Concept explainers

Videos

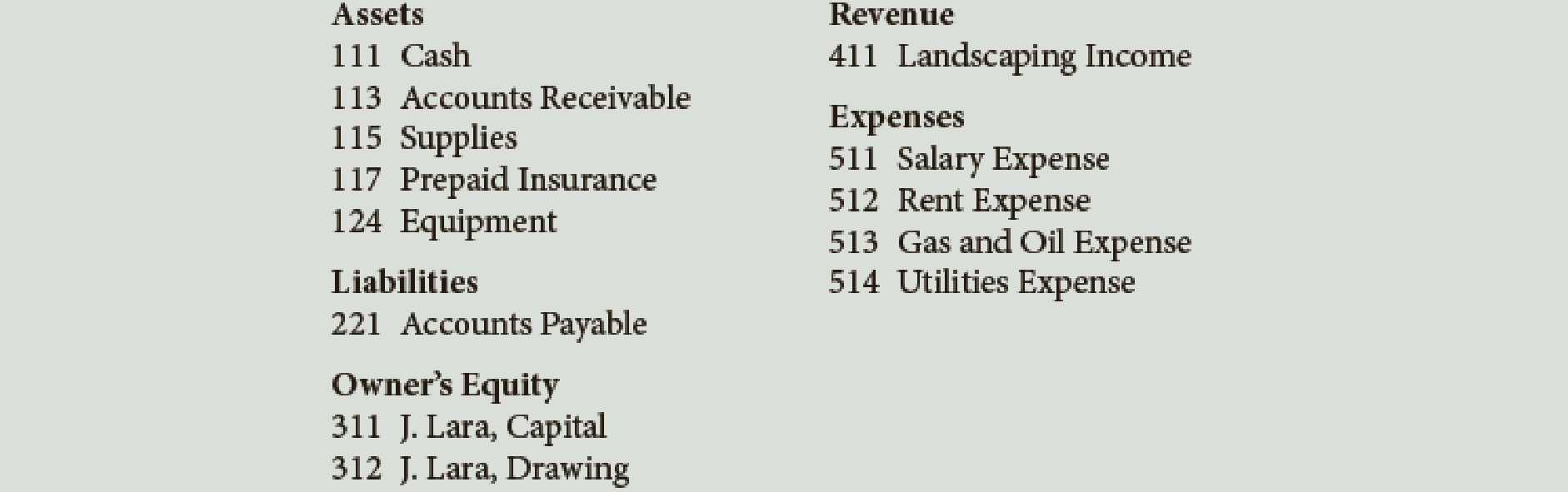

Lara’s Landscaping Service has the following chart of accounts:

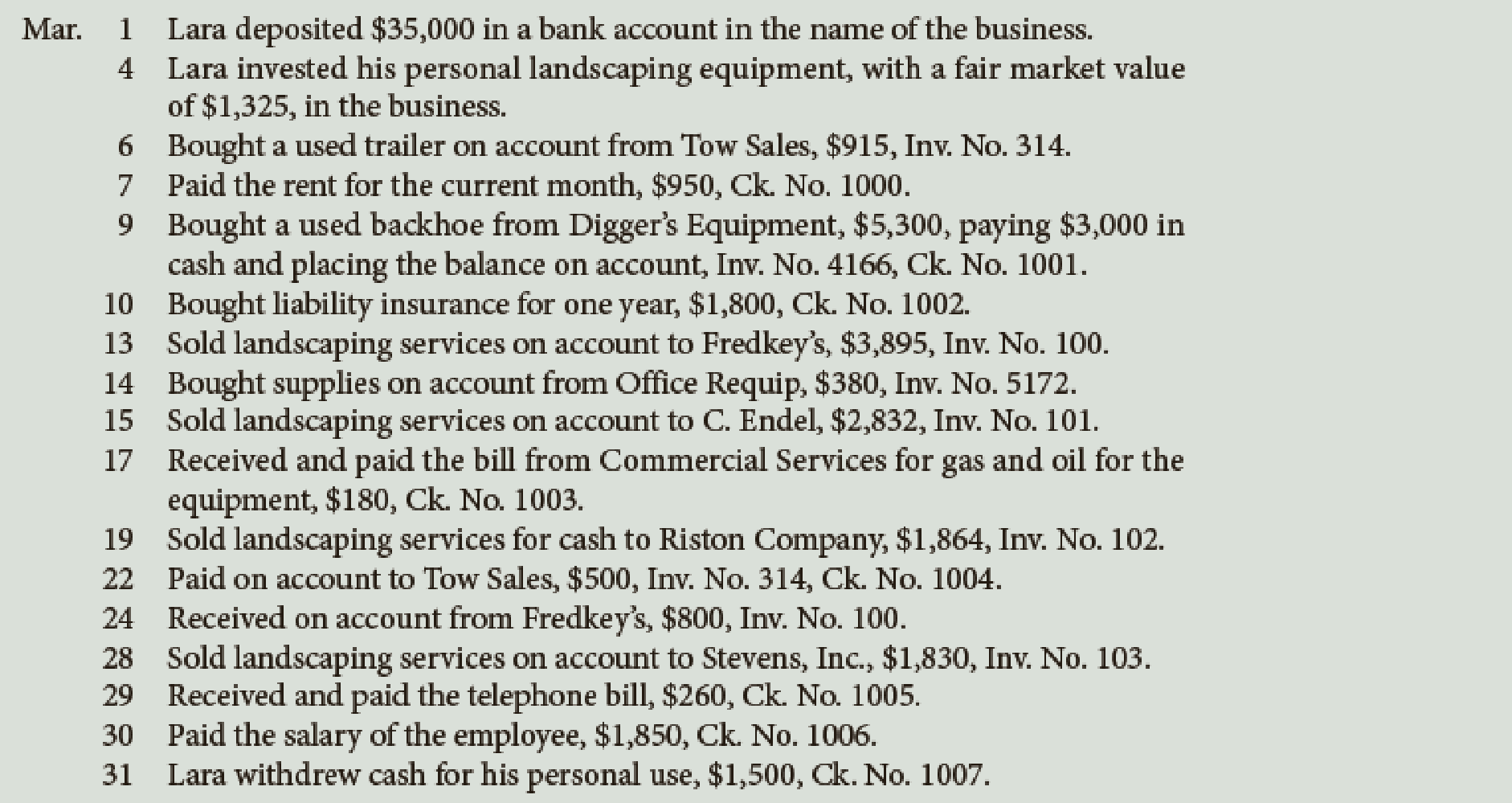

The following transactions were completed by Lara’s Landscaping Service:

Required

- 1. Journalize the transactions in the general journal. Provide a brief explanation for each entry.

- 2. If you are using working papers, write the name of the owner on the Capital and Drawing accounts. (Skip this step if you are using CLGL.)

- 3.

Post the journal entries to the general ledger accounts. (Skip this step if you are using CLGL.) - 4. Prepare a

trial balance dated March 31, 20–.

*If you are using CLGL, use the year 2020 when recording transaction! and preparing reports.

1.

Prepare journal entries for the given transactions.

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- ■ Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- ■ Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Prepare journal entries for the given transactions.

Transaction on March 1:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| March | 1 | Cash | 111 | 35,000 | ||

| JL, Capital | 311 | 35,000 | ||||

| (Record cash invested in the business by JL) | ||||||

Table (1)

Description:

- ■ Cash is an asset account. Since cash is invested in the business, asset account increased, and an increase in asset is debited.

- ■ JL, Capital is an equity account. Since cash is contributed as capital by the owner, equity value increased, and an increase in equity is credited.

Transaction on March 4:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| March | 4 | Equipment | 124 | 1,325 | ||

| JL, Capital | 311 | 1,325 | ||||

| (Record equipment invested in the business by JL) | ||||||

Table (2)

Description:

- ■ Equipment is an asset account. Since equipment is invested in the business, asset account increased, and an increase in asset is debited.

- ■ JL, Capital is an equity account. Since equipment is contributed as capital by the owner, equity value increased, and an increase in equity is credited.

Transaction on March 6:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| March | 6 | Equipment | 124 | 915 | ||

| Accounts Payable | 221 | 915 | ||||

| (Record purchase of equipment) | ||||||

Table (3)

Description:

- ■ Equipment is an asset account. Since equipment is bought, asset account increased, and an increase in asset is debited.

- ■ Accounts Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on March 7:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| March | 7 | Rent Expense | 512 | 950 | ||

| Cash | 111 | 950 | ||||

| (Record payment of rent expense) | ||||||

Table (4)

Description:

- ■ Rent Expense is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on March 9:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| March | 9 | Equipment | 124 | 5,300 | ||

| Cash | 111 | 3,000 | ||||

| Accounts Payable | 221 | 2,300 | ||||

| (Record purchase of equipment) | ||||||

Table (5)

Description:

- ■ Equipment is an asset account. Since equipment is bought, asset account increased, and an increase in asset is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

- ■ Accounts Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on March 10:

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| March | 10 | Prepaid Insurance | 117 | 1,800 | ||

| Cash | 111 | 1,800 | ||||

| (Record payment of insurance in advance) | ||||||

Table (6)

Description:

- ■ Prepaid Insurance is an asset account. Since insurance is paid in advance, it is recorded as asset until it is consumed. So, asset value is increased, and an increase in asset is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on March 13:

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| March | 13 | Accounts Receivable | 113 | 2,832 | ||

| Landscaping Income | 411 | 2,832 | ||||

| (Record services performed on account) | ||||||

Table (7)

Description:

- ■ Accounts Receivable is an asset account. The amount is increased because amount to be received increased, and an increase in asset is debited.

- ■ Landscaping Income is a revenue account. Since gains and revenues increase equity, and an increase in equity is credited, Landscaping Income account is credited.

Transaction on March 14:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| March | 14 | Supplies | 113 | 380 | ||

| Accounts Payable | 411 | 380 | ||||

| (Record supplies bought on account) | ||||||

Table (8)

Description:

- ■ Supplies is an asset account. Since store supplies are bought, asset account increased, and an increase in asset is debited.

- ■ Accounts Payable is a liability account. Since the payable increased, the liability increased, and an increase in liability is credited.

Transaction on March 15:

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| March | 15 | Accounts Receivable | 113 | 2,832 | ||

| Landscaping Income | 411 | 2,832 | ||||

| (Record services performed on account) | ||||||

Table (9)

Description:

- ■ Accounts Receivable is an asset account. The amount is increased because amount to be received increased, and an increase in asset is debited.

- ■ Landscaping Income is a revenue account. Since gains and revenues increase equity, and an increase in equity is credited, Landscaping Income account is credited.

Transaction on March 17:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| March | 17 | Gas and Oil Expense | 513 | 180 | ||

| Cash | 111 | 180 | ||||

| (Record payment of oil and gas expense) | ||||||

Table (10)

Description:

- ■ Gas and Oil Expense is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on March 19:

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| March | 19 | Cash | 111 | 1,864 | ||

| Landscaping Income | 411 | 1,864 | ||||

| (Record revenue earned and received) | ||||||

Table (11)

Description:

- ■ Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- ■ Landscaping Income is a revenue account. Since gains and revenues increase equity, and an increase in equity is credited, Landscaping Income account is credited.

Transaction on March 22:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| March | 22 | Accounts Payable | 221 | 500 | ||

| Cash | 111 | 500 | ||||

| (Record cash paid on account) | ||||||

Table (12)

Description:

- ■ Accounts Payable is a liability account. Since the payable decreased, the liability decreased, and a decrease in liability is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on March 24:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| March | 24 | Cash | 111 | 800 | ||

| Accounts Receivable | 113 | 800 | ||||

| (Record cash received on account) | ||||||

Table (13)

Description:

- ■ Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- ■ Accounts Receivable is an asset account. Since amount to be received has decreased, asset account decreased, and a decrease in asset is credited.

Transaction on March 28:

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| March | 28 | Accounts Receivable | 113 | 1,400 | ||

| Landscaping Income | 411 | 1,400 | ||||

| (Record services performed on account) | ||||||

Table (14)

Description:

- ■ Accounts Receivable is an asset account. The amount is increased because amount to be received increased, and an increase in asset is debited.

- ■ Landscaping Income is a revenue account. Since gains and revenues increase equity, and an increase in equity is credited, Landscaping Income account is credited.

Transaction on March 29:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| March | 29 | Utilities Expense | 514 | 260 | ||

| Cash | 111 | 260 | ||||

| (Record payment of utilities expense) | ||||||

Table (15)

Description:

- ■ Utilities Expense is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on March 30:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| March | 30 | Salary Expense | 511 | 1,850 | ||

| Cash | 111 | 1,850 | ||||

| (Record payment of salary expense) | ||||||

Table (16)

Description:

- ■ Salary Expense is an expense account. An increase in expense reduces the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Transaction on March 31:

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| March | 31 | JL, Drawing | 312 | 1,500 | ||

| Cash | 111 | 1,500 | ||||

| (Record cash withdrawn by JL for personal use) | ||||||

Table (17)

Description:

- ■ JL, Drawing is a contra-capital account. The contra-capital accounts decrease the equity value, and a decrease in equity is debited.

- ■ Cash is an asset account. Since cash is withdrawn, asset account decreased, and a decrease in asset is credited.

2.

Indicate the names of owner above the Capital and Drawing accounts.

Explanation of Solution

Owners’ equity: The financial interest of the owners to invest in the business is referred to as owners’ equity or capital. Owners’ equity comprises of capital, drawings, revenues and expenses.

Write the name of owner, JL before the capital and drawings terms and name those accounts as JL, Capital account and JL, Drawing account.

3.

Post the journalized transactions in the ledger accounts.

Explanation of Solution

Ledger: Ledger is a book in which the accounts are summarized and grouped from the transactions recorded in the journal.

Post the journalized transactions in the ledger accounts.

| ACCOUNT Cash ACCOUNT NO. 111 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 1 | 1 | 35,000 | 35,000 | |||

| 7 | 1 | 950 | 34,050 | ||||

| 9 | 1 | 3,000 | 31,050 | ||||

| 10 | 1 | 1,800 | 29,250 | ||||

| 17 | 1 | 180 | 29,070 | ||||

| 19 | 1 | 1,864 | 30,934 | ||||

| 22 | 1 | 500 | 30,434 | ||||

| 24 | 1 | 800 | 31,234 | ||||

| 29 | 1 | 260 | 30,974 | ||||

| 30 | 1 | 1,850 | 29,124 | ||||

| 31 | 1 | 1,500 | 27,624 | ||||

Table (18)

| ACCOUNT Accounts Receivable ACCOUNT NO. 113 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 13 | 1 | 3,895 | 3,895 | |||

| 15 | 1 | 2,832 | 6,727 | ||||

| 24 | 1 | 800 | 5,927 | ||||

| 28 | 1 | 1,830 | 7,757 | ||||

Table (19)

| ACCOUNT Supplies ACCOUNT NO. 115 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 14 | 1 | 380 | 380 | |||

Table (20)

| ACCOUNT Prepaid Insurance ACCOUNT NO. 117 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 10 | 1 | 1,800 | 1,800 | |||

Table (21)

| ACCOUNT Equipment ACCOUNT NO. 124 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 4 | 1 | 1,325 | 1,325 | |||

| 6 | 1 | 915 | 2,240 | ||||

| 9 | 1 | 5,300 | 7,540 | ||||

Table (22)

| ACCOUNT Accounts Payable ACCOUNT NO. 221 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 6 | 1 | 915 | 915 | |||

| 9 | 1 | 2,300 | 3,215 | ||||

| 14 | 1 | 380 | 3,595 | ||||

| 22 | 1 | 500 | 3,095 | ||||

Table (23)

| ACCOUNT JL, Capital ACCOUNT NO. 311 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 1 | 1 | 35,000 | 35,000 | |||

| 4 | 1 | 1,325 | 36,325 | ||||

Table (24)

| ACCOUNT JL, Drawing ACCOUNT NO. 312 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 31 | 1 | 1,500 | 1,500 | |||

Table (25)

| ACCOUNT Landscaping Income ACCOUNT NO. 411 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 13 | 1 | 3,895 | 3,895 | |||

| 15 | 1 | 2,832 | 6,727 | ||||

| 19 | 1 | 1,864 | 8,591 | ||||

| 28 | 1 | 1,830 | 10,421 | ||||

Table (26)

| ACCOUNT Salary Expense ACCOUNT NO. 511 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 30 | 1 | 1,850 | 1,850 | |||

Table (27)

| ACCOUNT Rent Expense ACCOUNT NO. 512 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 7 | 1 | 950 | 950 | |||

Table (28)

| ACCOUNT Gas and Oil Expense ACCOUNT NO. 513 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 17 | 1 | 180 | 180 | |||

Table (29)

| ACCOUNT Utilities Expense ACCOUNT NO. 514 | |||||||

| Date | Item | Post. Ref. | Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| March | 29 | 1 | 260 | 260 | |||

Table (30)

4.

Prepare the trial balance for L’s Landscaping Service as at March 31, 20--.

Explanation of Solution

Trial balance: Trial balance is a summary of all the asset, liability, and equity accounts and their balances.

Prepare the trial balance for L’s Landscaping Service as at March 31, 20--.

| L’s Landscaping Service | ||

| Trial Balance | ||

| March 31, 20-- | ||

| Account Title | Debit ($) | Credit ($) |

| Cash | $27,624 | |

| Accounts Receivable | 7,757 | |

| Supplies | 380 | |

| Prepaid Insurance | 1,800 | |

| Equipment | 7,540 | |

| Accounts Payable | $3,095 | |

| JL, Capital | 36,325 | |

| JL, Drawing | 1,500 | |

| Landscaping Income | 10,421 | |

| Salary Expense | 1,850 | |

| Rent Expense | 950 | |

| Gas and Oil Expense | 180 | |

| Miscellaneous Expense | 260 | |

| Total | $49,841 | $49,841 |

Table (31)

Hence, the debit and credit total of trial balance of L’s Landscaping Service at March 31, 20-- is 49,841.

Want to see more full solutions like this?

Chapter 3 Solutions

College Accounting: A Career Approach (with Quickbooks Accountant 2015 Cd-rom)

Additional Business Textbook Solutions

Introduction To Managerial Accounting

Intermediate Accounting (2nd Edition)

PRINCIPLES OF TAXATION F/BUS.+INVEST.

Managerial Accounting: Creating Value in a Dynamic Business Environment

Auditing And Assurance Services

Managerial Accounting: Tools for Business Decision Making

- Leanders Landscaping Service maintains the following chart of accounts: The following transactions were completed by Leander: Required 1. Journalize the transactions in the general journal. Prepare a brief explanation for each entry. 2. If you are using working papers, write the name of the owner on the Capital and Drawing accounts. 3. Post the journal entries to the general ledger accounts. (Skip this step if you are using CLGL.) 4. Prepare a trial balance dated April 30, 20. If you are using CLGL, use the year 2020 when recording transactions and preparing reports.arrow_forwardThe following transactions occurred for Luminary Engineering: View the transactions. Journalize the transactions of Luminary Engineering. Include an explanation with each journal entry. Use the following accounts: Cash; Accounts Receivable; Supplies; Equipment; Accounts Payable; Notes Payable; Luminary, Capital; Luminary, Withdrawals; Service Revenue; and Utilities Expense. (Record debits first, then credits. Select the explanation on the last line of the journal entry table.) July 2: Received $15,000 contribution from Bobby Luminary, owner, in exchange for capital. Date Jul. 2 Transactions Jul. 2 Accounts and Explanation Jul. 4 Jul. 5 Jul. 10 Jul. 12 Jul. 19 Jul. 21 Jul. 27 Debit Received $15,000 contribution from Bobby Luminary, owner, in exchange for capital. Paid utilities expense of $440. Purchased equipment on account, $2,600. Performed services for a client on account, $3,500. Borrowed $7,200 cash, signing a notes payable. Luminary withdrew $650 cash from the business. Purchased…arrow_forwardPost these transactions from each General Journal into the General Ledger accounts. When posting transactions to the general ledger, use the transaction letters a, b, c, d, or e as the description for each entry. Also, the dates must be entered in the format dd/mmm (ie, 15/Jan).arrow_forward

- urnalizing entries, information can be entered into T-Accounts and/or the four-column ledger. Enter the information from the T-Account and calculate the running balance in the appropriate place in the four-column ledger to review the similarities between the two formats.arrow_forwardPrepare general journal entries to record these transactions. You do have to enter descriptions for the entries for this problem.arrow_forwardidentify and discuss the steps in the recording process. Be sure to discuss what each step does and how it relates to the steps before and after it. Then, answer the following questions: Should business transactions credits and debits be recorded directly into the ledger accounts? What are the advantages of recording in the journal before posting transactions into the ledger?arrow_forward

- The general ledger of Jay Consulting shows the following balances at July 31: Jay has asked you to develop a worksheet that will serve as a trial balance (file name PTB). Use the data provided as input for your model. Review the Model-Building Problem Checklist on page 154 to ensure that your worksheet is complete. Print the worksheet when done. Check figure: Total debits, 17,731. To test your model, use the following balances at August 31: Print the worksheet when done. Check figure: Total debits, 18,810. CHART (optional) Using the test data worksheet, prepare a pie chart showing the percentage of each asset to total assets. Print the chart when done.arrow_forwardjournalize the transactions, please explain to me how you got the numbersarrow_forward*Required: Record the transactions using a general journal. Create your own account titles that will appropriately describe the exchanges of values. Post in T-accounts and compute the total assets, liabilities, and equity.arrow_forward

- A table of data for a library is shown in the table. Normalize these data into the third normal form, preparing it for use in a relational database environment. The library’s computer is programmed to compute the due date to be 14 days after the checkout date. Document the steps necessary to normalize the data similar to the procedures found in the chapter. Index any fields necessary and show how the databases are related.arrow_forwardDo you have to manually balance a journal entry or does Quickbooks do that for you?arrow_forwardcan you show me the correct journal entries for these please, want to compare to double check my work.arrow_forward

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning