Concept explainers

Videos

Comprehensive Problem 1

✓ 8 Net income. $31,425

Kelly Pitney began her consulting business. Kelly Consulting, on April 1, 20Y8. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter During May, Kelly Consulting entered into the following transactions:

May 3. Received cash from clients as an advance payment for services to be provided and recorded it as unearned tree $4,500

- 5. Received cash from clients on account $2,450.

- 9. Paid cash for a newspaper advertisement $225.

- 13. Raid Office Station Co for part of the debt incurred on April $, $640.

- 15. Recorded services provided on account for the period May 1-15, $9,180.

- 16 Paid part-time receptionist for two weeks’ salary including the amount owed on April 30, $750.

- 17. Recorded cash from cash clients for fees earned during the period May 1–16, $8,360. Record the following transactions on Page 6 of the Journal

- 20. Purchased support on account $735.

- 21. Recorded services provided on account for the period May 16–20. $4,820

- 25. Recorded cash from cash clients for fees earned for the period May 17–23, $7,900

- 27. Received cash from clients on account $9,520.

- 28. Paid part-time receptionist for two weeks’ salary. $7S0.

- 30. Raid telephone bill for May. $260

- 31. Paid electricity bill for May, $810.

- 31. Recorded cash from cash clients tor lees earned for the period May 20–31. $3,300.

- 31. Recorded services provided on account for the remainder of May, $2,650.

- 31. Paid dividends $10,500

Instructions

- 1. The chart of accounts foe Kelly Consulting is shown us Exhibit 9. and the post-closing

trial balance as of April 30, 20Y8, is shown in Exhibit 17. for each account in the post-closing trial balance, enter the balance in the appropriate Balance column of a four-column account. Date the balances May 1. 20Y8. and place a check mark (✓) in the Posting Reference column. Journalize each of the May transactions in a two-column journal starting cm Page $ of the journal and using Kelly Consulting’s chart of accounts. (Do not insert the account numbers in the journal at this time.) - 2. Post the journal to a ledger of four-column accounts.

- 5. Prepare an unadjusted trial balance.

- 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6).

- (a) Insurance expired during May is $275.

- (b) Supplies on hand on May II are $715.

- (c)

Depreciation of office equipment for May is $330. - (d) Accrued receptionist salary on May 31 is $325.

- (e) Rent expired during May is $1600.

- (f) Unearned fees on May 31 are $3,210

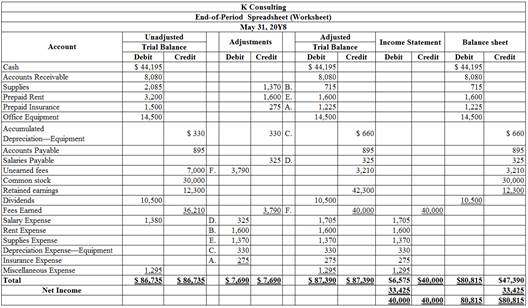

- 5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet

- 6. Journalize and post the

adjusting entries . Record the adjusting entries on Page 7 of the journal. - 7. Prepare an adjusted trial balance.

- 8. Prepare an income statement, a statement of

stockholders equity , and abalance sheet . - 9. Prepare and post the closing entries. Record the closing entries on Page 8 of the journal. Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry.

- 10. Prepare a post-closing trial balance.

1.

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

To journalize: The transactions of May in a two column journal beginning on page 5.

Explanation of Solution

Journalize the transactions of May in a two column journal beginning on page 5.

| Journal Page 5 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 20Y8 | 3 | Cash | 11 | 4,500 | |

| May | Unearned fees | 23 | 4,500 | ||

| (To record the cash received for the service yet to be provide) | |||||

| 5 | Cash | 11 | 2,450 | ||

| Accounts receivable | 12 | 2,450 | |||

| (To record the cash received from clients) | |||||

| 9 | Miscellaneousexpense | 59 | 225 | ||

| Cash | 11 | 225 | |||

| (To record the payment made for Miscellaneous expense) | |||||

| 13 | Accounts payable | 21 | 640 | ||

| Cash | 11 | 640 | |||

| (To record the payment made to creditors on account) | |||||

| 15 | Accounts receivable | 12 | 9,180 | ||

| Fees earned | 41 | 9,180 | |||

| (To record the revenue earned and billed) | |||||

| 14 | Salary Expense | 51 | 630 | ||

| Salaries payable | 22 | 120 | |||

| Cash | 11 | 750 | |||

| (To record the payment made for salary) | |||||

| Cash | 11 | 8,360 | |||

| 17 | Fees earned | 41 | 8,360 | ||

| (To record the receipt of cash) | |||||

Table (1)

| Journal Page 6 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 20Y8 | 18 | Supplies | 14 | 735 | |

| May | Accounts payable | 21 | 735 | ||

| (To record the payment made for automobile expense) | |||||

| 21 | Accounts receivable | 12 | 4,820 | ||

| Fees earned | 41 | 4,820 | |||

| (To record the payment of advertising expense) | |||||

| 25 | Cash | 11 | 7,900 | ||

| Fees earned | 41 | 7,900 | |||

| (To record the cash received from client for fees earned) | |||||

| 27 | Cash | 11 | 9,520 | ||

| Accounts receivable | 12 | 9,520 | |||

| (To record the cash received from clients) | |||||

| 28 | Salary expense | 51 | 750 | ||

| Cash | 11 | 750 | |||

| (To record the payment of salary) | |||||

| 30 | Miscellaneous Expense | 59 | 260 | ||

| Cash | 11 | 260 | |||

| (To record the payment of telephone charges) | |||||

| 31 | Miscellaneous Expense | 59 | 810 | ||

| Cash | 11 | 810 | |||

| (To record the payment of electricity charges) | |||||

| 31 | Cash | 11 | 3,300 | ||

| Fees earned | 41 | 3,300 | |||

| (To record the cash received from client for fees earned) | |||||

| 31 | Accounts receivable | 12 | 2,650 | ||

| Fees earned | 41 | 2,650 | |||

| (To record the revenue earned and billed) | |||||

| 31 | Dividends | 33 | 10,500 | ||

| Cash | 11 | 10,500 | |||

| (To record the drawing made for personal use) | |||||

Table (2)

(2), (6) and (9)

To record: The balance of each accounts in the appropriate balance column of a four-column account and post them to the ledger.

Explanation of Solution

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr.) and,

- The credit side (Cr).

| Account: Cash Account no.11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 22,100 | |||

| 3 | 5 | 4,500 | 26,600 | ||||

| 5 | 5 | 2,450 | 29,050 | ||||

| 9 | 5 | 225 | 28,825 | ||||

| 13 | 5 | 640 | 28,185 | ||||

| 16 | 5 | 750 | 27,435 | ||||

| 17 | 5 | 8,360 | 35,795 | ||||

| 25 | 6 | 7,900 | 43,695 | ||||

| 27 | 6 | 9,520 | 53,215 | ||||

| 28 | 6 | 750 | 52,465 | ||||

| 30 | 6 | 260 | 52,205 | ||||

| 31 | 6 | 810 | 51,395 | ||||

| 31 | 6 | 3,300 | 54,695 | ||||

| 31 | 6 | 10,500 | 44,195 | ||||

Table (3)

| Account: Accounts ReceivableAccount no.12 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 3,400 | |||

| 5 | 5 | 2,450 | 950 | ||||

| 15 | 5 | 9,180 | 10,130 | ||||

| 21 | 6 | 4,820 | 14,950 | ||||

| 27 | 6 | 9,520 | 5,430 | ||||

| 31 | 6 | 2,650 | 8,080 | ||||

Table (4)

| Account: SuppliesAccount no.14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 1,350 | |||

| 20 | 6 | 735 | 2,085 | ||||

| 30 | Adjusting | 7 | 1,350 | 715 | |||

Table (5)

| Account: Prepaid RentAccount no.15 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 3,200 | |||

| 31 | Adjusting | 7 | 1,600 | 1,600 | |||

Table (6)

| Account: Prepaid InsuranceAccount no.16 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 1,500 | |||

| 31 | Adjusting | 7 | 275 | 1,225 | |||

Table (7)

| Account: Office equipmentAccount no.18 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 14,500 | |||

Table (8)

| Account: Accumulated Depreciation-Office equipmentAccount no.19 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 330 | |||

| 31 | Adjusting | 7 | 330 | 660 | |||

Table (9)

| Account: Accounts Payable Account no.21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 800 | |||

| 13 | 5 | 640 | 160 | ||||

| 20 | 6 | 735 | 895 | ||||

Table (10)

| Account: Salaries Payable Account no.22 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 120 | |||

| 16 | 5 | 120 | |||||

| 31 | Adjusting | 7 | 325 | 325 | |||

Table (11)

| Account: Unearned Fees Account no.23 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 2,500 | |||

| 3 | 5 | 4,500 | 7,000 | ||||

| 31 | Adjusting | 7 | 3,790 | 3,210 | |||

Table (12)

| Account: Common StockAccount no.31 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 30,000 | |||

Table (13)

| Account: Retained EarningsAccount no.32 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 12,300 | |||

| 31 | Closing | 8 | 33,425 | 45,725 | |||

| 31 | Closing | 8 | 10,500 | 35,225 | |||

Table (14)

| Account: DividendsAccount no.33 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 31 | 6 | 10,500 | 10,500 | |||

| 31 | Closing | 8 | 10,500 | ||||

Table (15)

| Account: Income SummaryAccount no.34 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 31 | Closing | 8 | 40,000 | 40,000 | ||

| 31 | Closing | 8 | 6,575 | 33,425 | |||

| 31 | Closing | 8 | 33,425 | ||||

Table (16)

| Account: Fees earned Account no.41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 15 | 5 | 9,180 | 9,180 | |||

| 17 | 5 | 8,360 | 17,540 | ||||

| 21 | 6 | 4,820 | 22,360 | ||||

| 25 | 6 | 7,900 | 30,260 | ||||

| 31 | 6 | 3,300 | 33,560 | ||||

| 31 | 6 | 2,650 | 36,210 | ||||

| 31 | Adjusting | 7 | 3,790 | 40,000 | |||

| 31 | Closing | 8 | 40,000 | ||||

Table (17)

| Account: Salary expense Account no.51 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 16 | 5 | 630 | 630 | |||

| 28 | 6 | 750 | 1,380 | ||||

| 31 | Adjusting | 7 | 325 | 1,705 | |||

| 31 | Closing | 8 | 1,705 | ||||

Table (18)

| Account: Rent expense Account no.52 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 31 | Adjusting | 7 | 1,600 | 1,600 | ||

| 31 | Closing | 8 | 1,600 | ||||

Table (19)

| Account: Supplies expense Account no.53 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 31 | Adjusting | 7 | 1,370 | 1,370 | ||

| 31 | Closing | 8 | 1,370 | ||||

Table (20)

| Account: Depreciation expense Account no.54 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 31 | Adjusting | 7 | 330 | 330 | ||

| 31 | Closing | 8 | 330 | ||||

Table (21)

| Account: Insurance expense Account no.54 | |||||||

| Date | Item | PostRef. |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 31 | Adjusting | 7 | 275 | 275 | ||

| 31 | Closing | 8 | 275 | ||||

Table (22)

| Account: Miscellaneous expense Account no.59 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 9 | 5 | 225 | 225 | |||

| 30 | 6 | 260 | 485 | ||||

| 31 | 6 | 810 | 1,295 | ||||

| 31 | Closing | 8 | 1,295 | ||||

Table (23)

(3)

To prepare: The unadjusted trial balance of Consulting Kat May, 31.

Explanation of Solution

Adjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Prepare an unadjusted trial balance of Consulting K for the month ended May, 31 as follows:

|

K Consulting Unadjusted Trial Balance May 31, 20Y8 |

|||

| Particulars |

Account No. |

Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 2,085 | |

| Prepaid rent | 15 | 3,200 | |

| Prepaid insurance | 16 | 1,500 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated depreciation-Office equipment | 19 | 330 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 0 | |

| Unearned fees | 23 | 7,000 | |

| Common stock | 31 | 30,000 | |

| Retained earnings | 32 | 12,300 | |

| Dividends | 33 | 10,500 | |

| Fees earned | 41 | 36,210 | |

| Salary expense | 51 | 1,380 | |

| Rent expense | 52 | 0 | |

| Supplies expense | 53 | 0 | |

| Depreciation expense | 54 | 0 | |

| Insurance expense | 55 | 0 | |

| Miscellaneous expense | 59 | 1,295 | |

| Total | 86,735 | 86,735 | |

Table (22)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $86,735.

(5)

To enter: The unadjusted trial balance on an end-of-period spreadsheet.

Explanation of Solution

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (23)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

(6)

To Journalize: The adjusting entries of Consulting K for May 31.

Explanation of Solution

Adjusting entries:

An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

The adjusting entries of ConsultingK for May 31, 20Y8are as follows:

| Date | Accounts title and explanation | Post Ref. |

Debit ($) |

Credit ($) |

|

| 20Y8 | Insurance expense | 55 | 275 | ||

| May | 31 | Prepaid insurance | 16 | 275 | |

| (To record the insurance expense for May ) | |||||

| 31 | Supplies expense(1) | 53 | 1,370 | ||

| Supplies | 14 | 1,370 | |||

| (To record the supplies expense) | |||||

| 31 | Depreciation expense | 54 | 330 | ||

| Accumulated Depreciation | 19 | 330 | |||

| (To record the depreciation and the accumulated depreciation) | |||||

| 31 | Salaries expense | 51 | 325 | ||

| Salaries payable | 22 | 325 | |||

| (To record the accrued salaries payable) | |||||

| 31 | Rent expense | 52 | 1,600 | ||

| Prepaid rent | 15 | 1,600 | |||

| (To record the rent expense for May ) | |||||

| 31 | Unearned fees(2) | 23 | 3,790 | ||

| Fees earned | 41 | 3,790 | |||

| (To record the receipt of unearned fees) | |||||

Table (24)

Working notes:

(7)

To prepare: An adjusted trial balance of Consulting K for May 31, 20Y8.

Explanation of Solution

Spreadsheet: A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

An adjusted trial balanceof Consulting K for May 31, 20Y8 is prepared as follows:

|

K Consulting Adjusted Trial Balance May 31, 20Y8 |

|||

| Particulars |

Account No. |

Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 715 | |

| Prepaid insurance | 16 | 1,600 | |

| Prepaid rent | 15 | 1,225 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated Depreciation-Office equipment | 19 | 660 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 325 | |

| Unearned fees | 23 | 3,210 | |

| Common stock | 31 | 30,000 | |

| Retained earnings | 32 | 12,300 | |

| Dividends | 33 | 10,500 | |

| Fees earned | 41 | 40,000 | |

| Salary expense | 51 | 1,705 | |

| Rent expense | 52 | 1,600 | |

| Supplies Expense | 53 | 1,370 | |

| Depreciation expense | 54 | 330 | |

| Insurance expense | 55 | 275 | |

| Miscellaneous expense | 59 | 1,295 | |

| Total | 87,390 | 87,390 | |

Table (25)

The debit column and credit column of the adjusted trial balance are agreed, both having balance of $87,390.

(8)

To Prepare: An income statement for the year ended May 31, 20Y8.

Explanation of Solution

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

An income statement for the year ended May 31, 20Y8 is as follows:

| K Consulting | ||

| Income Statement | ||

| For the year ended May 31, 20Y8 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Fees Earned | 40,000 | |

| Expenses: | ||

| Salaries Expense | 1,705 | |

| Rent Expense | 1,600 | |

| Supplies Expense | 1,370 | |

| Depreciation Expense- Building | 330 | |

| Insurance Expense | 275 | |

| Miscellaneous Expense | 1,295 | |

| Total Expenses | 6,575 | |

| Net Income | $33,425 | |

Table (26)

Hence, the net income of K Consultingfor the year ended May 31, 20Y8is $33,425.

To Prepare: The statement of stockholders’ equity for the year ended May 31, 20Y8.

Explanation of Solution

The statement of stockholders’ equity for the year ended May 31, 20Y8 is as follows:

| G Consulting | ||

| Statement of Stockholders’ Equity | ||

| For the Year Ended May 31, 20Y8 | ||

| Particulars | Amount ($) | Amount ($) |

| Balance, May 1, 20Y7 | 12,300 | |

| Add: Net income | 33,425 | |

| Less: Dividends | (10,500) | |

| Change in retained earnings | 22,925 | |

| Balance, May 31, 20Y8 | $35,225 | |

Table (27)

Hence, retained earnings for the year ended May 31, 20Y8is $35,225.

To Prepare: The balance sheet of K Consulting at May 31, 20Y8.

Answer to Problem 1COP

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

| K Consulting | |||

| Balance Sheet | |||

| May 31, 20Y8 | |||

| Assets | |||

| Current Assets: | $ | $ | |

| Cash | 44,195 | ||

| Accounts Receivable | 8,080 | ||

| Supplies | 715 | ||

| Prepaid Rent | 1,600 | ||

| Prepaid Insurance | 1,225 | ||

| Total Current Assets | 55,815 | ||

| Property, plant and equipment: | |||

| Office Equipment | 14,500 | ||

| Less: Accumulated Depreciation | (660) | ||

| Total Plant Assets | 13,840 | ||

| Total Assets | $69,655 | ||

| Liabilities | |||

| Current Liabilities: | |||

| Accounts Payable | 895 | ||

| Salaries Payable | 325 | ||

| Unearned rent | 3,210 | ||

| Total Liabilities | $4,430 | ||

| Stockholder’s Equity | |||

| Common stock | 30,000 | ||

| Retained earnings | 35,225 | ||

| Total stockholder’s equity | 65,225 | ||

| Total Liabilities and stockholder’s Equity | $69,655 | ||

Table (28)

Explanation of Solution

It is one of the financial statements, which shows the assets, liabilities, and stockholders’ equity of a company at a particular point of time. It reveals the financial health of a company. Thus, this statement is also called as the Statement of Financial Position. It helps the users to know about the creditworthiness of a company as to whether the company has enough assets to pay off its liabilities.

Therefore, the total assets and total liabilities plus owners’ equity of Consulting Kat May 31, 20Y8 is $69,655.

(9)

To Journalize: The closing entries for KConsulting.

Answer to Problem 1COP

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| May 31, 20Y8 | Fees earned | 41 | 40,000 | |

| Salary expense | 51 | 1,705 | ||

| Rent Expense | 52 | 1,600 | ||

| Supplies Expense | 53 | 1,370 | ||

| Depreciation Expense | 54 | 330 | ||

| Insurance Expense | 55 | 275 | ||

| Miscellaneous Expense | 59 | 1,295 | ||

| Retained earnings | 34 | 33,425 | ||

| (To close the revenues and expenses account. Then the balance amount are transferred to retained earnings account) | ||||

| May 31, 20Y8 | Retained earnings | 32 | 10,500 | |

| Dividends | 33 | 10,500 | ||

| (To close the dividend account to retained earnings account) |

Table (4)

Explanation of Solution

Closing entries

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts such as retained earnings. It is passed at the end of the accounting period, to transfer the final balance.

Process of closing:

- The balance of revenue and expense are transferred to retrained earnings account.

- The balance of dividend account is transferred to retained earnings account to close the temporary accounts.

Rules of Debit and Credit:

- Debit, the revenue account and retained earnings account balance. In addition debit retained earnings account if it suffer loss (net loss)

- Credit, the expense account, retained earnings if it earn income (net income) and dividend account.

- Fees earned are a revenue account. Since the amount of revenue is closed and transferred to retained earnings account. Here, AS Company earned an income of $33,425. Therefore, it is debited.

- Wages Expense, Rent Expense, Insurance Expense, Utilities Expese, Supplies Expense, Depreciation Expense and Miscellaneous Expense are expense accounts. Since the amount of expenses are closed to Income Summary account. Therefore, it is credited.

Working Note:

Calculate net income on income summary account:

- The Dividend is paid to the shareholders out of the Retained Earnings. Thus, Retained Earnings is debited since the earnings are decreased on payment of dividend.

- Dividends is a component of stockholders’ equity account. It is credited because dividends are transferred to Retained Earnings account.

(10)

To Journalize: The closing entries for KConsulting.

Explanation of Solution

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

Prepare apost–closing trial balance of KConsulting for the month ended May 31, 20Y8 as follows:

|

Consulting K Post-closing Trial Balance May, 31, 20Y8 |

|||

| Particulars | Account Number | Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 715 | |

| Prepaid rent | 15 | 1,600 | |

| Prepaid insurance | 16 | 1,225 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated depreciation –Office Equipment | 19 | 660 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 325 | |

| Unearned rent | 23 | 3,210 | |

| Common stock | 31 | 30,000 | |

| Retained earnings | 32 | 35,225 | |

| Total | 70,315 | 70,315 | |

Table (5)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $70,315

Want to see more full solutions like this?

Chapter 4 Solutions

Corporate Financial Accounting

- Comprehensive problem 1 Kelly Pitney began her consulting business, Kelly Consulting, on April 1, 2016. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter. During May, Kelly Consulting entered into the following transactions: May 3. Received cash from clients as an advance payment for services to be provided and recorded it as unearned fees, 4,500. 5. Received cash from clients on account, 2,450. 9. Paid cash for a newspaper advertisement. 225. 13. Paid Office Station Co. for part of the debt incurred on April 5, 640. 15. Recorded services provided on account for the period May 1-15; 9,180. 16. Paid part-time receptionist for two weeks salary including the amount owed on April 30, 750. 17. Recorded cash from cash clients for fees earned during the period May 1-16, 8,360. Record the following transactions on Page 6 of the journal: 20. Purchased supplies on account, 735. 21. Recorded services provided on account for the period May 16-20, 4,820. 25. Recorded cash from cash clients for fees earned for the period May 17-23, 7,900. 27. Received cash from clients on account, 9,520. 28. Paid part-time receptionist for two weeks salary, 750. 30. Paid telephone bill for May, 260. 31. Paid electricity bill for May, 810. 31. Recorded cash from cash clients for fees earned for the period May 26-31, 3,300. 31. Recorded services provided on account for the remainder of May, 2,650. 31. Paid dividends, 10,500. Instructions 1. The chart of accounts for Kelly Consulting is shown in Exhibit 9, and the post-closing trial balance as of April 30, 2016, is shown in Exhibit 17. For each account in the post-closing trial balance, enter the balance in the appropriate Balance column of a four-column account. Date the balances May 1, 2016, and place a check mark () in the Posting Reference column. Journalize each of the May transactions in a two- column journal starting on Page 5 of the journal and using Kelly Consultings chart of accounts. (Do not insert the account numbers in the journal at this time.) 2. Post the journal to a ledger of four-column accounts. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6). a. Insurance expired during May is 275. b. Supplies on hand on May 31 are 715. c. Depreciation of office equipment for May is 330. d. Accrued receptionist salary on May 31 is 325. e. Rent expired during May is 1,600. f. Unearned fees on May 31 are 3,210. 5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 7 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a retained earnings statement, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 8 of the journal. (Income Summary is account 34 in the chart of accounts.) Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. 10. Prepare a post-closing trial balance.arrow_forwardKelly Pitney began her consulting business, Kelly Consulting, on April 1, 2016. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter. During May, Kelly Consulting entered into the following transactions: May 3. Received cash from clients as an advance payment for services to be provided and recorded it as unearned fees, 4,500. 5. Received cash from clients on account, 2,450. 9. Paid cash for a newspaper advertisement, 225. 13. Paid Office Station Co. for part of the debt incurred on April 5, 640. 15. Recorded services provided on account for the period May 115, 9,180. 16. Paid part-time receptionist for two weeks' salary including the amount owed on April 30, 750. 17. Recorded cash from cash clients for fees earned during the period May 116, 8,360. Record the following transactions on Page 6 of the journal: 20. Purchased supplies on account, 735. 21. Recorded services provided on account for the period May 1620, 4,820. 25. Recorded cash from cash clients for fees earned for the period May 1723, 7,900. 27. Received cash from clients on account, 9,520. 28. Paid part-time receptionist for two weeks' salary, 750. 30. Paid telephone bill for May, 260. 31. Paid electricity bill for May, 810. 31. Recorded cash from cash clients for fees earned for the period May 2631, 3,300. 31. Recorded services provided on account for the remainder of May, 2,650. 31. Kelly withdrew 10,500 for personal use. Instructions 1. The chart of accounts for Kelly Consulting is shown in Exhibit 9, and the post-closing trial balance as of April 30, 2016, is shown in Exhibit 17. For each account in the post-closing trial balance, enter the balance in the appropriate Balance column of a four-column account. Date the balances May 1, 2016, and place a check mark () in the Posting Reference column. Journalize each of the May transactions in a two-column journal starting on Page 5 of the journal and using Kelly Consultings chart of accounts. (Do not insert the account numbers in the journal at this time.) 2. Post the journal to a ledger of four-column accounts. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6). a. Insurance expired during May is 275. b. Supplies on hand on May 31 are 715. c. Depreciation of office equipment for May is 330. d. Accrued receptionist salary on May 31 is 325. e. Rent expired during May is 1,600. f. Unearned fees on May 31 are 3,210. 5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 7 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of owners equity, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 8 of the journal. (Income Summary is account #33 in the chart of accounts.) Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. 10. Prepare a post-closing trial balance.arrow_forwardContinuing Problem 4.Total of Debit column: 40,750 The transactions completed by PS Music during June 20Y5 were described .it the end of Chapter 1. The following transactions were completed during July, the second month of businesss operations: July 1. Peyton Smith made an additional investment k PS Music in exchange for common stock by depositing 5,000 in PS Mu wet checking account. 1.Instead of continuing to share office space with a local real estate agency. Peyton decided to rent office space near a local musk store, Paid rent for July, 1,750. 1.Paid a premium of 2,700 for a comprehensive insurance policy covering liability, theft and fire. The policy covers a one year period. 2.Received 1,000 on account 3. On behalf of PS Musk, Peyton signed a contract with a local radio station. KXMD, to provide guest spots for the next three months. The contract requires PS Musk to provide a guest disc jockey for 80 hours per month for a monthly fee of 3,600. Any additional hours beyond 80 will be billed to KXMD at 40 per hour. In accordance with the contract Peyton received 7,200 from KXMD as an advance payment for the first two months. 3.Paid 2SO on account 4.Paid an attorney 900 for reviewing the July 3 contract with KXMD. (Record as Miscellaneous Expense.) 5.Purchased office equipment on account from Office Mart. 7,500. 8.Paid for a newspaper advertisement 200. 11.Received 1.000 for serving as a disc jockey for a party. 13.Paid 700 to a local audio electronics store for rental of digital recording equipment 14.Paid wages of 1,200 to receptionist and part-time assistant. Enter the following transactions on Pane 2 of the two-column journal: 16.Received 2,000 for serving as a disc jockey for a wedding reception. 18.Purchased supplies on account 850 21.Paid 620 to Upload Musk for use of its current musk demos in making various musk sets. 22.Paid 800 to a local radio station to advertise the services of PS Music twice daily for the remainder of July. 23.Served as disc jockey for a party for 2,500 Received 750, with the remainder due August 4.20YS. 27.Paid electric Ml 915. 28.Paid wages of 1,200 to receptionist and part-time assistant. 29.Paid miscellaneous expenses, 540. 30.Served as a disc jockey for a charity ball for 1,500, Received S00 with the remainder due on August 9. 20Y5. 31.Received 3,000 for serving as a disc jockey for a party. 31.Paid 1.400 royalties (musk expense) to National Musk Clearing for use of various artists music during July. 31. Paid dividends, 1,250. PS Musics chart of accounts and the balance of accounts as of July 1, 20Y5 (all normal balances), are as follows: 11 Cash 3,920 12 Accounts Receivable 1,000 14 Supplies 170 15 Prepaid Insurance 17 Office Equipment 21 Accounts Payable 250 23 Unearned Revenue 31 Common Stock 4.000 33 Dividends 500 41 Fees Earned 6,200 50 Wages Expense 400 51 Office Rent Expense 800 52 Equipment Rent Expense 67S 53 Utilities Expense 300 54 Music Expense 1.590 55 Advertising Expense 500 56 Supplies Expense 180 59 Miscellaneous Expense 415 Instructions 1. Enter the July 1, 20Y5, account balances in the appropriate balance column of a four-column account. Write Balance in the Item column, and place a check mark () in the Posting Reference column. (Hint: Verify the equality of the debit and credit balances in the ledger before proceeding with the next instruction.) 2. Analyze and journalize each transaction in a two-column journal beginning on Page 1, omitting journal entry explanations. 3. Post the journal to the ledger, extending the account balance to the appropriate balance column after each posting. 4. Prepare an unadjusted trial balance as of July 31, 20Y5.arrow_forward

- Transactions; financial statements 2. Net income: 10,850 On April 1, 20Y8, Maria Adams established Custom Realty. Maria completed the following transactions during the month of April: a. Opened a business bank account with a deposit of 24,000 in exchange for common stock. b. Paid rent on office and equipment for the month, 3,600. c. Paid automobile expenses for month, 1,350, and miscellaneous expenses, 600. d. Purchased supplies on account, 1,200. e. Earned sales commissions, receiving cash, 19,800. f. Paid creditor on account, 750. g. Paid office salaries, 2,500. h. Paid dividends, 3,500. i. Determined that the cost of supplies on hand was 300; therefore, the cost of supplies used was 900. Instructions 1. Indicate the effect of each transaction and the balances after each transaction, using the following tabular headings: 2. Prepare an income statement for April, a statement of stockholders equity for April, and a balance sheet as of April 30.arrow_forwardBrief Exercise 2-32 Journalize Transactions Galle Inc. entered into the following transactions during January. January, 1: Borrowed $50,000 from First Street Bank by signing a note payable. January, 4: Purchased $25,000 of equipment for cash. January, 6: Paid $500 to landlord for rent for January. January, 15: Performed services for customers on account. $10,000. January, 25: Collected $3,000 from customers for services performed in Transaction d. January, 30: Paid salaries of $2,500 for the current month. Required: Prepare journal entries for the transactions.arrow_forwardProblem 2-56A Analyzing Transactions Luis Madero, after working for several years with a large public accounting firm decided to open his own accounting service. The business is operated as a corporation under the name Madero Accounting Services. The following captions and amounts summarize Maderos balance sheet at July 31, 2019. The following events occurred during August 2019. Issued common stock to Ms. Garriz in exchange for $15,000 cash. Paid $850 for first months rent on office space. Purchased supplies of $2,250 on credit. Borrowed $8,000 from the bank. Paid $1,080 on account for supplies purchased earlier on credit. Paid secretarys salary for August of $2,150. Performed amounting services for clients who paid cash upon completion of the service in the total amount of $4,700. Used $3,180 of the supplies on hand. Perfumed accounting services for clients on credit in the total amount of $1,920. Purchased $500 in supplies for cash. Collected $1,290 cash from clients for whom services were performed on credit. Paid $1,000 dividend to stockholders. Required: Record the effects of the transactions listed above on the accounting equation. Use the format given in the problem, starting with the totals at July 31, 20l9. Prepare the trial balance at August 31, 2019.arrow_forward

- Exercise 2-43 Transaction Analysis Goal Systems, a business consulting firm, engaged in the following transactions: Issued common stock for $75,000 cash. Borrowed $35,000 from a bank. Purchased equipment for $12,000 cash. Prepaid rent on office space for 6 months in the amount of $7.800. Performed consulting services in exchange for $6,300 cash. Perfumed consulting services on credit in the amount of $18,750. Incurred and paid wage expense of $9,500. Collected $10,200 of the receivable arising from Transaction f. Purchased supplies for $1,800 on credit. Used $1,200 of the supplies purchased in Transaction i. Paid for all of the supplies purchased in Transaction i. Required: For each transaction described above. indicate the effects on assets, liabilities, and stockholders equity using the format below.arrow_forwardBrief Exercise 2-28 Assumptions and Principles Five common accounting practices are listed below: A customer pays $20 to mail a package on December 30. The delivery company recognizes revenue when the package is delivered in January. Jim Trotter owns C**S Heating Company. In preparing the financial statements, Trotter makes sure that the purchase of a new truck for personal use is not included in C&S’s financial statements. Moseley Inc. recorded land at its purchase price of $50,000. In future periods, the land is reflected in the financial statements at $50,000. Mack Company purchases inventory in March. However, it does not expense that inventory until it is sold in April. Mueller Inc. prepares quarterly and annual financial statements. Required: Identify the amounting principle or assumption that best describes each practicearrow_forwardProblem 2-593 Journalizing Transactions Monilast Chemicals engaged in the following transactions during December 2019: Dec 2 Paid rent on office furniture, $1,200. 3 Borrowed $25,030 on a 9-month, 3% note. 7 Provided services on credit. $42,600. 10 Purchased supplies on credit, $2,850. 13 Collected accounts receivable, $20,150. 19 Issued common stock, $50000. 22 Paid employee wages for December. $13,825. 23 Paid accounts payable, $1,280. 25 Provided services for cash, $13,500. 30 Paid utility bills for December, $1,975. Required: Prepare a journal entry for each transaction.arrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Corporate Financial AccountingAccountingISBN:9781337398169Author:Carl Warren, Jeff JonesPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781337398169Author:Carl Warren, Jeff JonesPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,