenses | 7,025 | |

| Net income | 2,975 | |

Table (13)

Working note:

Calculate the income before income tax:

Calculate the income tax expense:

Thus the income statement of Corporation R is prepared and it shows the net income of $2,975.

Classified balance sheet:

This is the financial statement of a company which shows the grouping of similar assets and liabilities under subheadings.

Prepare the classified balance sheet as on 31st January:

| Corporation RH | ||

| Balance Sheet | ||

| As on 31st January | ||

| Particulars | Amount ($) | Amount ($) |

| Assets | ||

| Current Assets: | ||

| Cash | 11,210 | |

| Accounts Receivable | 2,500 | |

| Total Current Assets | 13,710 | |

| Non-Current assets: | ||

| Equipment | 10,000 | |

| Accumulated Depreciation–Equipment | (100) | |

| Equipment, net of Accumulated Depreciation | 9,900 | |

| TOTAL ASSETS | $23,610 | |

| Liabilities and stockholders’ equity | ||

| Current Liabilities: | ||

| Unearned Revenue | 1,250 | |

| Salaries and Wages Payable | 800 | |

| Interest Payable | 60 | |

| Income Tax Payable | 525 | |

| Total Current Liabilities | 2,635 | |

| Non-Current liabilities: | ||

| Note Payable (long–term) | 8,000 | |

| Total Liabilities | 10,635 | |

| Stockholders’ Equity: | ||

| Common Stock | 10,000 | |

| Retained Earnings | 2,975 | |

| Total Stockholders’ Equity | 12,975 | |

| TOTAL LIABILITIES & STOCKHOLDERS’ EQUITY | 23,610 | |

Table (14)

Thus, the classified balance sheet of Corporation RHC is prepared and the total assets and liabilities showing equal balance of $23,610.

Want to see more full solutions like this?

Chapter 4 Solutions

FUNDAMENTALS OF FINANCIAL ACCOUNTING

- Bennett Griffin and Chula Garza organized Cole Valley Book Store as a corporation; each contributed $71,600 cash to start the business and received 5,800 shares of common stock. The store completed its first year of operations on December 31, current year. On that date, the following financial items for the year were determined: December 31, current year, cash on hand and in the bank, $70,150; December 31, current year, amounts due from customers from sales of books, $41,000; unused portion of store and office equipment, $78,000; December 31, current year, amounts owed to publishers for books purchased, $13,800; one-year note payable to a local bank for $3,200. No dividends were declared or paid to the stockholders during the year. Required: 1. Complete the following balance sheet as of the end of the current year. Some information has been given below. 2. What was the amount of net income for the year? (Hint: Use the retained earnings equation [Beginning Retained Earnings + Net Income…arrow_forwardBennett Griffin and Chula Garza organized Cole Valley Book Store as a corporation; each contributed $71,600 cash to start the business and received 4,700 shares of common stock. The store completed its first year of operations on December 31, current year. On that date, the following financial items for the year were determined: December 31, current year, cash on hand and in the bank, $69,650; December 31, current year, amounts due from customers from sales of books, $39,500; unused portion of store and office equipment, $73,500: December 31, current year, amounts owed to publishers for books purchased, $12,600; one-year note payable to a local bank for $3,800. No dividends were declared or paid to the stockholders during the year. Required: 1. Complete the following balance sheet as of the end of the current year. Some information has been given below. 2. What was the amount of net income for the year? (Hint: Use the retained earnings equation (Beginning Retained Earnings + Net Income…arrow_forwardThe following information is available about the company. Provide a five-step way to record this information so that it can be used by managers: 1. Investment of the company's shareholders in the amount of 1000 monetary units to establish a company and deposit this amount in a current account in a bank. 2. Purchase of land for 1,500 currency units, half of which will be paid in cash and the rest next year. 3- Purchasing equipment in the amount of 140 monetary units in cash. 4. Buy 500 currency units (60% cash and 40% credit). 5. Receive a loan in the amount of 90 monetary units from the bank and deposit it in the current account.arrow_forward

- Georgia Corporation incorporated on September 2, current year. The company engaged in the following transactions during its first month of operations. Sept. 2 Issued capital stock in exchange for $1,17e,e00 cash. Sept. 4 Purchased land and a building for $1,080,000. The value of the land was $240,eee, and the value of the building was $840,000. The company paid $120,000 cash and issued a note payable for the balance. Sept. 12 Purchased office supplies for $600 on account. The supplies will last for several months. Sept. 19 Billed clients $216,000 on account. Sept. 29 Recorded and paid salary expense of $72, e00. Sept. 30 Received $132,0ee from clients billed on September 19. A partial list of the account titles used by the company includes the following. Cash Accounts Receivable Office Supplies Land Building Notes Payable Accounts Payable Capital Stock Client Revenue Salary Expense a. Prepare journal entries for the above transactions. b. Post each entry to the appropriate ledger…arrow_forwardKen Young and Kim Sherwood organized Reader Direct as a corporation; each contributed $52,675 cash to start the business and received 4,300 shares. The store completed its first year of operations on December 31, 2020. On that date, the following financial items for the year were determined: cash on hand and in the bank, $49,150, amounts due from customers from sales of books, $28,850, property and equipment, $54,750, amounts owed to publishers for books purchased, $8,900; one-year note payable to a local bank for $4,200. No dividends were declared or paid to the shareholders during the year. Required: 1. Complete the balance sheet at December 31, 2020: Total assets Assets READER DIRECT Balance Sheet At December 31, 2020 $ Total liabilities Liabilities Shareholders' equity Total shareholders equity 0 Total llabilities & shareholders' equity $ 0 0arrow_forwardGlenn Grimes is the founder and president of Heartland Construction, a real estate development venture. The business transactions during February while the company was being organized are listed as follows. Feb. 1 Grimes and several others invested $600,000 cash in the business in exchange for 30,000 shares of capital stock. Feb. 10 The company purchased office facilities for $277,500, of which $92,500 was applicable to the land and $185,000 to the building. A cash payment of $55,500 was made and a note payable was issued for the balance of the purchase price. Feb. 16 Computer equipment was purchased from PCWorld for $15,300 cash. Feb. 18 Office furnishings were purchased from Hi-Way Furnishings at a cost of $9,450. A $945 cash payment was made at the time of purchase, and an agreement was made to pay the remaining balance in two equal installments due March 1 and April 1. Hi-Way Furnishings did not require that Heartland sign a promissory note. Feb. 22 Office supplies were purchased…arrow_forward

- In June 2021, Wanda Fonda organized a corporation to provide drone photography services. The company, called Drone Queen Inc., began operations immediately. Transactions during the month of June were as follows: June 1 The corporation issued 60,000 shares of capital stock to Wanda Fonda in exchange for $60,000 cash. Purchased a plane from Utility Aircraft for $220,000. Made a $40,000 cash down payment and issued a note payable for the remaining balance. June 2 June 4 Paid Piarco Airport $2,500 to rent office and hangar space for the month. June 15 Billed customers $8,320 for aerial photographs taken during the first half of June. June 15 Paid $5,880 in salaries earned by employees during the first half of June. Paid Henry's Hangar $1,890 for maintenance and repair services on the company plane. June 18 June 25 Collected $4,910 of the amounts billed to customers on June 15. June 30 Billed customers $16,450 for aerial photographs taken during the second half of the month. June 30 Paid…arrow_forwardIn June 2021, Wanda Fonda organized a corporation to provide drone photography services. The company, called Drone Queen Inc., began operations immediately. Transactions during the month of June were as follows: June 1 The corporation issued 60,000 shares of capital stock to Wanda Fonda in exchange for $60,000 cash. Purchased a plane from Utility Aircraft for $220,000. Made a $40,000 cash down payment and issued a note payable for the remaining balance. June 2 June 4 Paid Piarco Airport $2,500 to rent office and hangar space for the month. June 15 Billed customers $8,320 for aerial photographs taken during the first half of June. June 15 Paid $5,880 in salaries earned by employees during the first half of June. June 18 Paid Henry's Hangar $1,890 for maintenance and repair services on the company plane. June 25 Collected $4,910 of the amounts billed to customers on June 15. June 30 Billed customers $16,450 for aerial photographs taken during the second half of the month. June 30 Paid…arrow_forwardKen Young and Kim Sherwood organized Reader Direct as a corporation; each contributed $46,000 cash to start the business and received 4,000 shares of stock. The store completed its first year of operations on December 31, 2020. On that date, the following financial items for the year were determined: cash on hand and in the bank, $41,500; amounts due from customers from sales of books, $27,600; equipment, $45,000; amounts owed to publishers for books purchased, $8,100; one-year notes payable to a local bank for $3,900. No dividends were declared or paid to the stockholders during the year. 2. Using the retained earnings equation and an openind balance of $0, work backwards to compute the amount of net income for the year ended December 31, 2020. Net Income = Ending RE + Dividends-Beginning REarrow_forward

- In June 2021, Wanda Fonda organized a corporation to provide drone photography services. The company, called Drone Queen Inc., began operations immediately. Transactions during the month of June were as follows: June 1 The corporation issued 60,000 shares of capital stock to Wanda Fonda in exchange for $60,000 cash. June 2 Purchased a plane from Utility Aircraft for $220,000. Made a $40,000 cash down payment and issued a note payable for the remaining balance. June 4 Paid Piarco Airport $2,500 to rent office and hangar space for the month. June 15 Billed customers $8,320 for aerial photographs taken during the first half of June. June 15 Paid $5,880 in salaries earned by employees during the first half of June. Paid Henry's Hangar $1,890 for maintenance and repair services on the company plane. June 18 June 25 Collected $4,910 of the amounts billed to customers on June 15. June 30 Billed customers $16,450 for aerial photographs taken during the second half of the month. June 30 Paid…arrow_forwardIn June 2021, Wanda Fonda organized a corporation to provide drone photography services. The company, called Drone Queen Inc., began operations immediately. Transactions during the month of June were as follows: June 1 The corporation issued 60,000 shares of capital stock to Wanda Fonda in exchange for $60,000 cash. June 2 Purchased a plane from Utility Aircraft for $220,000. Made a $40,000 cash down payment and issued a note payable for the remaining balance. June 4 Paid Piarco Airport $2,500 to rent office and hangar space for the month. June 15 Billed customers $8,320 for aerial photographs taken during the first half of June. June 15 Paid $5,880 in salaries earned by employees during the first half of June. June 18 Paid Henry's Hangar $1,890 for maintenance and repair services on the company plane. June 25 Collected $4,910 of the amounts billed to customers on June 15. June 30 Billed customers $16,450 for aerial photographs taken during the second half of the month. June 30 Paid…arrow_forwardIn June 2021, Wanda Fonda organized a corporation to provide drone photography services. The company, called Drone Queen Inc., began operations immediately. Transactions during the month of June were as follows: June 1 The corporation issued 60,000 shares of capital stock to Wanda Fonda in exchange for $60,000 cash. June 2 Purchased a plane from Utility Aircraft for $220,000. Made a $40,000 cash down payment and issued a note payable for the remaining balance. June 4 Paid Piarco Airport $2,500 to rent office and hangar space for the month. June 15 Billed customers $8,320 for aerial photographs taken during the first half of June. June 15 Paid $5,880 in salaries earned by employees during the first half of June. June 18 Paid Henry's Hangar $1,890 for maintenance and repair services on the company plane. June 25 Collected $4,910 of the amounts billed to customers on June 15. June 30 Billed customers $16,450 for aerial photographs taken during the second half of the month. June 30 Paid…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education